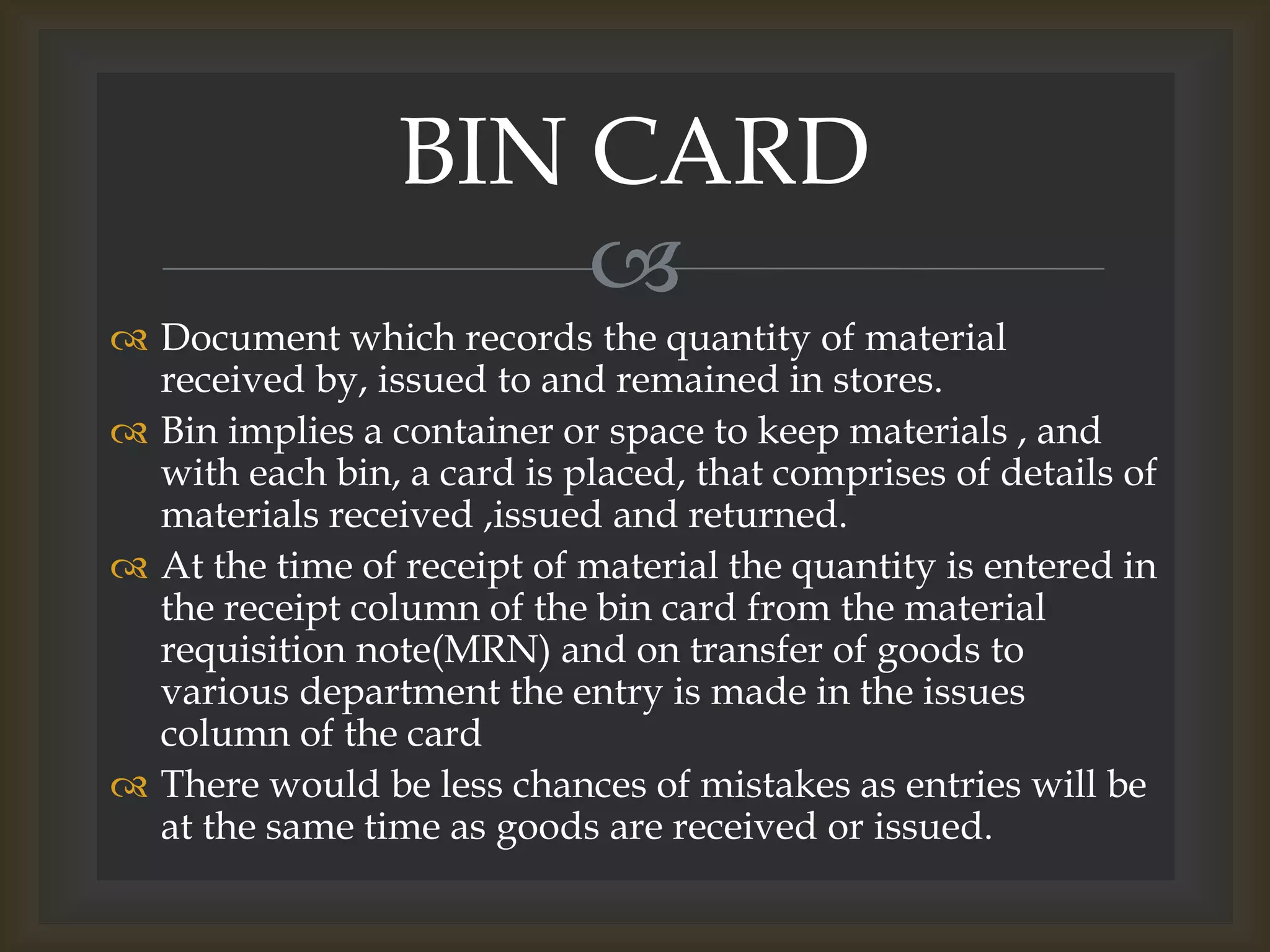

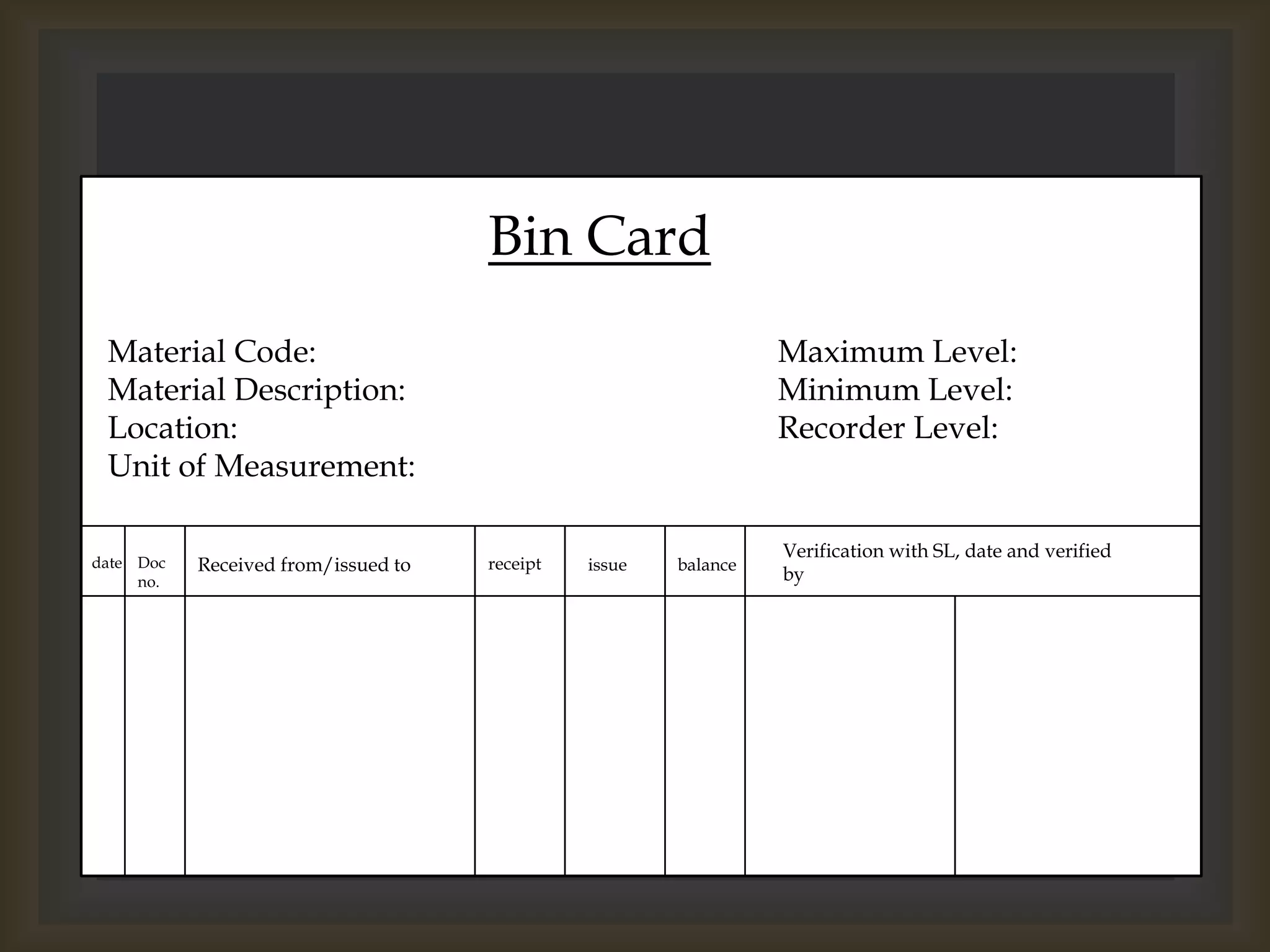

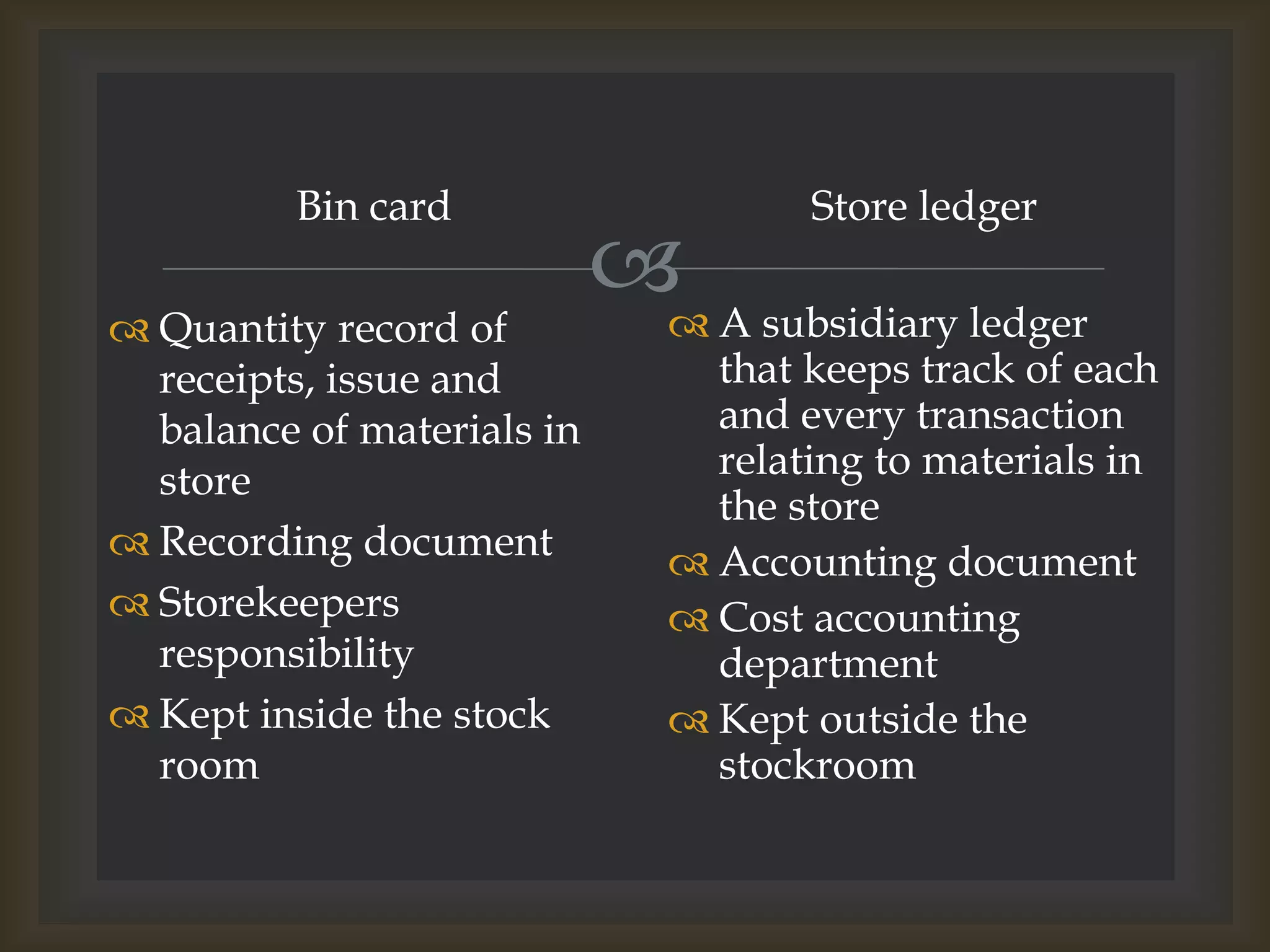

Bin cards are used to track inventory quantities and are maintained by the stores department. They record details of materials received, issued, and balances at the bin or storage location. Entries are made at the time of receipt or issue directly from material requisition notes or transfer documents. This allows for accurate and timely recording with less chances of mistakes.

