Download as PDF, PPTX

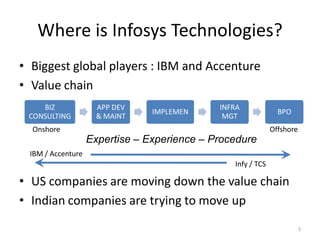

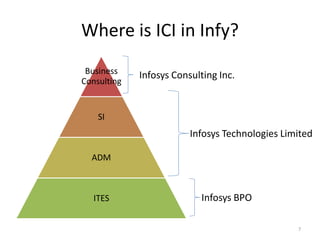

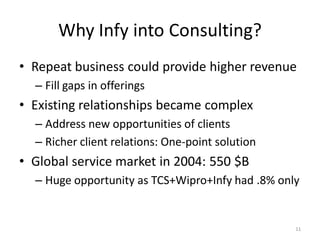

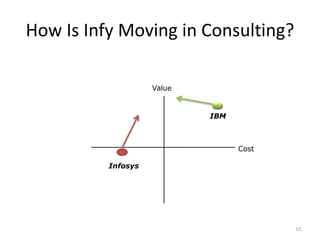

Infosys Consulting (ICI) was established in 2006 to expand Infosys' presence in the global business consulting market. While ICI aimed to leverage Infosys' Global Delivery Model (GDM) of offshore resources, integrating consulting services posed challenges due to differences in culture and business models between ICI and Infosys Technologies Limited (ITL). To compete effectively, ICI would need to establish its brand, deliver higher value beyond cost savings, and strengthen integration with ITL over the long term.