Downloaded 925 times

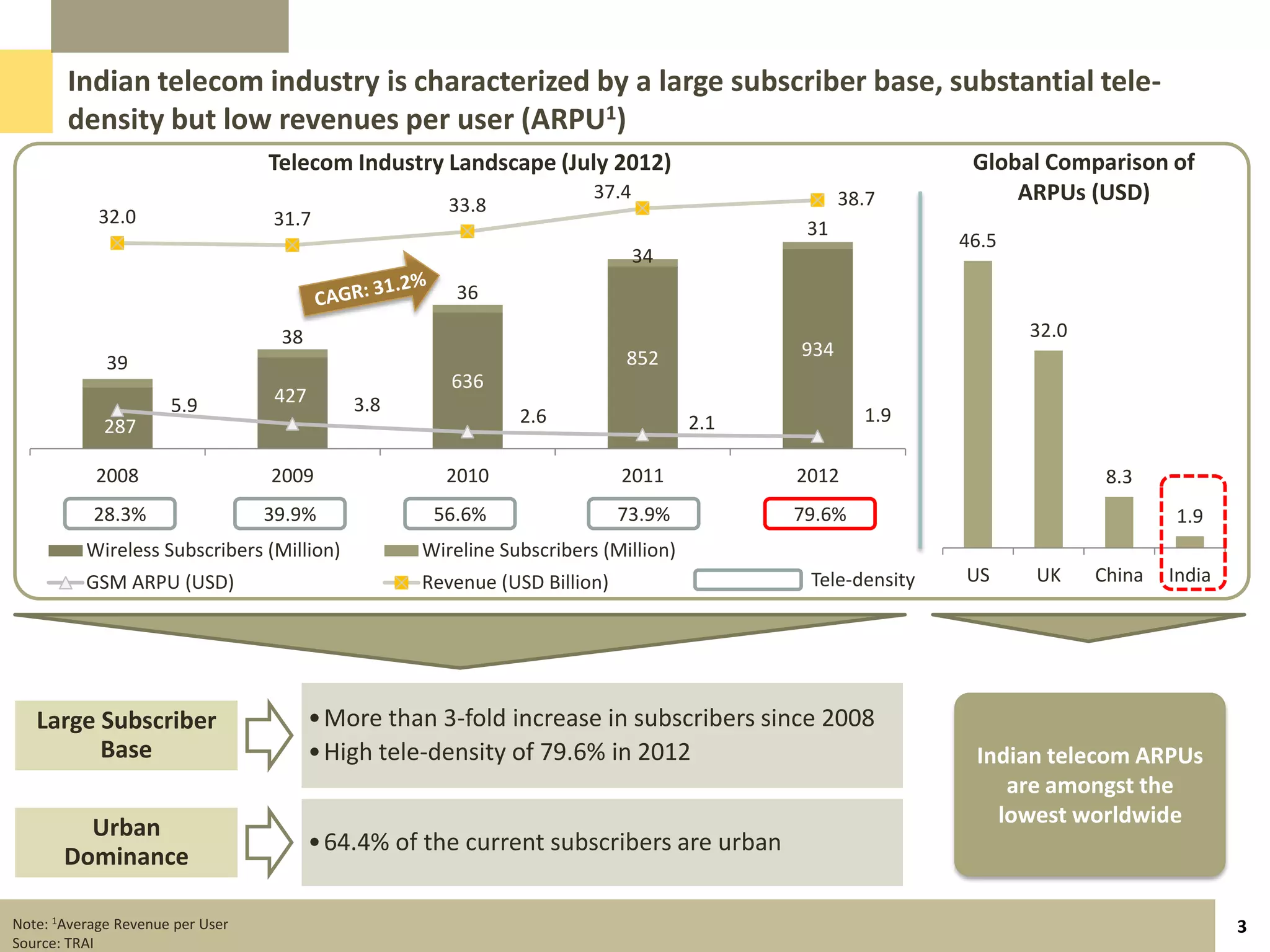

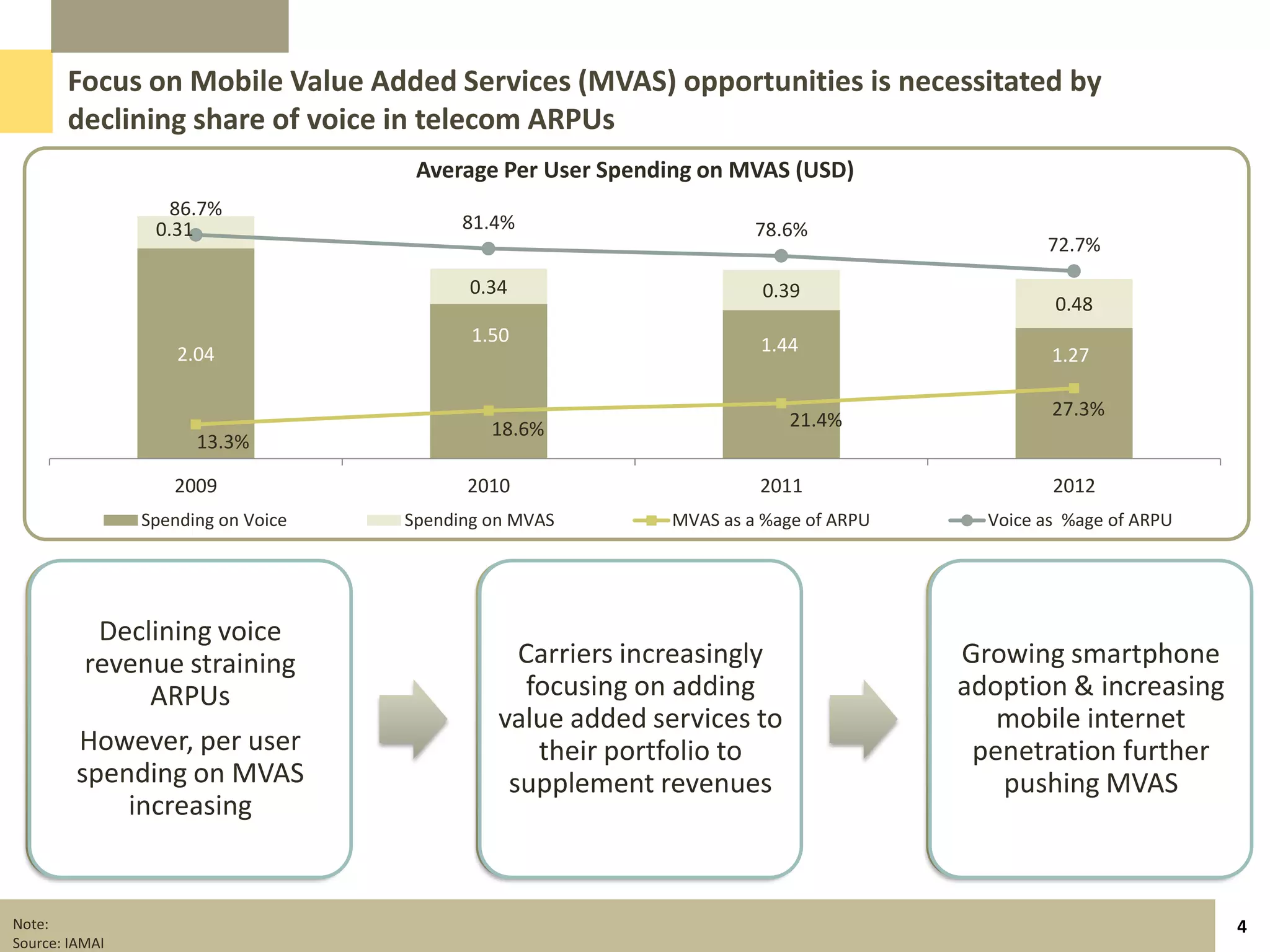

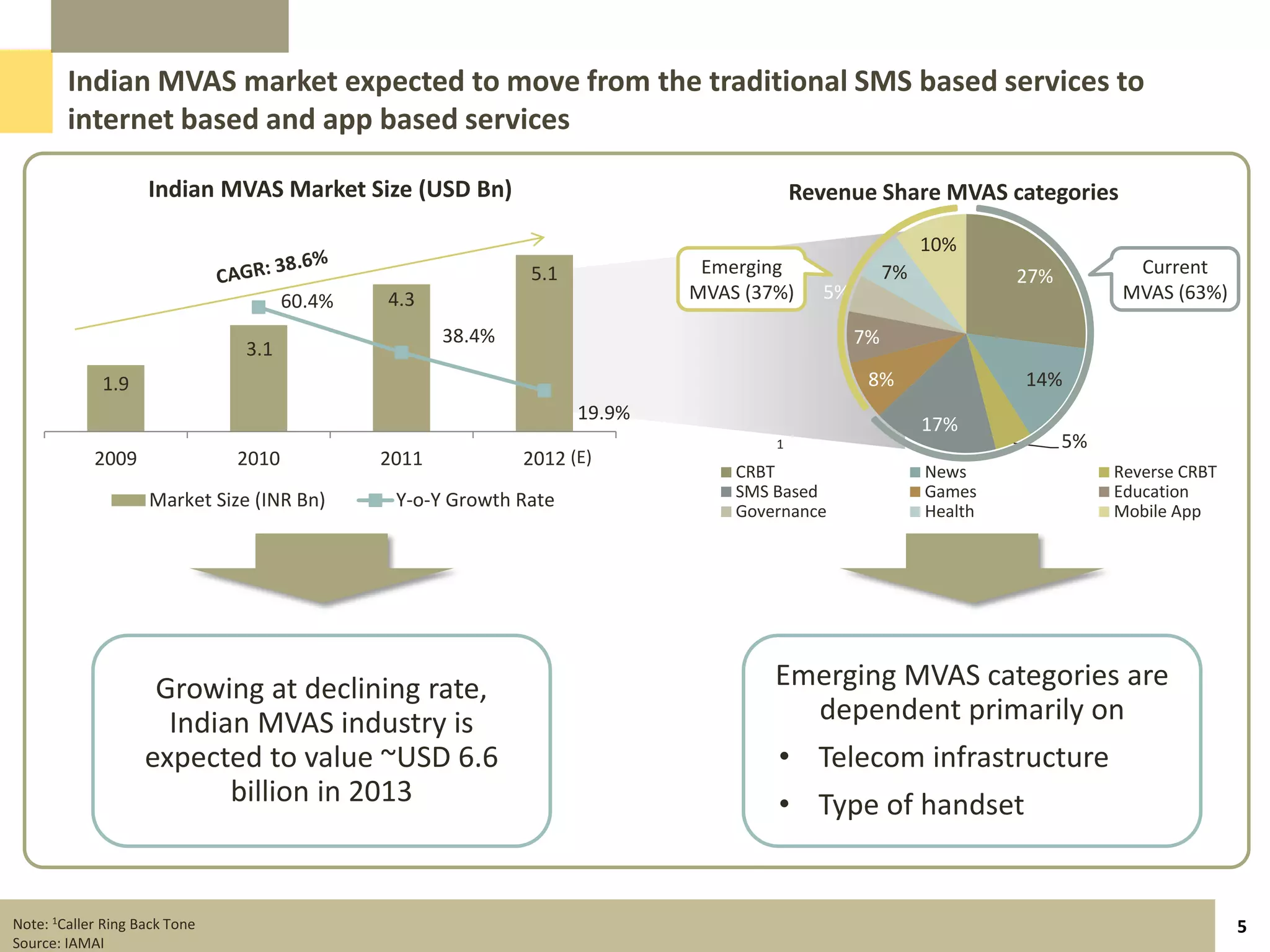