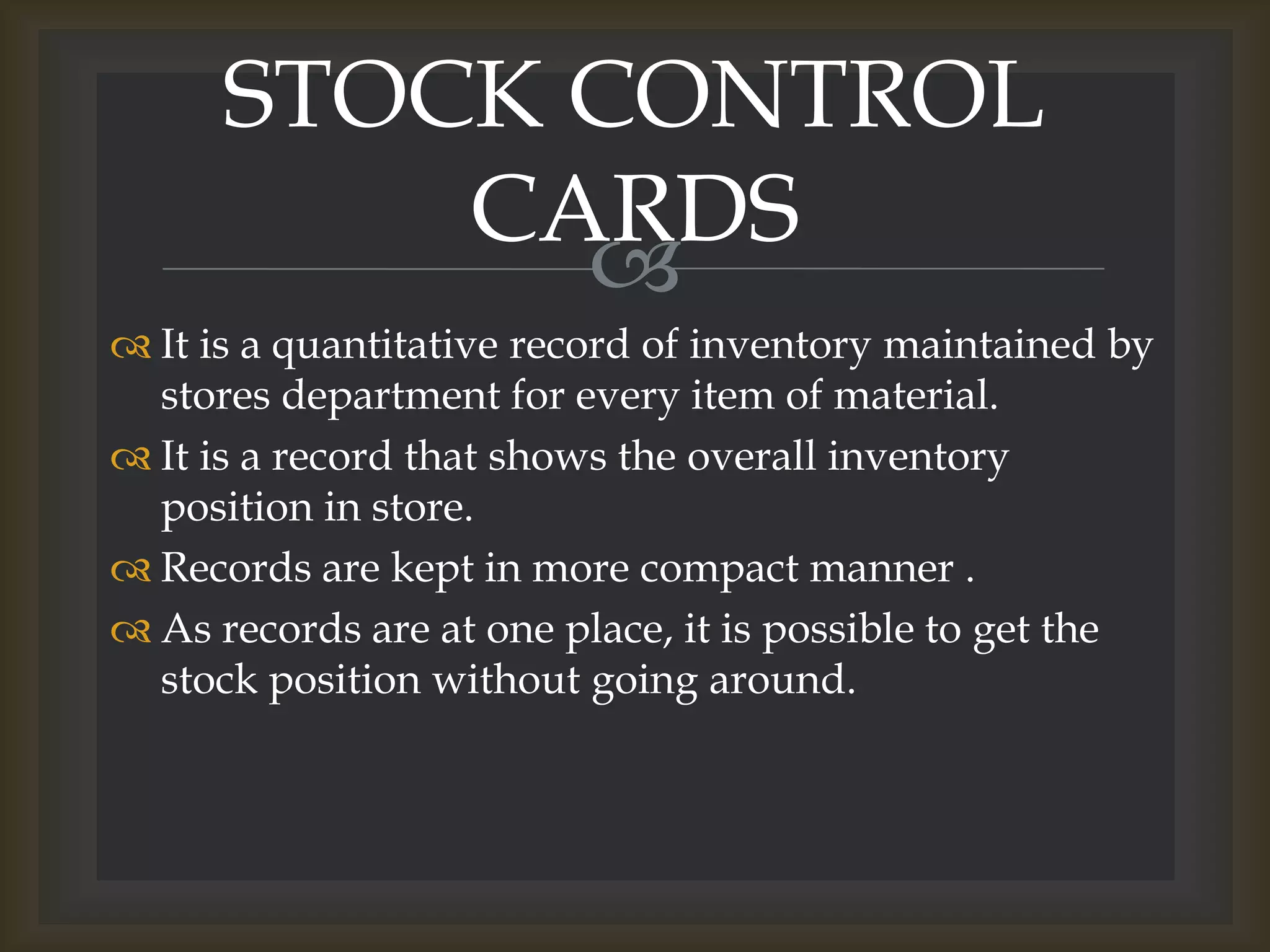

Stock control cards maintain an overall record of inventory positions within the stores. They keep track of inventory in a more compact manner and allow getting stock positions without checking individual bins.

