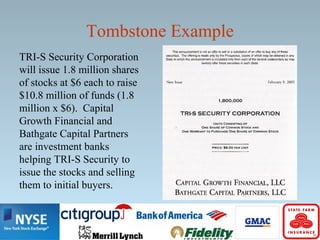

Direct finance involves borrowers borrowing funds directly from lenders through financial markets by selling securities. Financial markets transfer funds from lenders to borrowers through primary and secondary markets. Primary markets involve the initial sale of new securities, while secondary markets allow existing securities to be traded. Financial markets provide risk sharing, liquidity, and information services. They are classified by maturity, type of claim, and trading place.

![Repurchase Agreements

• Repurchase agreement (repo): an agreement that one

party sell securities to the other party with a promise

that the former will buy it back the securities from the

later at the set price.

– It is effectively short-term loan for which often U.S.

Treasury bills serve as collateral (an asset that the lender

receives if the borrower does not pay back the loan).

– Usually maturity of less than two weeks

– Analogy: Pawnshop [This is not repo, but the mechanism

behind is same.]](https://image.slidesharecdn.com/learningunit04-2012-150115224920-conversion-gate01/85/Econ315-Money-and-Banking-Learning-Unit-04-Direct-Finance-29-320.jpg)

![Banker’s Acceptance

• Banker’s acceptance: a bank draft (like check) issued

by a firm, payable at some future date, and

guaranteed by the bank that stamps it “accepted.”

– An accepting bank requires the issuing firm to deposit the

required funds into a special account.

– Used for foreign trades where exporters and importers do

not each other, but they know some large banks in two

countries

– Analogy: you sell a good at e-bay to someone. You may

not accept any personal check from him, but PayPal

payment since you know PayPal). [This is NOT a banker’s

acceptance, but the mechanism behind is same.]](https://image.slidesharecdn.com/learningunit04-2012-150115224920-conversion-gate01/85/Econ315-Money-and-Banking-Learning-Unit-04-Direct-Finance-31-320.jpg)