Downloaded 198 times

![42

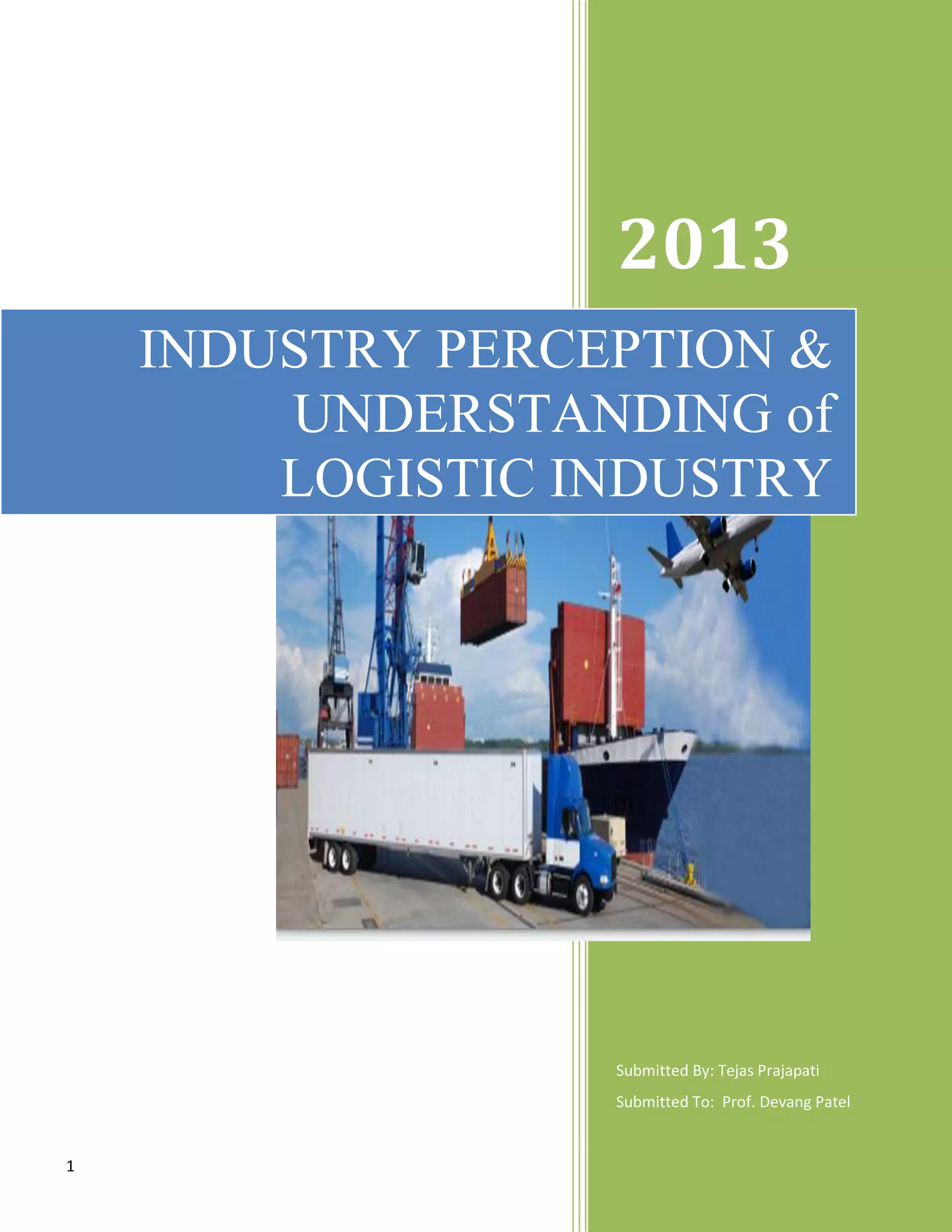

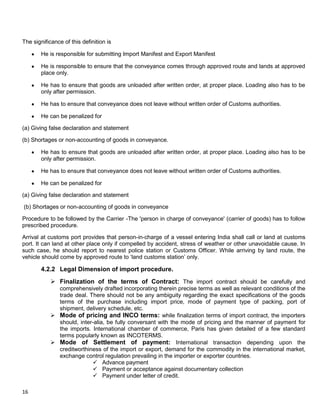

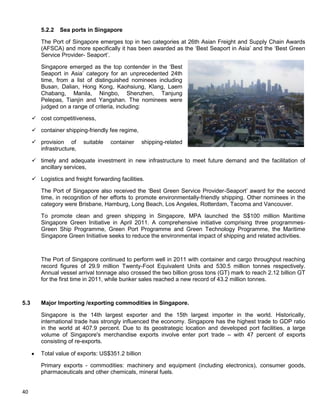

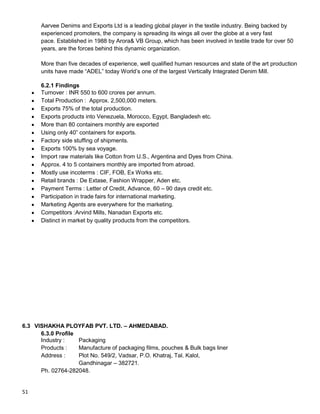

Among Indian imports from Singapore- cocoa and cocoa preparations, mineral fuels, pharmaceutical

products, tanning or dyeing extracts, perfumery, cosmetic or toilet preparations, plastics, paper and

paperboard, manmade filaments, natural or cultured pearls, iron & steel; copper; optical, photographic

cinematographic measuring, checking precision, medical or surgical inst. and apparatus, aircraft and

parts; ships, boats and floating structures; boilers, machinery and mechanical appliances, electrical

machinery etc. form the important items.

