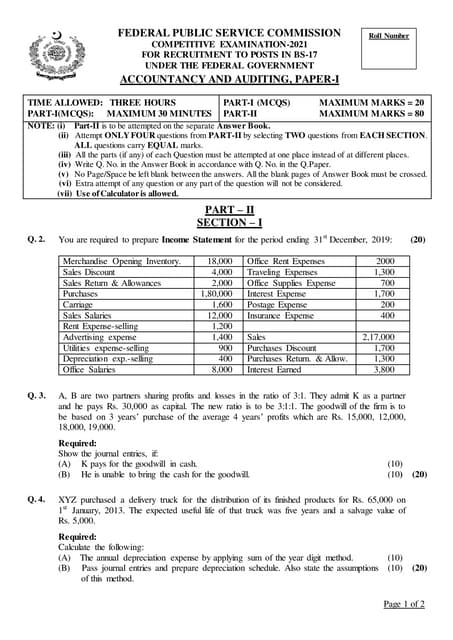

- The document provides guidance answers and valuation scheme for the IPCC exam accounting paper.

- It includes solutions to multiple questions related to computation of basic earnings per share, lease accounting, capitalization of borrowing costs, departmental trading and profit and loss accounts, foreign branch accounts, insurance company accounts, liquidator's statement of receipts and payments, and bank capital fund ratios.

- Workings and journal entries are provided with marks allocated for each part of the solutions.

![1 (b) Solution 6 Marks

(i) Calculation of Annual Lease Payment (3 Marks)

Rs

Cost of the equipment

Unguaranteed Residual Value

PV of unguaranteed residual value for 3 years @ 10%

(Rs 1,00,000 x 0.751)

Fair value to be recovered from Lease Payment

(Rs 7,46,55,100 – Rs 75,100)

PV Factor for 3 years @ 10%

Annual Lease Payment

(Rs 7,45,80,000 / PV Factor for 3 years @ 10% i.e. 2.486)

7,46,55,100

1,00,000

75,100

7,45,80,000

2.486

3,00,00,000

(ii) Unearned Finance Income (3 Marks)

Total lease payments [Rs 3,00,00,000 x 3] 9,00,00,000

Add: Residual value 1,00,000

Gross Investments 9,01,00,000

Less: Present value of Investments

(Rs 7,45,80,000 + Rs 75,100) (7,46,55,100)

Unearned Finance Income 1,54,44,900

1. (c) Solution 8 Marks

According to para 6 of AS 16 “Borrowing Costs”, borrowing costs that are directly attributable

to the acquisition, construction or production of a qualifying asset should be capitalised as part of

the cost of that asset. The amount of borrowing costs eligible for capitalisation should be

determined in accordance with this Standard. Other borrowing costs should be recognised as an

expense in the period in which they are incurred.

Also para 10 of AS 16 “Borrowing Costs” states that to the extent that funds are borrowed

specifically for the purpose of obtaining a qualifying asset, the amount of borrowing costs

eligible for capitalisation on that asset should be determined as the actual borrowing costs

incurred on that borrowing during the period less any income on the temporary investment of

those borrowings.

Thus, eligible borrowing cost

= Rs 11,00,000 – Rs 2,00,000

= Rs 9,00,000 ( 4 Marks)](https://image.slidesharecdn.com/ipccadvancedaccountingmodelexamanswerkey22-151006101959-lva1-app6891/85/Ipcc-advanced-accounting_model_exam_answer_key_22-03-2015-2-320.jpg)

![Shree Guru Kripa’s Institute of Management Accounting – IPCC

Working Notes: (2 Marks)

1. Stock of department A will be adjusted according to the rate applicable to department B =

[(7,50,000 ÷ 15,00,000) х 100] = 50%

2. Stock of department B will be adjusted according to the rate applicable to department A =

[(4,00,000 ÷ 10,00,000) х 100] = 40%

2 (b) Solution 8 Marks

In the books of ABC Ltd.

New York Branch Trial Balance in (Rs)

as on 31st March, 2015

Conversion

rate per US $

(Rs)

Dr.

Rs

Cr.

