Downloaded 163 times

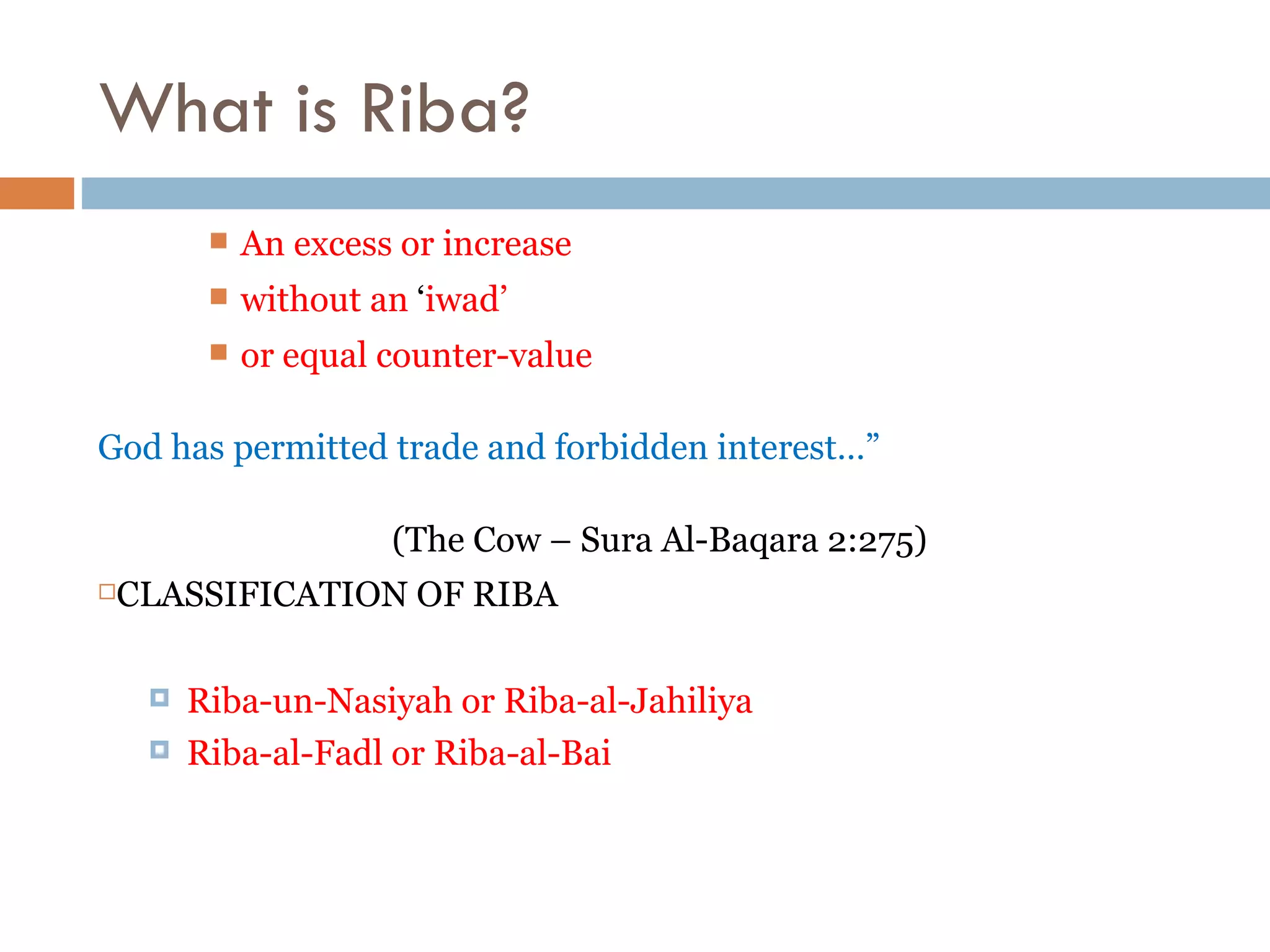

![…why From Hazrat Jabir Ibn-e-Abdullah (RA): The Prophet, peace be on him, cursed : The receiver and the payer of interest, The one who records it and The witnesses to the transaction And said: " They are all alike [in guilt]." (Muslim, Tirmidhi and Musnad Ahmad)](https://image.slidesharecdn.com/alhudapresentationonislamicbankingmissiramsaba-110103071601-phpapp01/75/Al-huda-presentation-on-islamic-bankingmiss-iram-saba-4-2048.jpg)

