Download to read offline

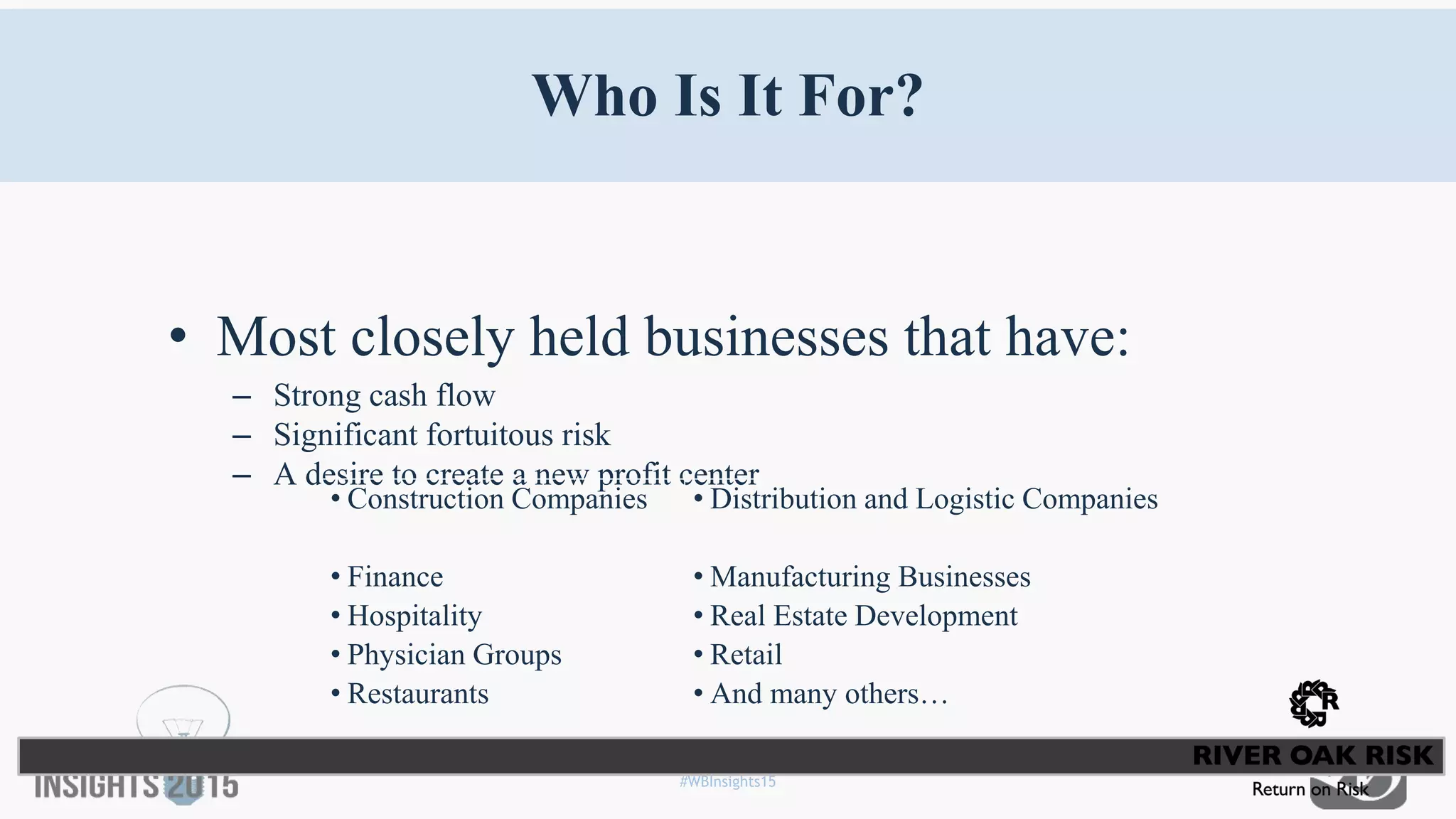

This document discusses captive insurance companies, which are insurance companies formed by businesses to insure their own risks or the risks of affiliated businesses. Captive insurance companies allow businesses to insure risks that are not covered by traditional commercial insurance, retain underwriting profits, take advantage of tax incentives, and provide asset protection and estate planning benefits. The document outlines how captive insurance companies work, the types of businesses that may benefit from them, requirements for legitimate captive insurance companies, and examples of policies that could be issued by captive insurers for different types of businesses.

![Aba On Captives[1]](https://cdn.slidesharecdn.com/ss_thumbnails/abaoncaptives1-13105274119087-phpapp01-110712222513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)