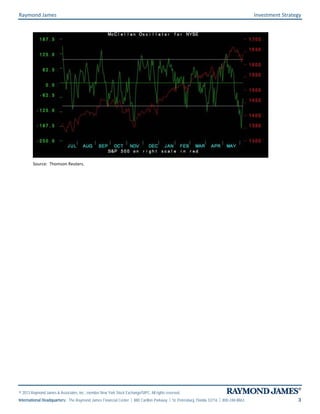

The document discusses investment strategies and thinking processes. It summarizes that good thinking is a lonely process that requires anticipating change correctly. It discusses how linear thinking can cause investors to miss opportunities for change. It provides examples from history where thinking on the margins helped identify opportunities, such as recognizing changes in technology stocks in the 1960s and interest rates in the 1980s. It analyzes current market conditions and predicts the odds of a new secular bull market are now 45-50%, though few investors currently believe this. It concludes that select market correlations broke down last week and economic reports imply tapering may be delayed, supporting stocks in the near-term.