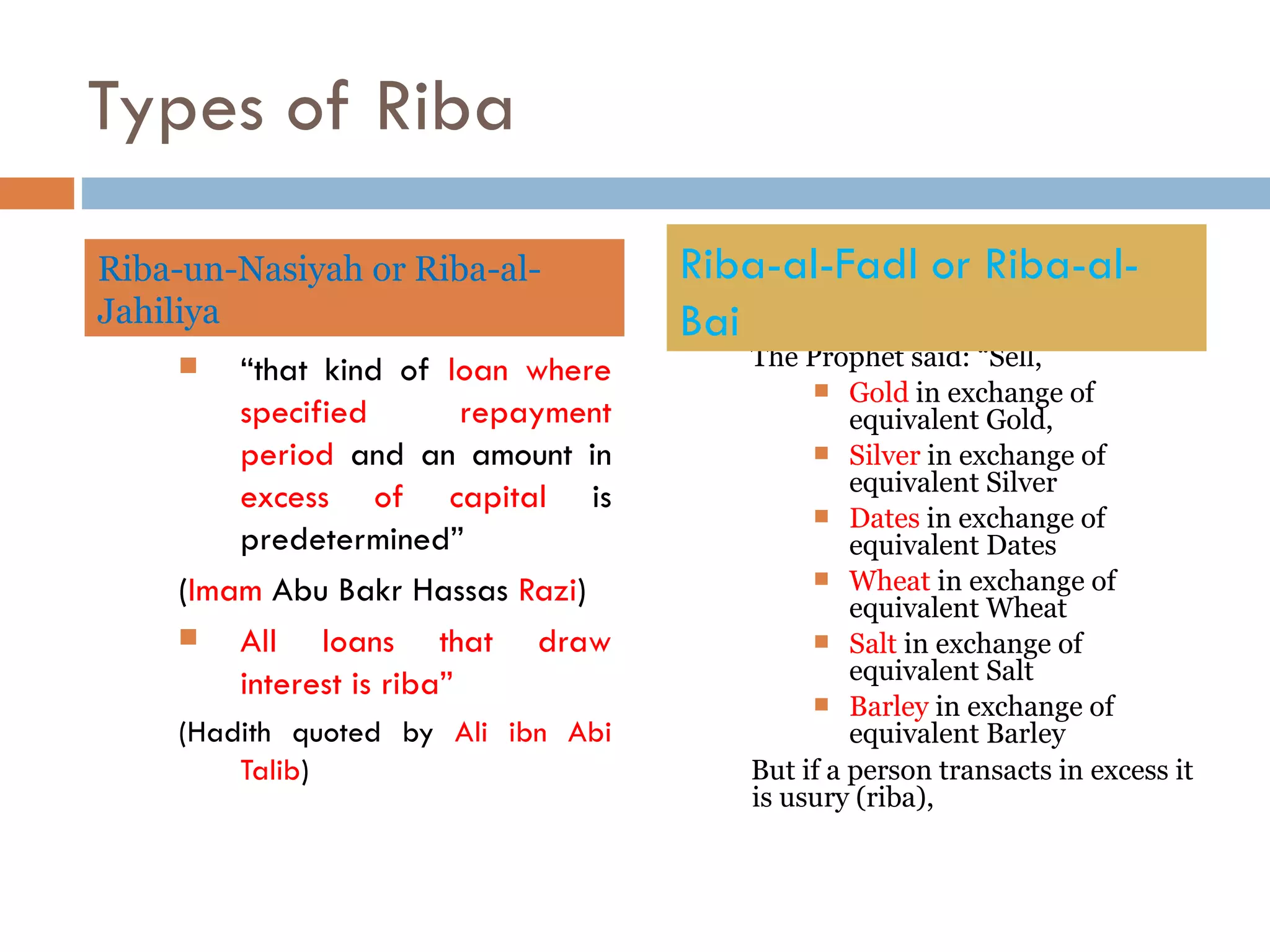

![…why ? Objectives Resolution First major step in framing a constitution was the passage by the Constituent Assembly of the Objectives Resolution of March 1949 , which defined the basic principles of the new state. It provided that Pakistan would be a state "wherein the principles of democracy, freedom, equality, tolerance and social justice, as enunciated by Islam , shall be fully observed; wherein the Muslims shall be enabled to order their lives in the individual and collective spheres in accordance with the teachings and requirements of Islam as set out in the Holy Qur'an and Sunnah ; [and] wherein adequate provision shall be made for the minorities freely to progress and practice their religions and develop their cultures."](https://image.slidesharecdn.com/alhudapresentationonislamicbankingmissiramsaba-110103071601-phpapp01/75/Al-huda-presentation-on-islamic-bankingmiss-iram-saba-5-2048.jpg)

The document provides an overview of Islamic banking in Pakistan, including its history, current state, and key features that distinguish it from conventional interest-based banking. It notes that Islamic banking grew gradually in Pakistan starting in the 1970s-80s due to various efforts, with the current strategy involving full-fledged Islamic banks, Islamic banking subsidiaries, and standalone branches. Today, Islamic banking is available across major cities in Pakistan through 6 full-fledge banks and 13 conventional banks with Islamic banking divisions comprising over 500 branches in total.

![Lecture-Slides [Autosaved].ppt Islamic banking](https://cdn.slidesharecdn.com/ss_thumbnails/lecture-slidesautosaved-250225053236-7e285f6e-thumbnail.jpg?width=640&height=640&fit=bounds)