Downloaded 100 times

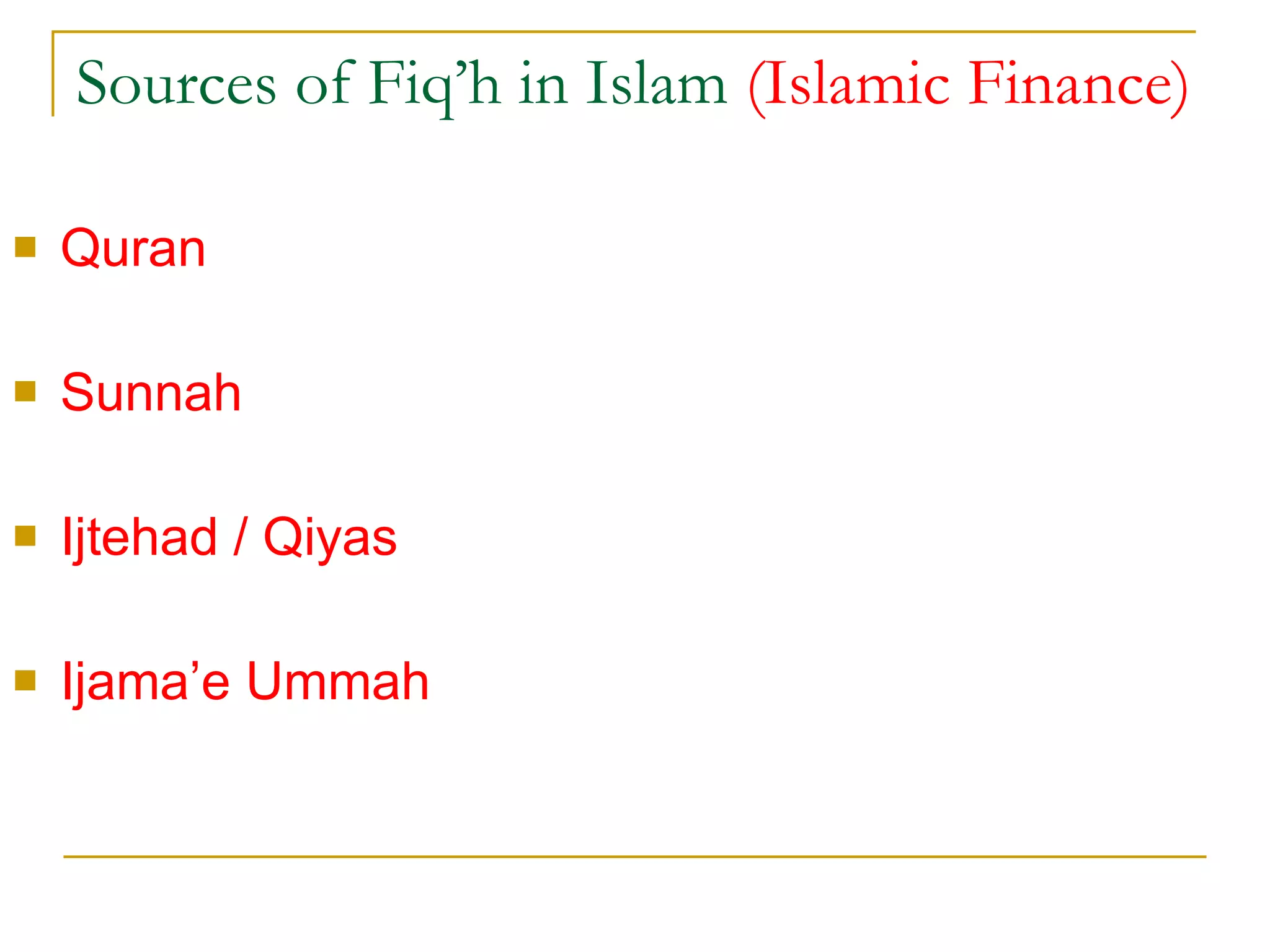

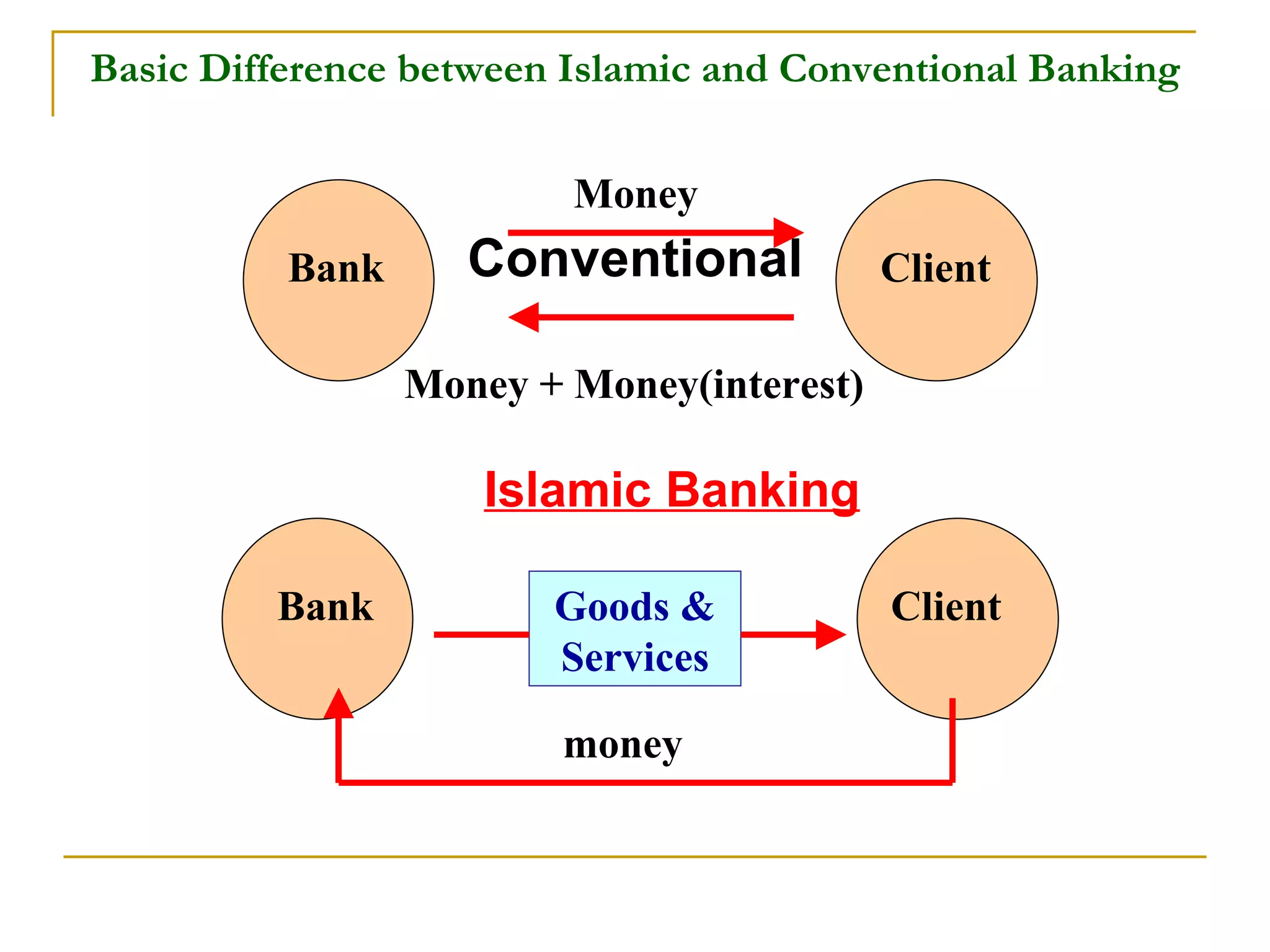

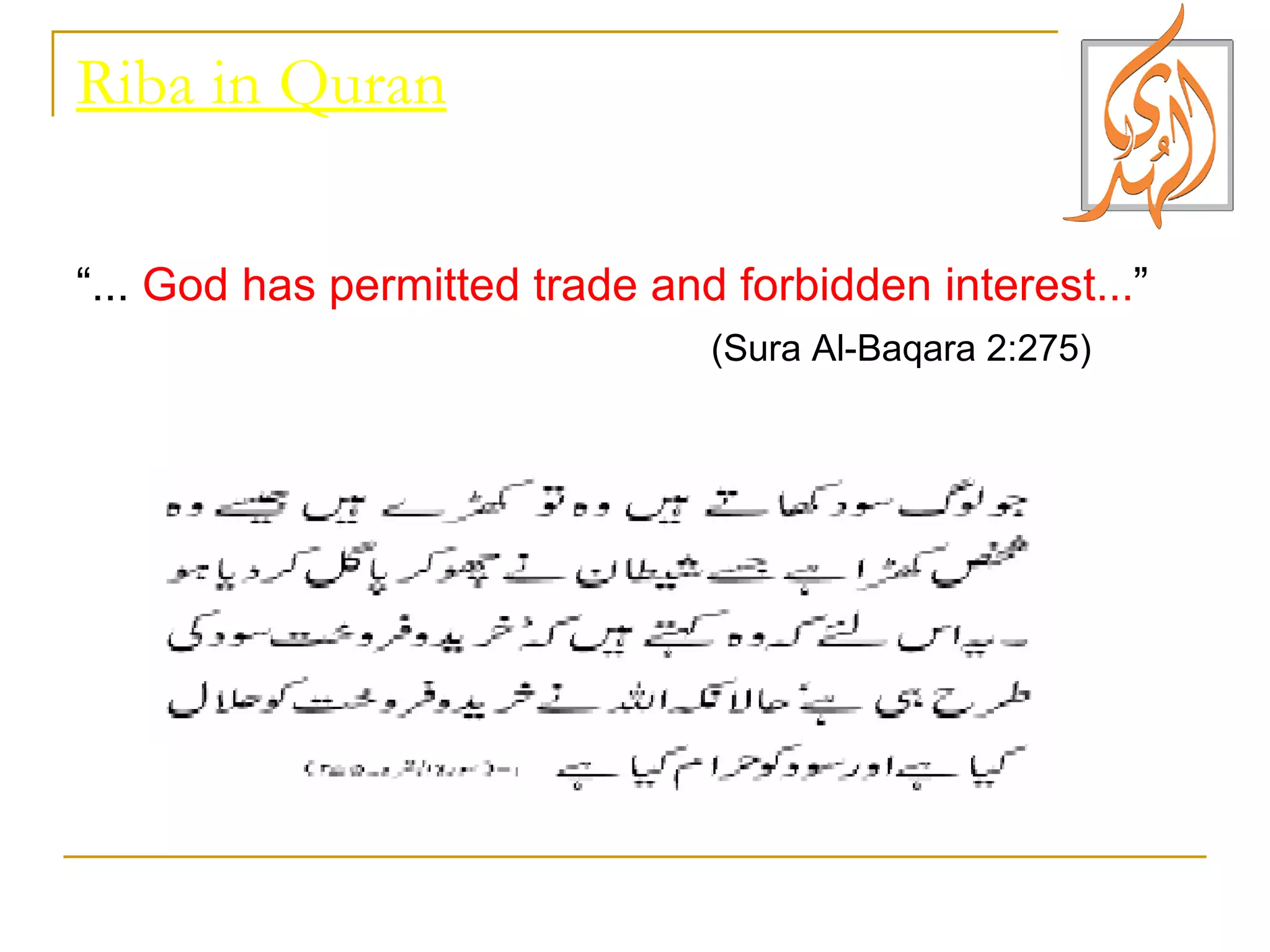

The document provides an overview of Islamic banking, including its foundations in Islamic principles, key differences from conventional banking, common Islamic banking products and financing modes, and the progress and current state of the Islamic banking industry both in Pakistan and globally. It discusses Islamic prohibitions on riba (interest), and how Islamic banks engage in trade-based, partnership-based and rental-based modes to fulfill financial needs in accordance with Shariah law.