Downloaded 315 times

![HISTORY OF ICM

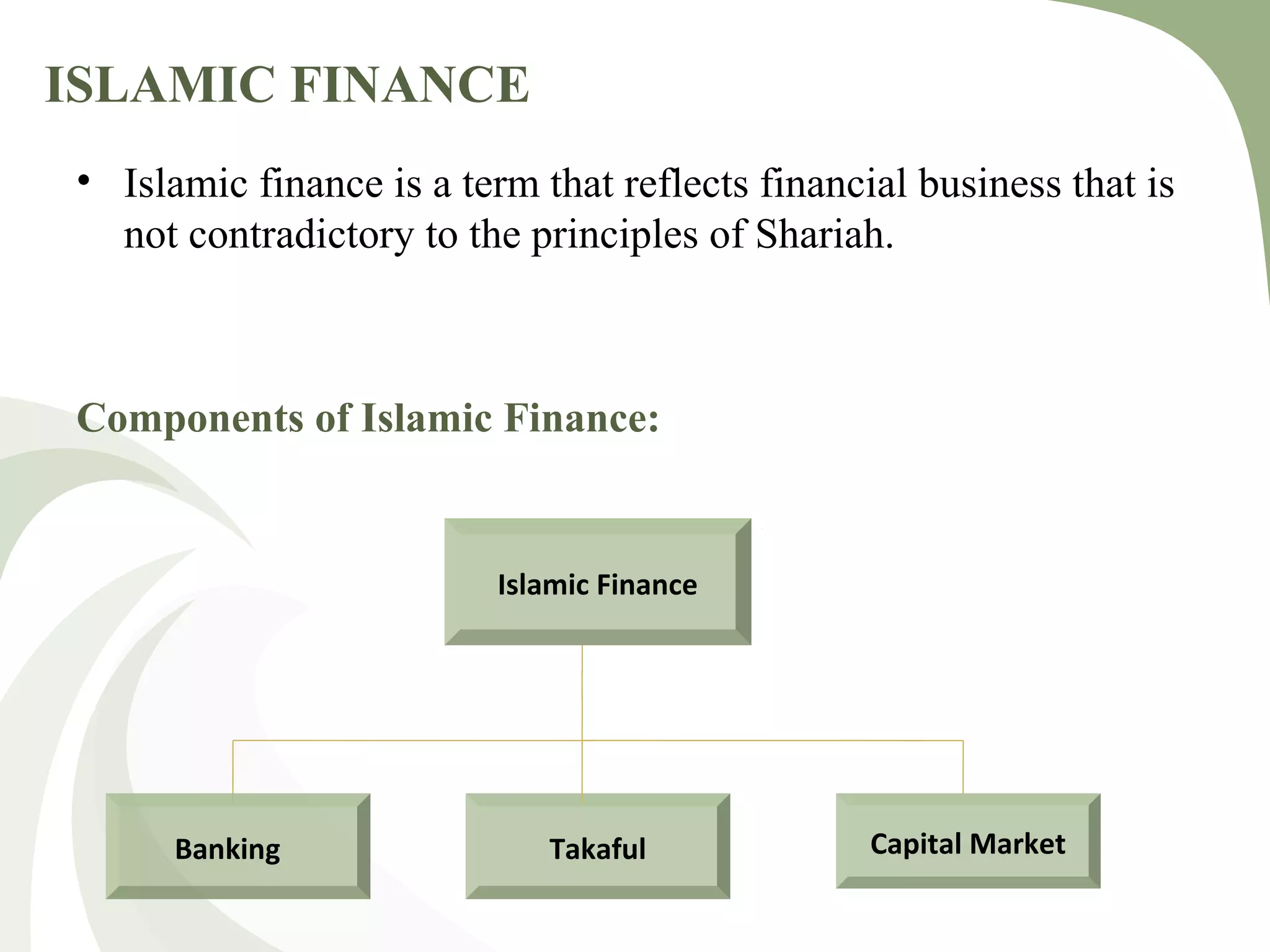

Islamic Finance starts in 1961 in Egypt by establishing the

earliest Islamic Bank [Mit Ghimar Bank]

Structured Involvement of Islamic Finance in Financial

Markets started in the decades of 1970 and 1980’s by

establishing many Islamic Banks, Takaful and Investment

companies.