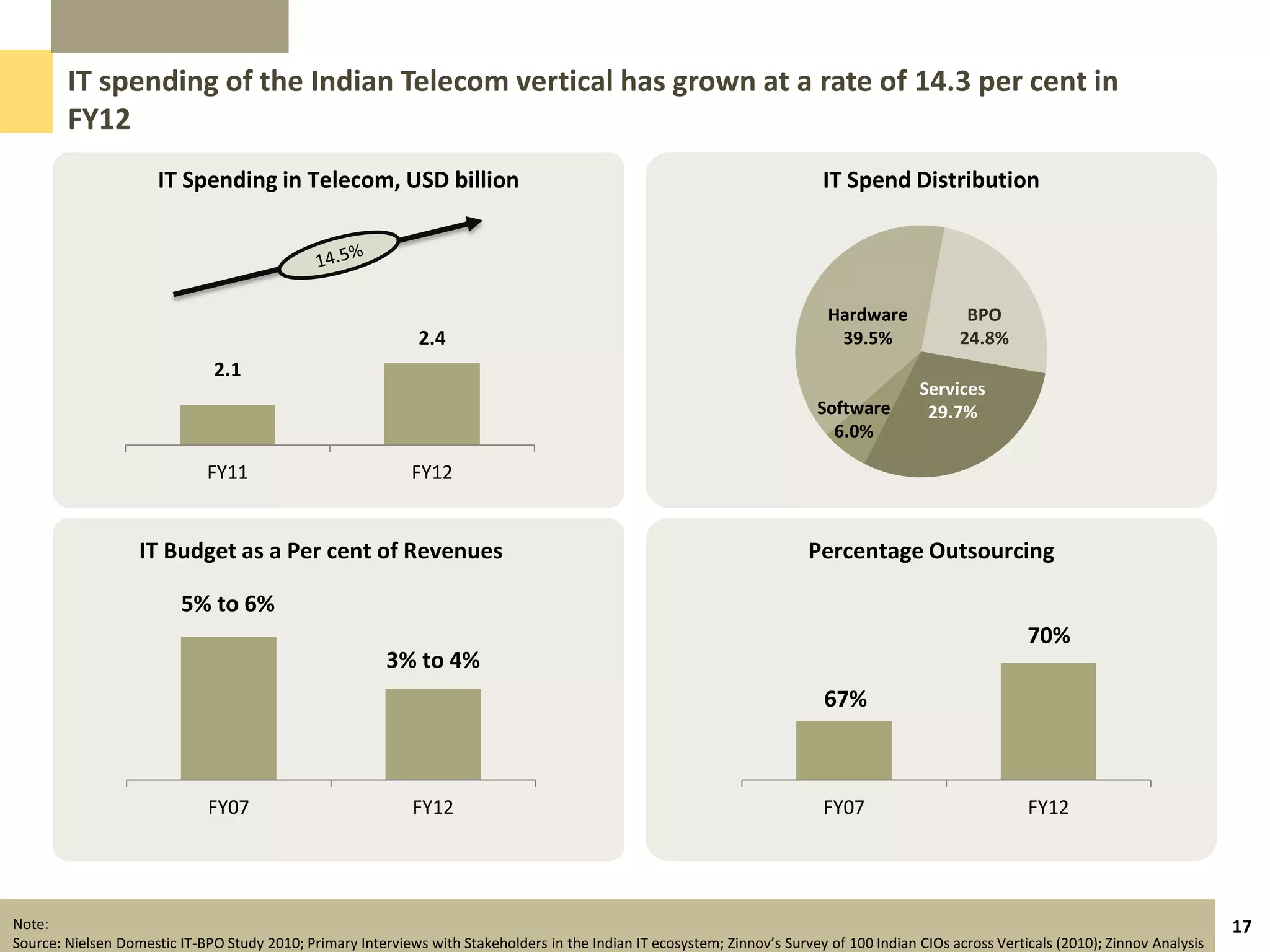

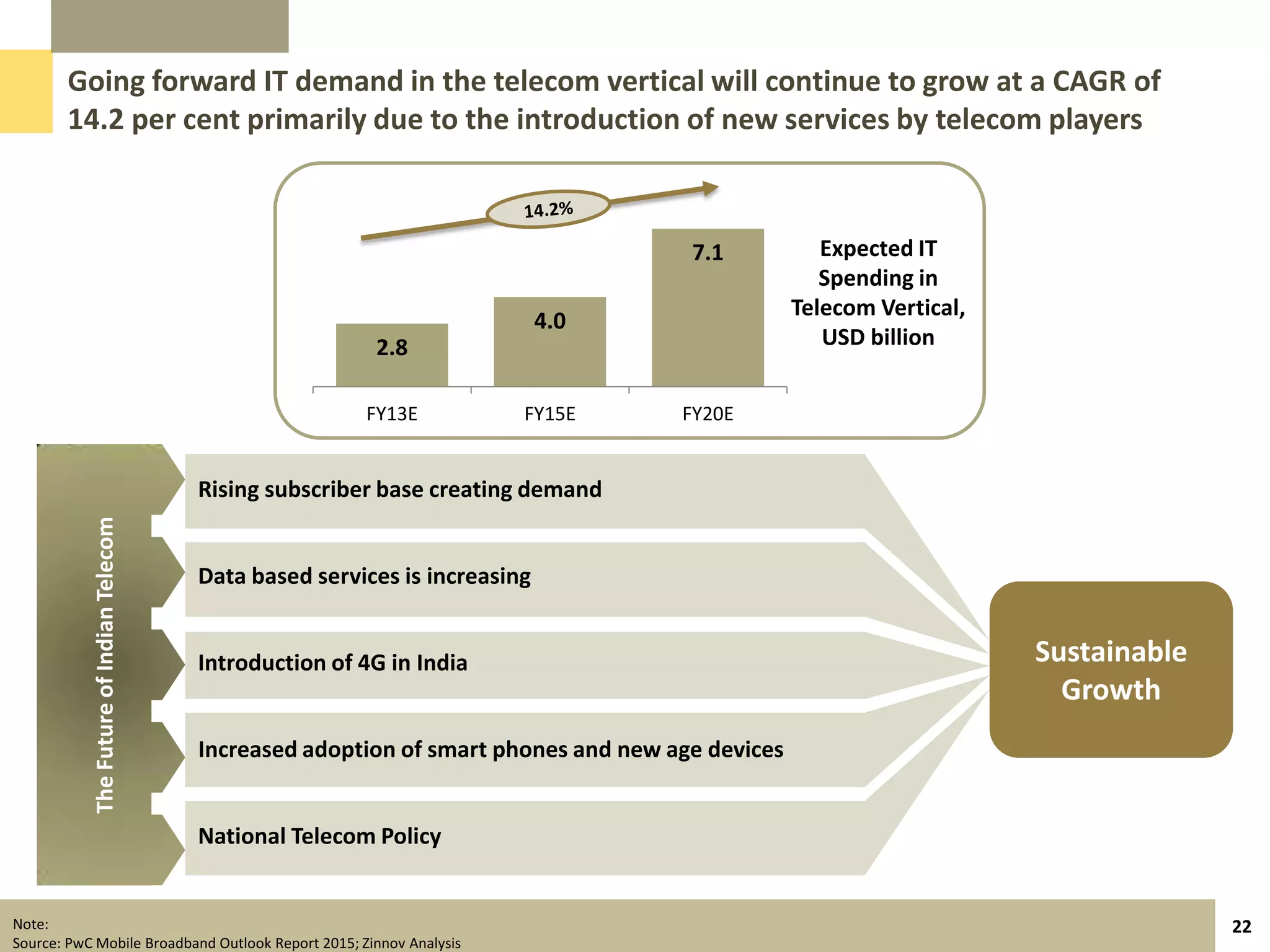

The document provides an overview of the Indian telecom market as of October 2012, highlighting a large subscriber base and high tele-density but low average revenue per user. Key trends include a shift towards mobile value-added services amidst declining voice revenue, increased smartphone adoption, and various government initiatives in governance and education. It also discusses challenges such as regulatory uncertainties and operational costs affecting profitability in the telecom sector.