Rs

Stock on 1.4.14

Purchases and sales

Sundry debtors and creditors

Bills of exchange

Sundry expenses

Bank balance

Delhi head office A/c

40

41

42

42

41

42

–

6,000

16,400

8,400

2,520

22,140

8,820

–

–

30,750

6,300

5,040

–

–

22,190

64,280 64,280

3 (a) Solution 8 Marks

In the books of XYZ Marine Insurance Ltd

Amount (Rs)

(i) Net Premium earned

Premium from Direct Business received

Add: Receivable as on 31.03.2014

92,00,000

3,94,000

Less: Receivable as on 01.04.2013 (4,59,000)

Sub Total (A) 91,35,000

Premium on reinsurance accepted 7,86,000

Add: Receivable as on 31.03.2014 33,000

Less: Receivable as on 01.04.2013 (37,000)

Sub Total (B) 7,82,000

Premium on reinsurance Ceded 6,36,000

Add: Payable as on 31.03.2014 20,000

Less: Payable as on 01.04.2013 (28,000)](https://image.slidesharecdn.com/ipccadvancedaccountingmodelexamanswerkey22-151006101959-lva1-app6891/85/Ipcc-advanced-accounting_model_exam_answer_key_22-03-2015-4-320.jpg)

![Shree Guru Kripa’s Institute of Management Accounting – IPCC

Sub Total (C) 6,28,000

Premium Earned (A+B-C) 92,89,000

(ii) Net Claims Incurred

Claims paid on direct business 73,00,000

Add: Outstanding as on 31.03.2014 1,01,000

Less: Outstanding as on 01.04.2013 (94,000)

Sub Total (A) 73,07,000

Reinsurance claims 5,80,000

Add: Outstanding as on 31.03.2014 12,000

Less: Outstanding as on 01.04.2013 (16,000)

Sub Total (B) 5,76,000

Claims received from reinsurance 2,10,000

Add: Outstanding as on 31.03.2014 39,000

Less: Outstanding as on 01.04.2013 (42,000)

Sub Total (C) 2,07,000

Net Claim Incurred (A+B-C) 76,76,000

3 (b) Solution 8 Marks

a) Interest on loan (4 Marks)

2010-11

Rs

2011-12

Rs

2012-13

Rs

Opening Capital cost (A)

Gross Opening loan - considered at 70% of

(A)=(B)

Cumulative Repayment of Loan upto previous

year (C)

135.39

94.773

14

137.02

95.914

14.96

138

96.6

15.83

Net Loan Opening (B)-(C)=(D)

Additional capital expenditure (allowed above)

(E)

Addition of loan due to approved additional

capital expenditure - considered at 70% of

(E)=(F)

Repayment of loan during the year (net)(G) Net

Loan Closing [(D)+(F)-(G)=(H)]

Average Loan[(D)+(H)/2]=I

Weighted Average Rate of Interest on Loan (J)

Interest on Loan(I) x (J)

80.773

1.63

1.141

0.96

80.954

80.864

7.35%

5.944

80.954

0.98

0.686

0.87

80.77

80.862

7.48%

6.048

80.77

0.52

0.364

0.68

80.454

80.612

7.50%

6.046](https://image.slidesharecdn.com/ipccadvancedaccountingmodelexamanswerkey22-151006101959-lva1-app6891/85/Ipcc-advanced-accounting_model_exam_answer_key_22-03-2015-5-320.jpg)

![Shree Guru Kripa’s Institute of Management Accounting – IPCC

Risk Adjusted Assets (5 Marks)

Particulars Amount

(Rs in crores)

% of

weight

Amount

(Rs in crores)

Funded Risk Assets

Cash Balance with RBI

Balance with other Banks

Other Investments

Loans & Advances :

(i) Guranteed by Government

(ii) Others

Premises Furniture & Fixture

Total (i)

12.00

20.00

40.00

14.50

5,465.00

74.00

0

20

100

0

100

100

0.00

4.00

40.00

0.00

5,465.00

74.00

5583.00

Off Balance Sheet Items

Guarantees and other obligations 700.00 100 700.00

Acceptances, endorsements and

letter of credit 4,900.00 100 4,900.00

Total (ii) 5,600.00

Total [ (i) + (ii) ] 11183.00

Risk Weighted Assets Ratio: (1 Mark)

Capital Fund x 100

Risk Adjusted Assets

= (726.10 / 11183) x 100

= 6.49%](https://image.slidesharecdn.com/ipccadvancedaccountingmodelexamanswerkey22-151006101959-lva1-app6891/85/Ipcc-advanced-accounting_model_exam_answer_key_22-03-2015-8-320.jpg)

![Financial_statement_for_the_company[1].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/financialstatementforthecompany1-241017204922-2fcfacd7-thumbnail.jpg?width=640&height=640&fit=bounds)