Boost in Islamic Capital Markets came after financial

liberalization. ICM started in 1980s in Malaysia while in

Bahrain, Pakistan and some other countries in early 1990s](https://image.slidesharecdn.com/islamiccapitalmarkets-150922065049-lva1-app6892/75/Islamic-Capital-Markets-7-2048.jpg)

![STANDARDISING And REGULATORY

AUTHORITIES

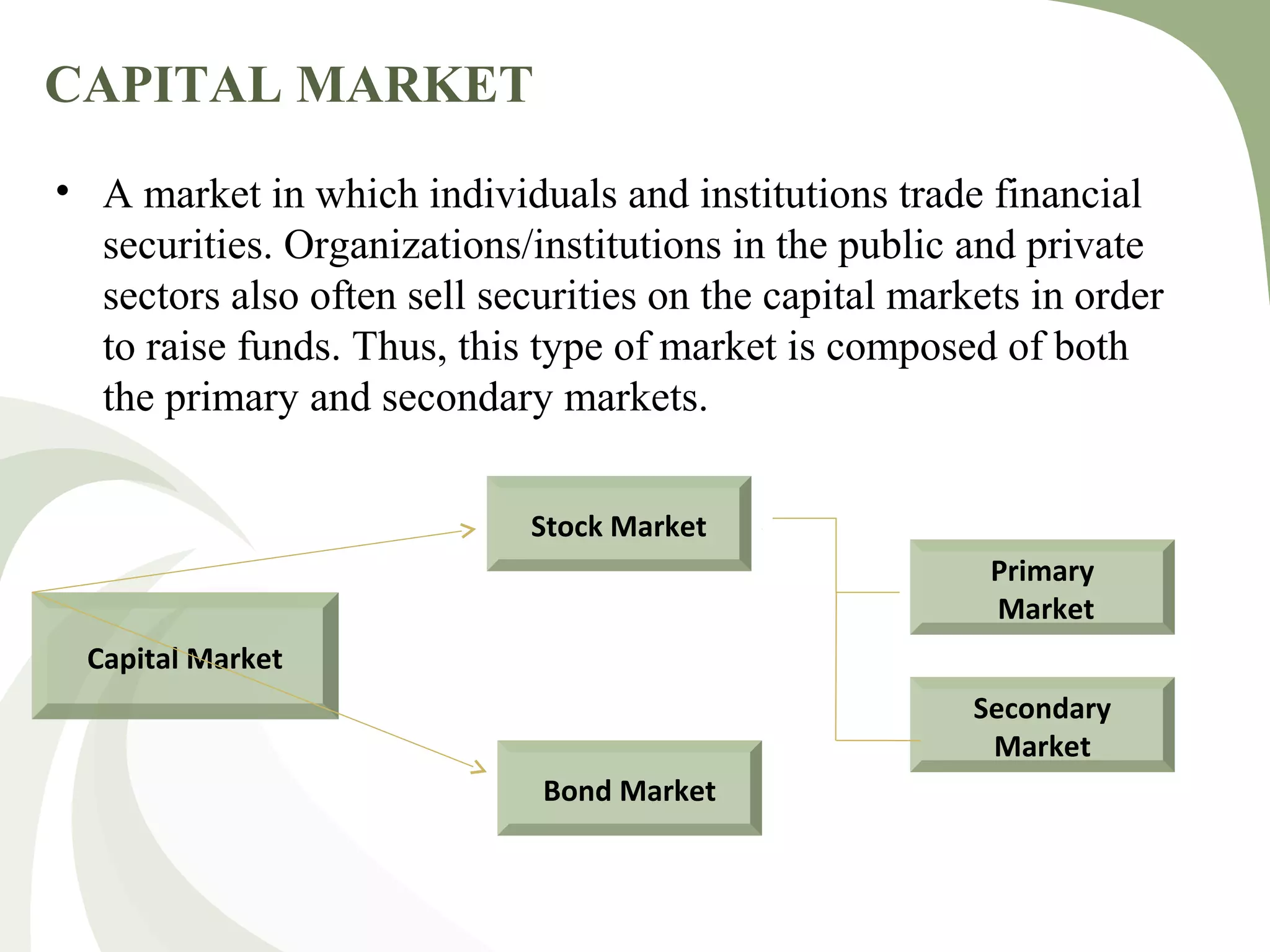

International Islamic Financial Market (IIFM) [2002]

Its primary focus lies in the standardization of Islamic financial

products, documentation and related processes at the global level.

The Islamic Financial Services Board (IFSB) [2003]

It is an international standard-setting organization that promotes

and enhances the soundness and stability of the Islamic financial

services industry by issuing global prudential standards and

guiding principles for the industry, broadly defined to include

banking, capital markets and insurance sectors.](https://image.slidesharecdn.com/islamiccapitalmarkets-150922065049-lva1-app6892/75/Islamic-Capital-Markets-11-2048.jpg)

![STANDARDISING And REGULATORY

AUTHORITIES Cont…….

