Download as PDF, PPTX

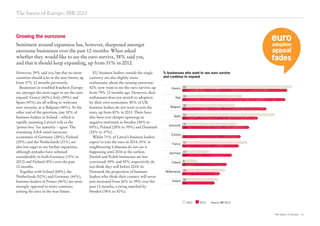

This document discusses the future of Europe based on data from economic forecasts and interviews with business leaders. It finds: 1) Europe's economies are stagnating with weak growth prospects and high unemployment expected to continue. Public debt is also rising in many countries due to slow growth hampering deficit reduction efforts. 2) Business confidence in Europe is low, with few expecting profits or hiring to increase in the coming year. However, investment in machinery is expected to rise which may provide a boost. 3) There is strong support among eurozone business leaders for further European integration, with 66% open to more economic integration and 40% open to greater political union as well. Ireland is least supportive of further integration.