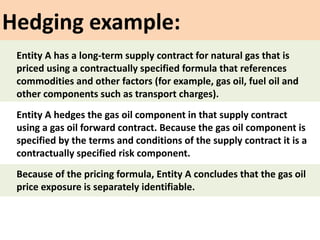

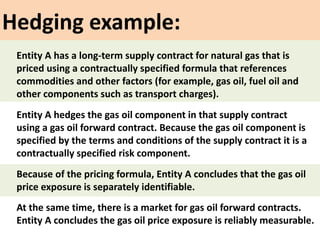

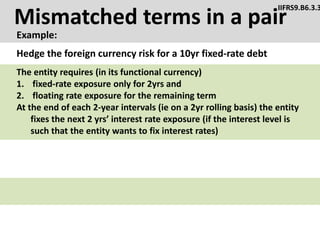

Downloaded 135 times

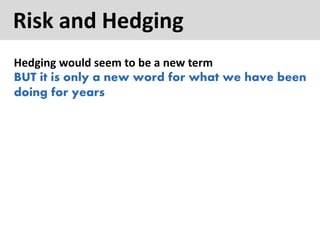

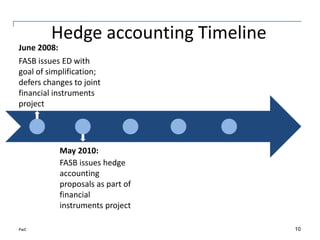

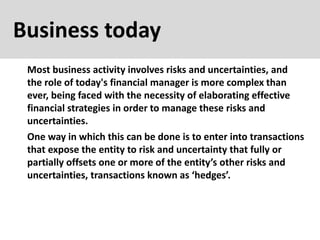

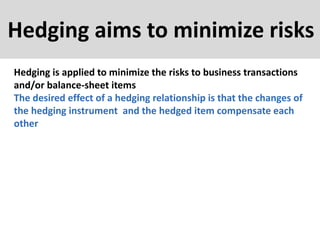

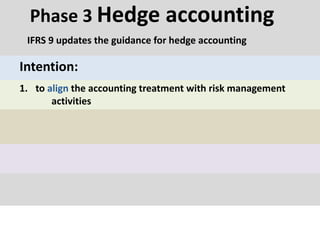

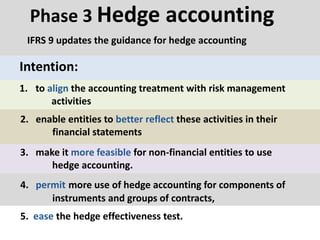

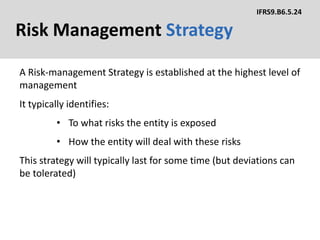

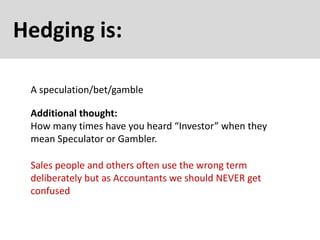

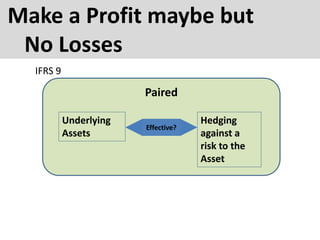

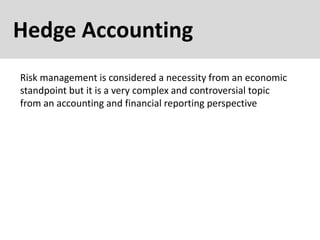

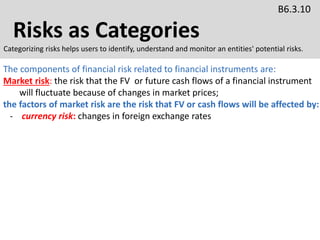

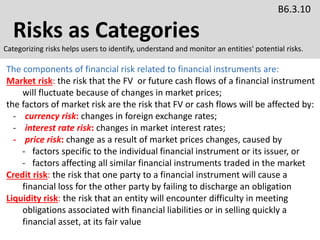

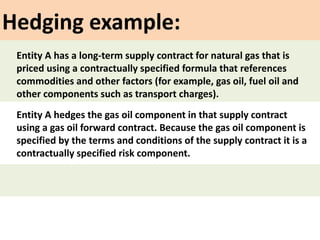

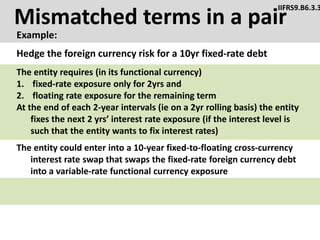

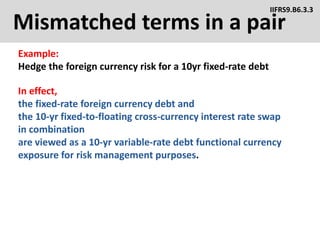

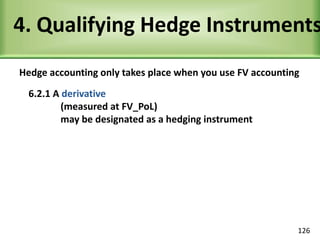

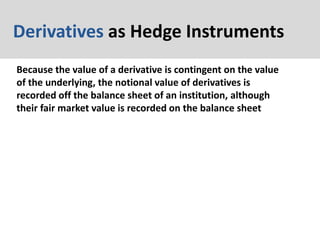

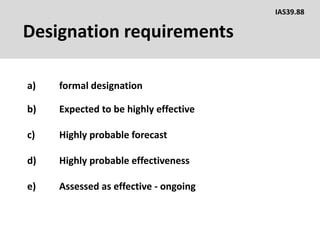

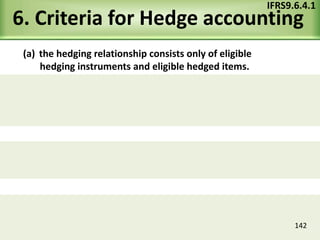

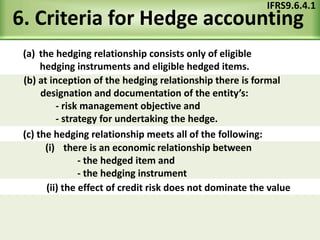

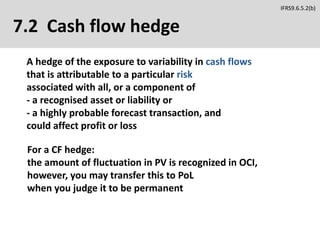

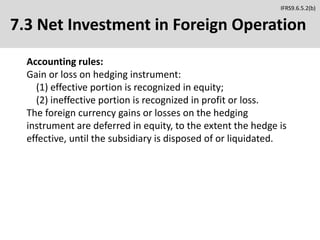

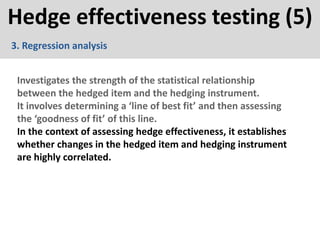

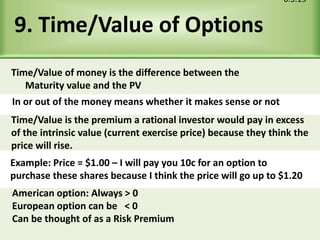

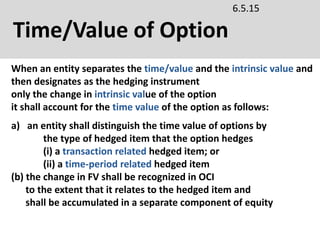

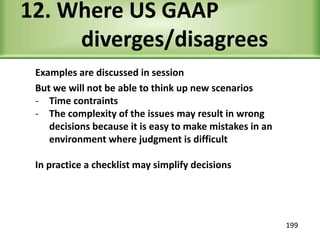

![Time/Value of Option

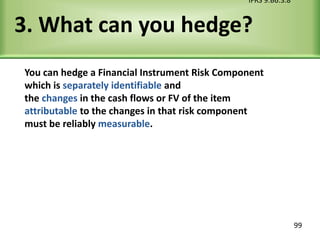

IFRS9.6.5.15