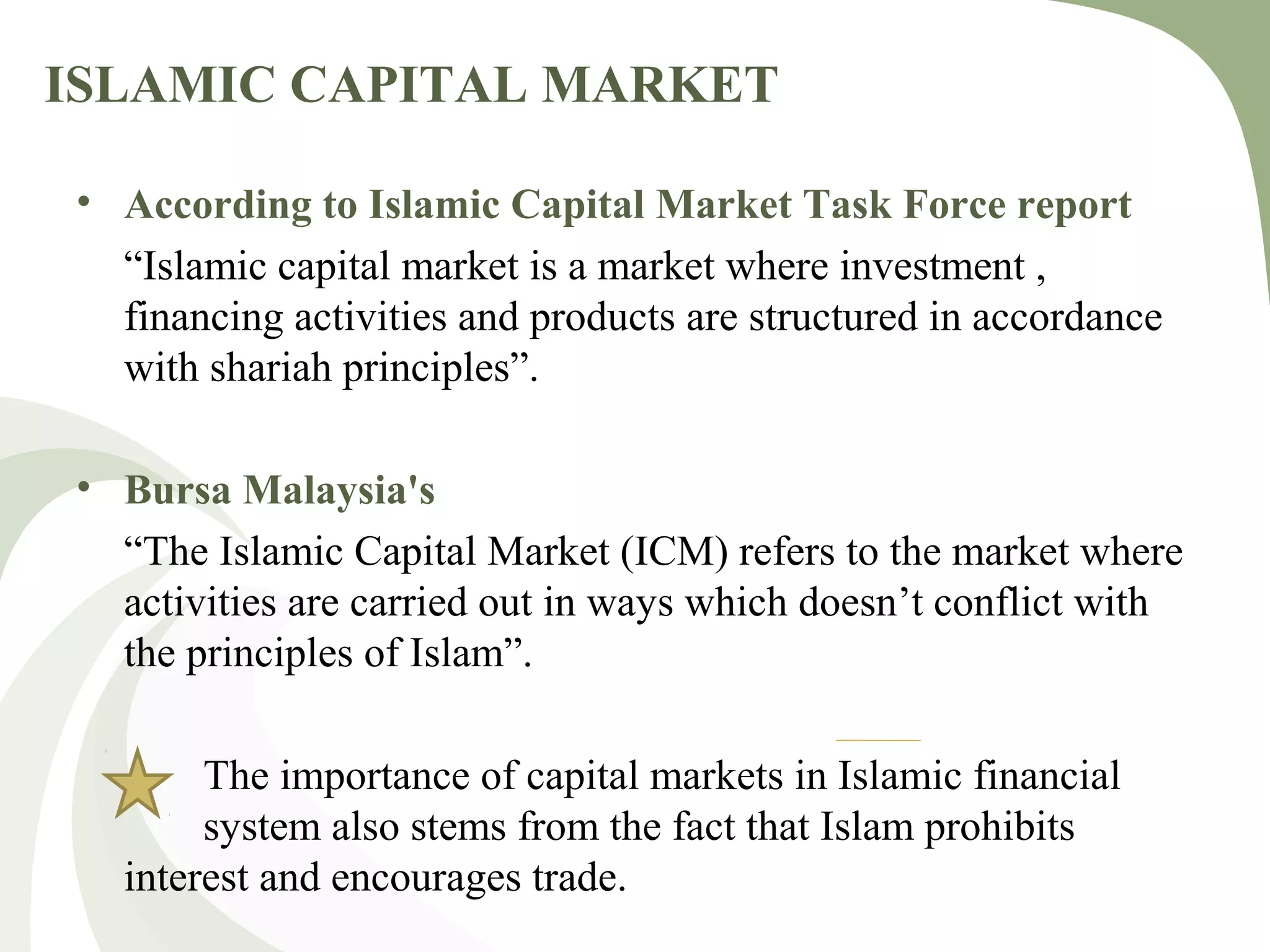

The Shariah board [2003]

It has the responsibility for ensuring that all products and services

offered by that institution are compliant with the principles of

Shariah law

The Accounting and Auditing Organization for Islamic

Financial Institution. (AAOIFI) [1990]

It sets compliance standards for institutions that wish to gain

access to the Islamic banking market.](https://image.slidesharecdn.com/islamiccapitalmarkets-150922065049-lva1-app6892/75/Islamic-Capital-Markets-12-2048.jpg)

![STANDARDISING And REGULATORY

AUTHORITIES Cont…….

