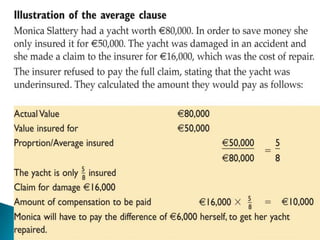

Insurance protects individuals and businesses from financial loss by paying compensation for damage to or loss of property and for legal liability resulting from negligence or injury to other people. It works by pooling risks among many insured entities, collecting fees from those insured and paying out claims to those who suffer losses from pooled risks. There are several principles that govern insurance, including insurable interest, utmost good faith, indemnity, contribution, subrogation and average clause.

![87356964 introduction-to-insurance[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87356964-introduction-to-insurance1-121105111440-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)