Exports to Singapore

Values in US$ Million

Country 2011-2012 %Share 2012-2013

(Apr- Dec)

%Share

SINGAPORE 16,857.71 5.5097 10,504,.39 4.8624

India‟ total

export

305,963.92 216,032.30

Imports from Singapore

Values in US$ Million

Country 2011-2012 %Share 2012-2013

(Apr- Dec)

%Share

SINGAPORE 8,600.29 1.7576 5,727.64 1.5775

India‟ total

import

489,319.49 363,081.40

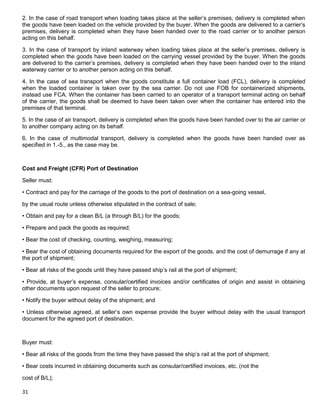

5.6 India– Singapore Trades 2000-01 to 2011-12

5.6.0 Exports

India – Singapore Trade 2000-01 to 2011-12

[Figures in USD Million]

Year Export to

Singapore

India's Total

Export

Growth of

Exports to

Singapore

(% over

preceding year)

Growth of

overall

exports

(% over

preceding

year)

2000-01 877.11 44,560.29 30.39 21.01

2001-02 972.31 43,826.72 10.85 -1.65

2002-03 1421.58 52,719.43 20.29 20.29

2003-04 2124.83 63,842.55 21.10 21.10](https://image.slidesharecdn.com/projectreportsip-130823045042-phpapp02/85/import-export-full-report-42-320.jpg)

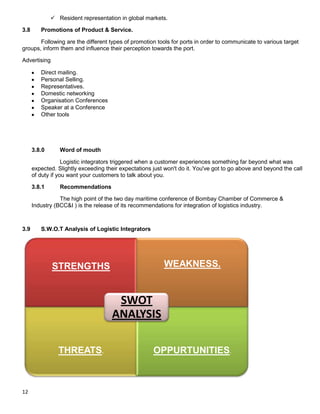

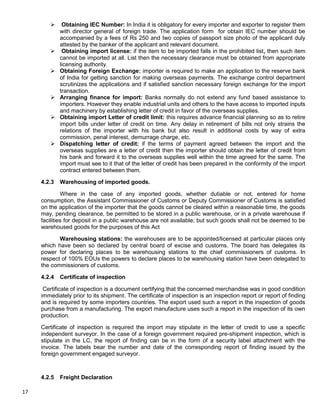

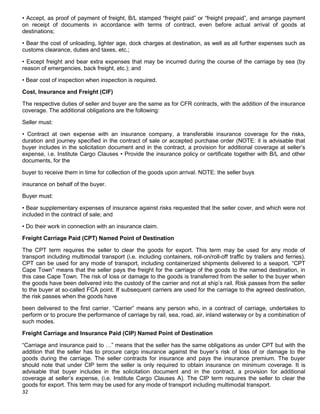

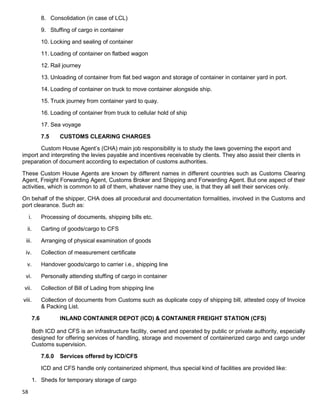

![43

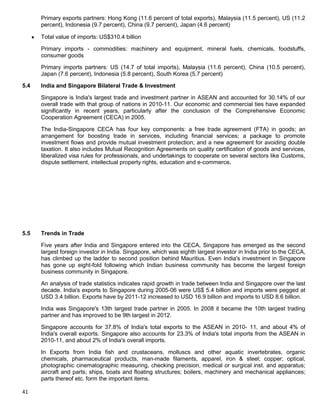

2004-05 4000.61 83,535.94 88.28 30.85

2005-06 5425.29 103,090.53 35.61 23.41

2006-07 6053.84 126,414.05 11.59 22.62

2007-08 7379.2 163,132.18 21.89 29.05

2008-09 8444.93 185,295.36 14.44 13.59

2009-10 7592.17 178,751.43 -10.1 -3.53

2010-11 9825.44 251,136.19 29.42 40.49

2011-12 1657.71 305,963.92 71.57 21.83

5.6.1 Imports

India – Singapore Trade 2000-01 to 2011-12

[Figures in USD Million]

Year Imports

from

Singapore

India's

Total

Imports

Growth of

Imports from

Singapore

(% over

preceding

year)

Growth of

overall

Imports

(% over

preceding

year)

2000-01 1463.91 50,536.45 26.17 1.61

2001-02 1304.09 51,413.28 -10.92 1.74

2002-03 1434.81 61,412.14 10.02 19.45

2003-04 2085.37 78,149.11 45.34 27.25

2004-05 2651.4 111,517.43 27.14 42.70

2005-06 3353.77 149,165.73 26.49 33.76](https://image.slidesharecdn.com/projectreportsip-130823045042-phpapp02/85/import-export-full-report-43-320.jpg)

This document provides an overview of Logistic Integrators, an Indian logistics company. It discusses the company's vision, mission, products, and services. Some key points: - Logistic Integrators aims to integrate the entire logistics and supply chain with precision while providing innovative solutions beyond boundaries. - The company's products and services include air and sea export/import, with an emphasis on using technology like ERP software to improve efficiency. - Located in Ahmedabad, Logistic Integrators has advantages of being in a major logistics hub and industrial area of Gujarat, with proximity to large industries.