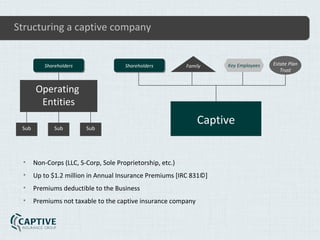

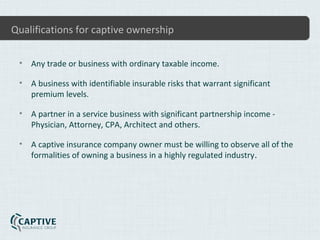

![Insuring “Other” Business Risks

• Forming a captive insurance company (CIC) offers solutions for covering

uninsured risks for many companies.

Actuarially determines insurable risks and prices the risk.

A CIC is formed in a state or territorial domicile that is favorable for the

business operation.

A CIC provides additional coverage and is not intended to replace current

property and casualty coverage.

A CIC is eligible for up to $1.2 million in annual insurance premium [IRC

831(b)].

A CIC is required to be professionally managed to ensure regulatory and IRS

compliance.

Captive Insurance Group, LLC provide professional services for ongoing

management of captive insurance companies.](https://image.slidesharecdn.com/captiveinsurancegroup-121214104645-phpapp02/85/Captive-Insurance-Group-A-Risk-Management-Strategy-4-320.jpg)

This document introduces captive insurance companies as a risk management strategy that can cover uninsured risks of businesses, including various operational and financial risks. It outlines the benefits, tax treatment, and requirements for establishing a captive insurance company, alongside the professional services provided by Captive Insurance Group, LLC for ongoing management. The document also emphasizes the importance of compliance with regulatory standards and the potential for favorable tax implications for distributions from a captive.

![Aba On Captives[1]](https://cdn.slidesharecdn.com/ss_thumbnails/abaoncaptives1-13105274119087-phpapp01-110712222513-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)