Downloaded 168 times

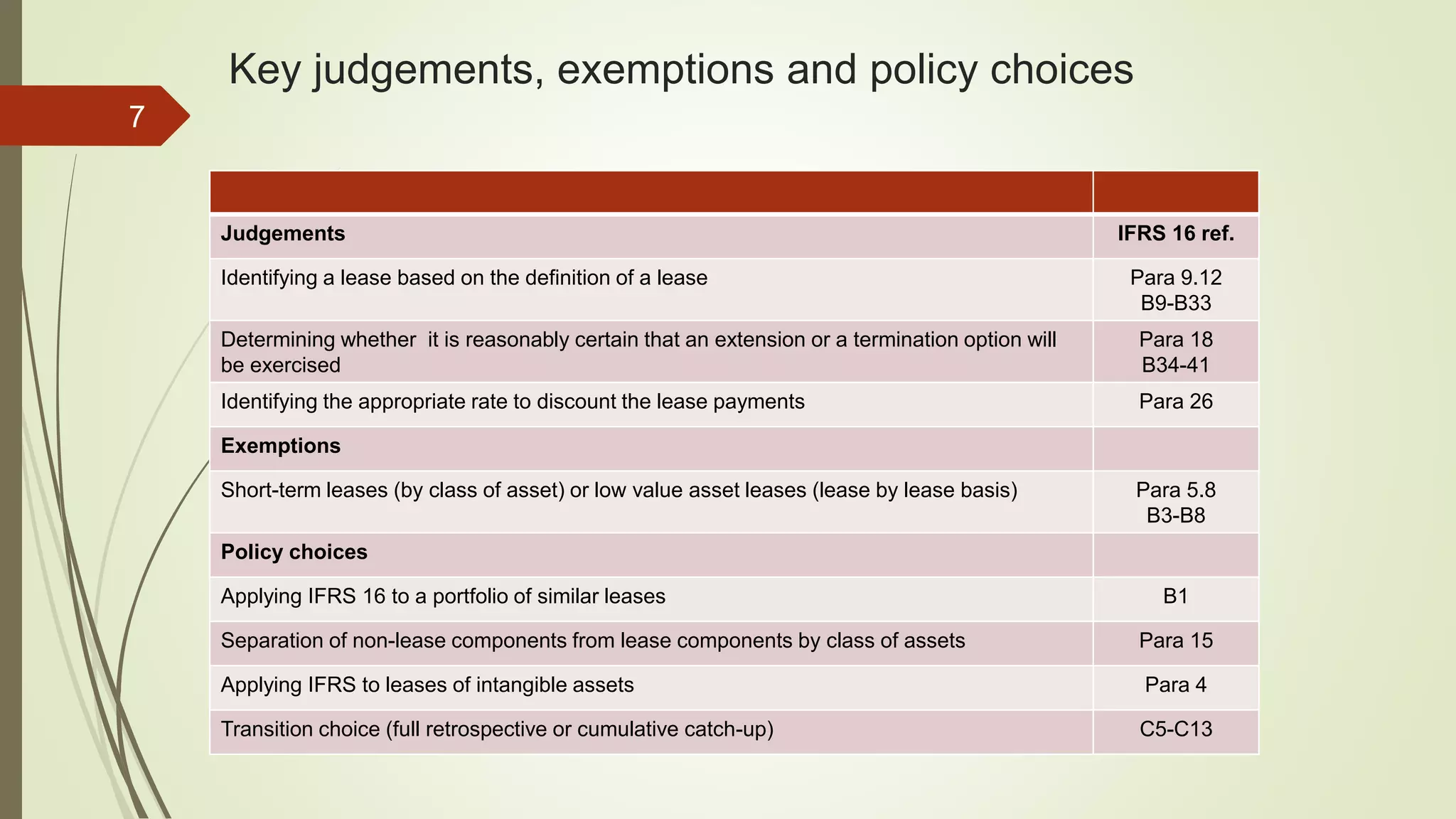

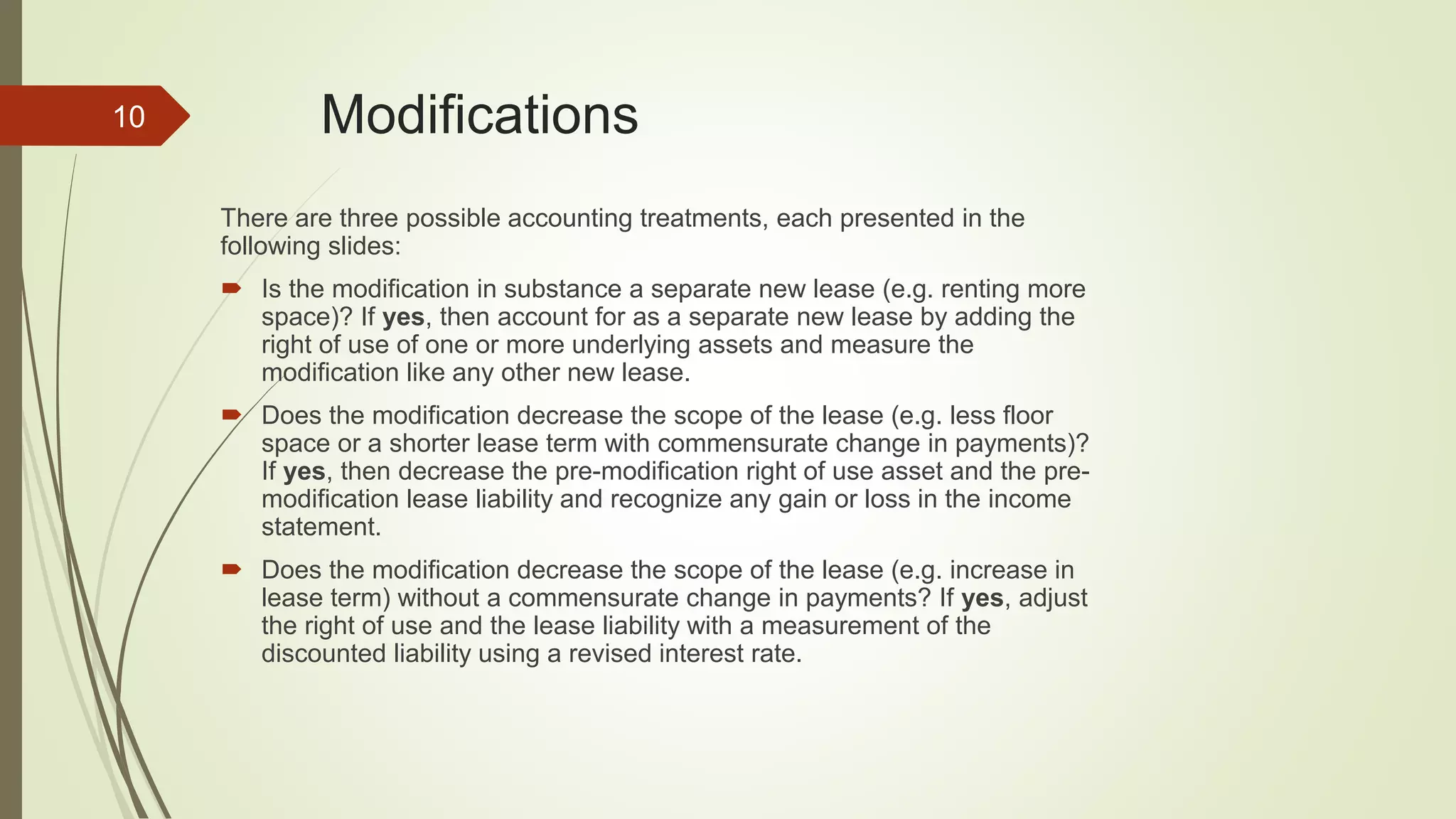

IFRS 16 is a new accounting standard that replaces several previous standards, effective from January 1, 2019, and introduces significant changes for lessees in recognizing lease obligations and right-of-use assets on the balance sheet. The standard offers exemptions for short-term leases and low-value assets, while also impacting financial ratios and requiring a reassessment of existing leases under certain circumstances. Key aspects of the standard include distinguishing between lease and non-lease components, and accounting for modifications to lease agreements.