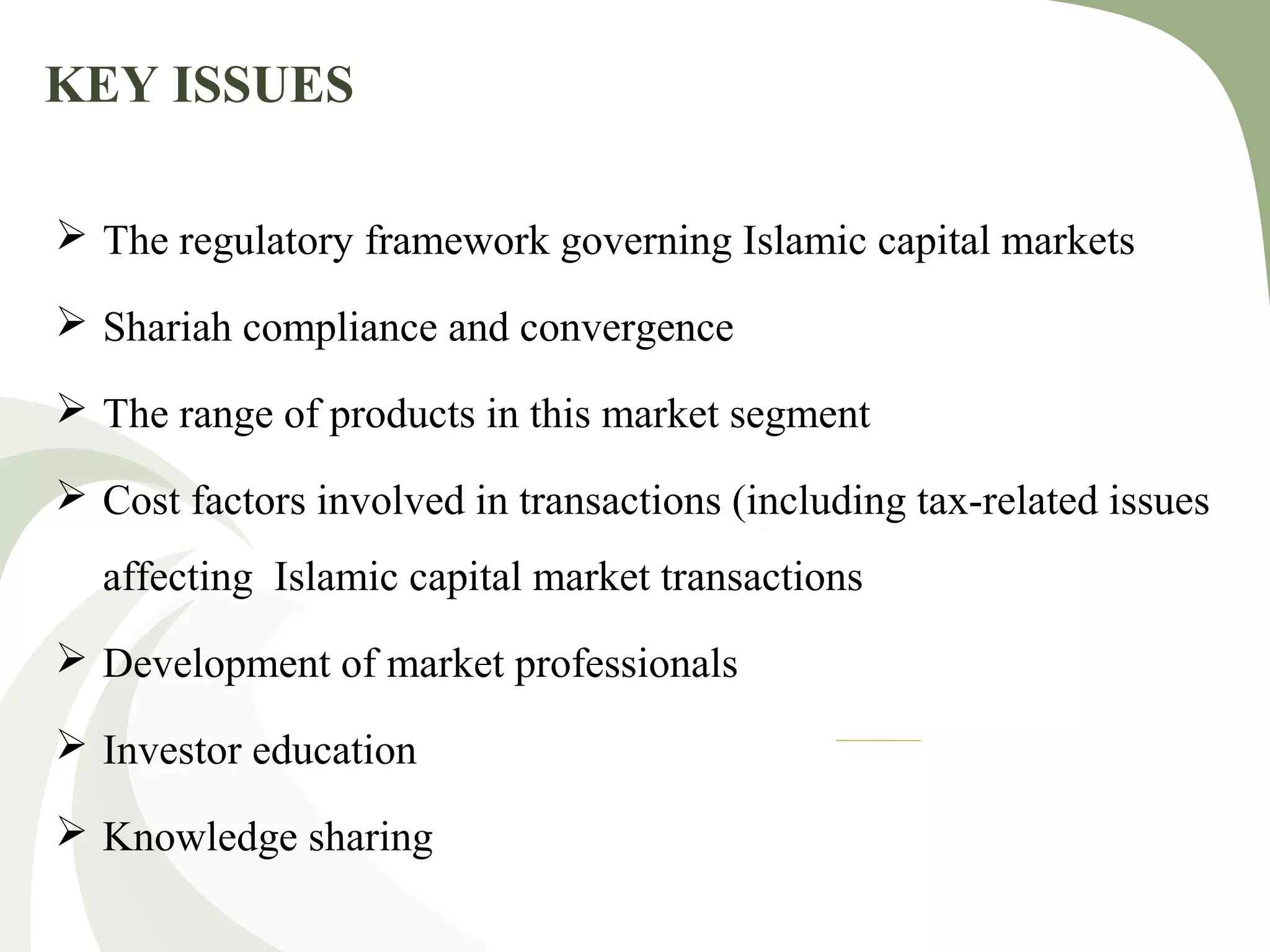

The Islamic capital markets Task Force of the International

Organization of Securities Commission (IOSCO)

It assist relevant regulators in assessing the extent of the

development and potential regulatory issues relating to Islamic

Capital Market, as well as to gather information on Islamic

financial products.

The International Islamic Rating Agency (IIRA) [2002]

evaluate and provide independent assessments and opinions on

the likelihood of any future loss by Islamic Financial Institutions,](https://image.slidesharecdn.com/islamiccapitalmarkets-150922065049-lva1-app6892/75/Islamic-Capital-Markets-13-2048.jpg)

The document provides a comprehensive overview of Islamic capital markets, detailing their foundation in Shariah principles and their growth since the establishment of the first Islamic bank in 1961. It discusses the components, functions, and development challenges of these markets, as well as the role of various regulatory authorities in standardizing Islamic financial products. Key issues include regulatory frameworks and investor education, with suggestions for addressing these through capacity building and market development initiatives.