The cumulative change in fair value arising from the time value of

the option that has been accumulated in a separate component of

equity (the ‘amount’) shall be accounted for as follows:

(b) (i) Non-fin >> to add to cost [carrying amount]

(ii) unless not justified (then W/O PoL)

(c)(i) Fin >> amortize (add) to OCI

(ii) If discontinued hedge >> PoL](https://image.slidesharecdn.com/ifrs09hedging02-170812165154/85/Ifrs09-IFRS9-hedging-accounting-for-hedges-hedge-accounting-Investment-derivatives-accounting-195-320.jpg)

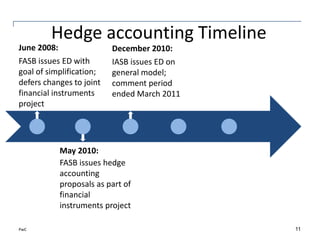

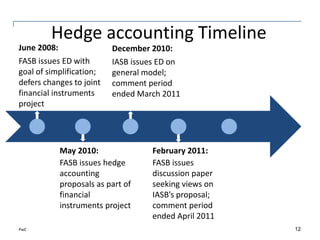

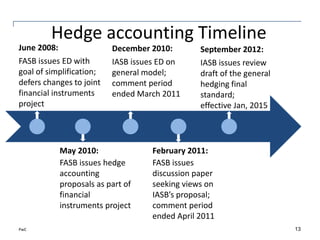

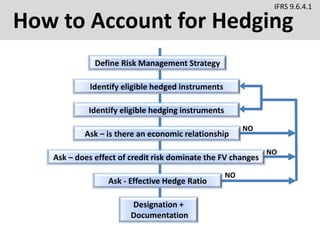

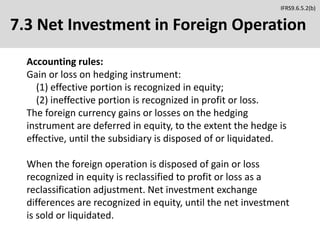

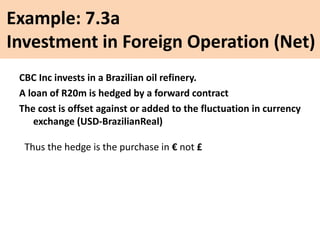

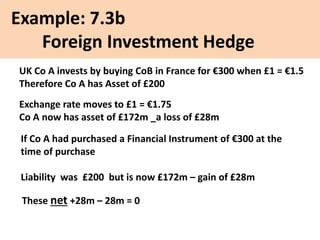

IFRS 9 outlines updated guidance for hedge accounting to align accounting treatment with risk management activities and enable better reflection of these activities in financial statements. It facilitates the use of hedge accounting for components of instruments and simplifies effectiveness tests, making it feasible for non-financial entities. The document emphasizes that hedging is a crucial risk management tool, aimed at minimizing risks related to business transactions and maintaining the net effects between hedged items and hedging instruments.