Downloaded 98 times

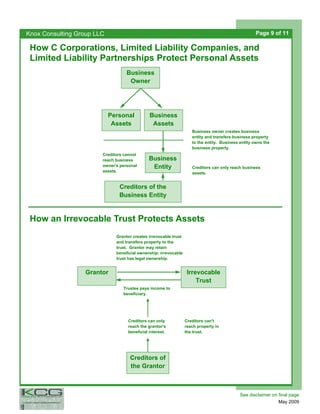

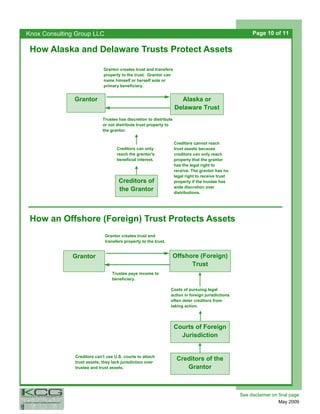

This document provides an overview of asset protection strategies. It discusses identifying risks, implementing plans before problems arise, and avoiding fraudulent transfers. It then summarizes three basic techniques: insurance to shift risks, statutory protections of exempt assets like a home, and asset placement by transferring ownership. Placement options include corporations, partnerships, trusts, and shifting assets between spouses to protect from each other's creditors.

![Six Sigma[1]](https://cdn.slidesharecdn.com/ss_thumbnails/six-sigma14148-thumbnail.jpg?width=640&height=640&fit=bounds)

![Internationalisation ppt [repaired 2]](https://cdn.slidesharecdn.com/ss_thumbnails/internationalisationpptrepaired2-111004174032-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)