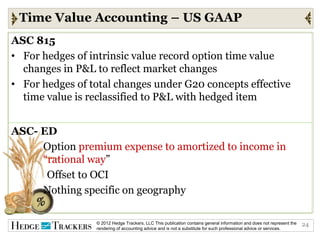

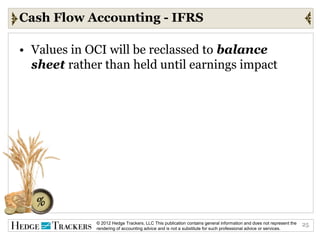

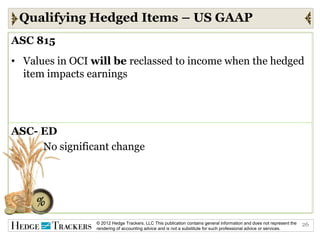

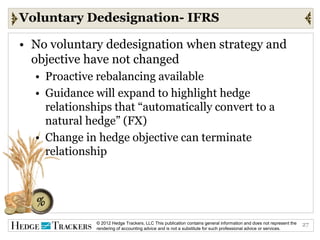

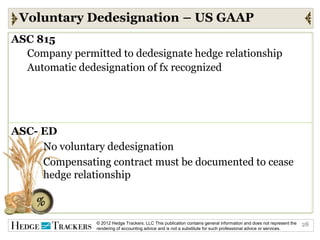

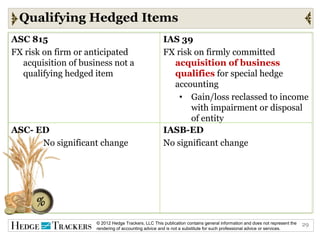

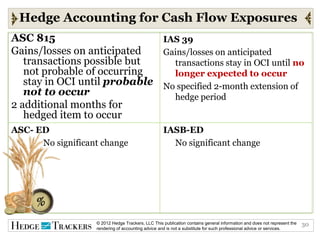

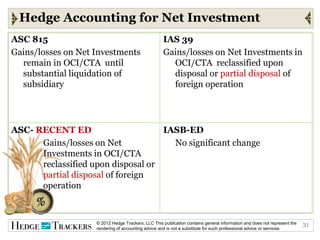

The document discusses the evolution of international financial reporting standards (IFRS) and their potential adoption in the U.S. to replace GAAP by 2014, emphasizing major changes in derivative and hedge accounting processes. It outlines the IASB and FASB projects aimed at revising these accounting principles, including the comparison of IFRS 9 and U.S. GAAP standards. Key aspects addressed include qualifying hedged items, effectiveness testing, and cash flow accounting adjustments related to hedge accounting.