Downloaded 61 times

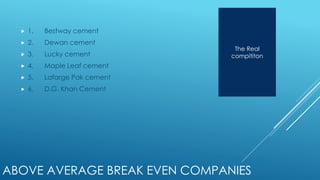

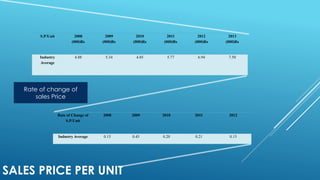

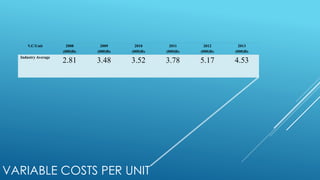

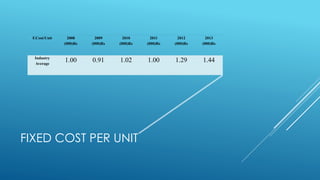

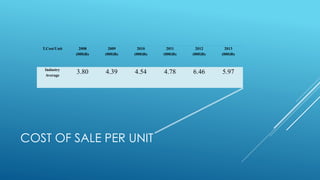

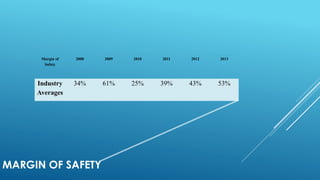

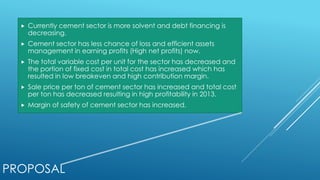

The document discusses a capital budgeting proposal for expanding a cement industry in Pakistan. It begins by outlining the project steps, including investment screening, capital budget proposal, tracking, and auditing. It then analyzes opportunities and threats in the cement industry, including factors like existing cartels and resource availability. Porter's Five Forces model is applied to the industry. Selection criteria are listed and the capital budget methodology is outlined. Cost analyses are presented for the cement sector from 2008-2013, showing trends in sales price, costs, margins, and capacity. Finally, a proposal is made to incorporate a new company, obtain necessary registrations and approvals, and present the capital budget to the CEO for approval.