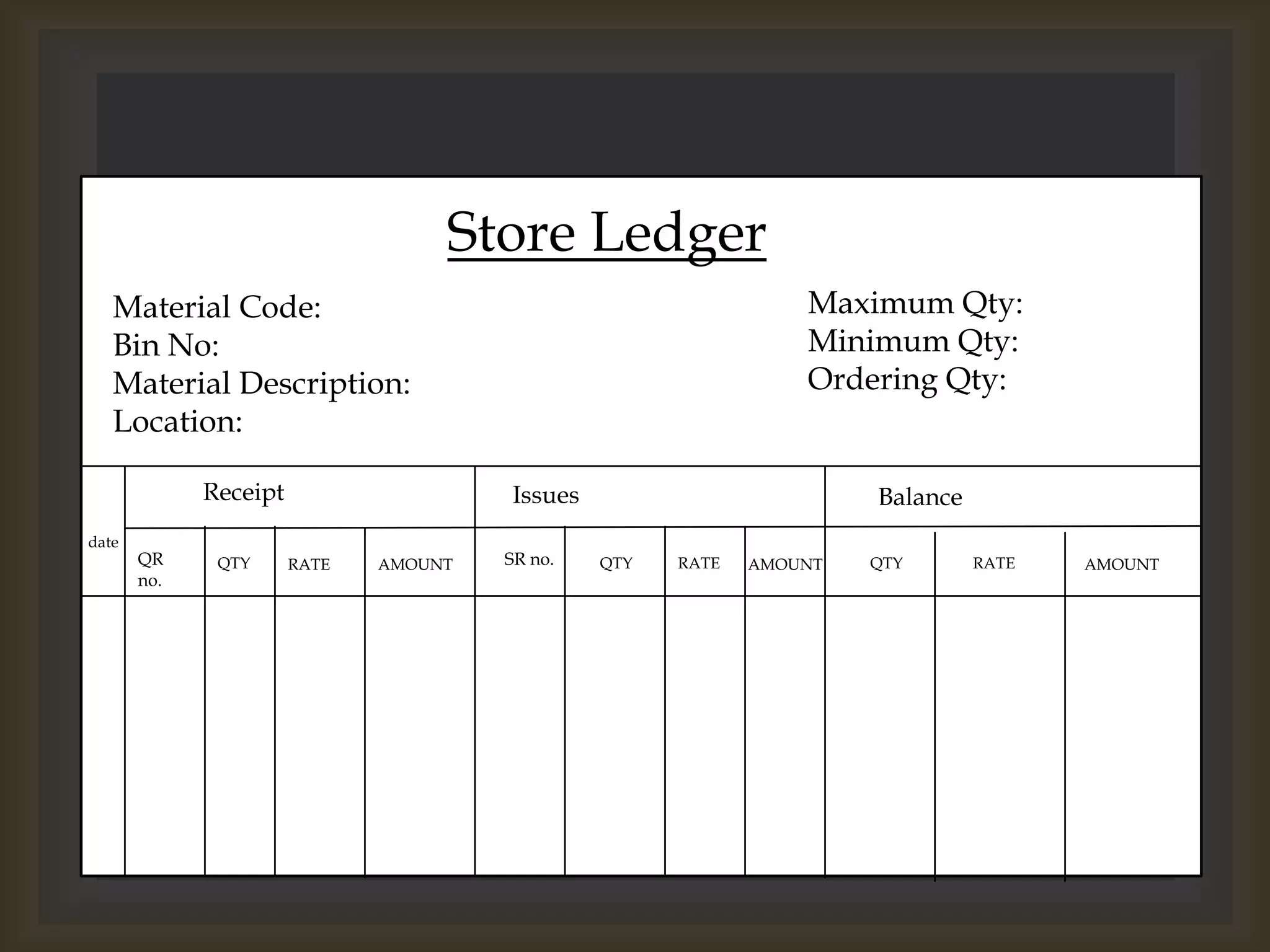

The store ledger is an accounting record that tracks inventory transactions both quantitatively and monetarily. It contains details of receipts, issues, balances, quantities, rates, and amounts for materials. It provides