Download to read offline

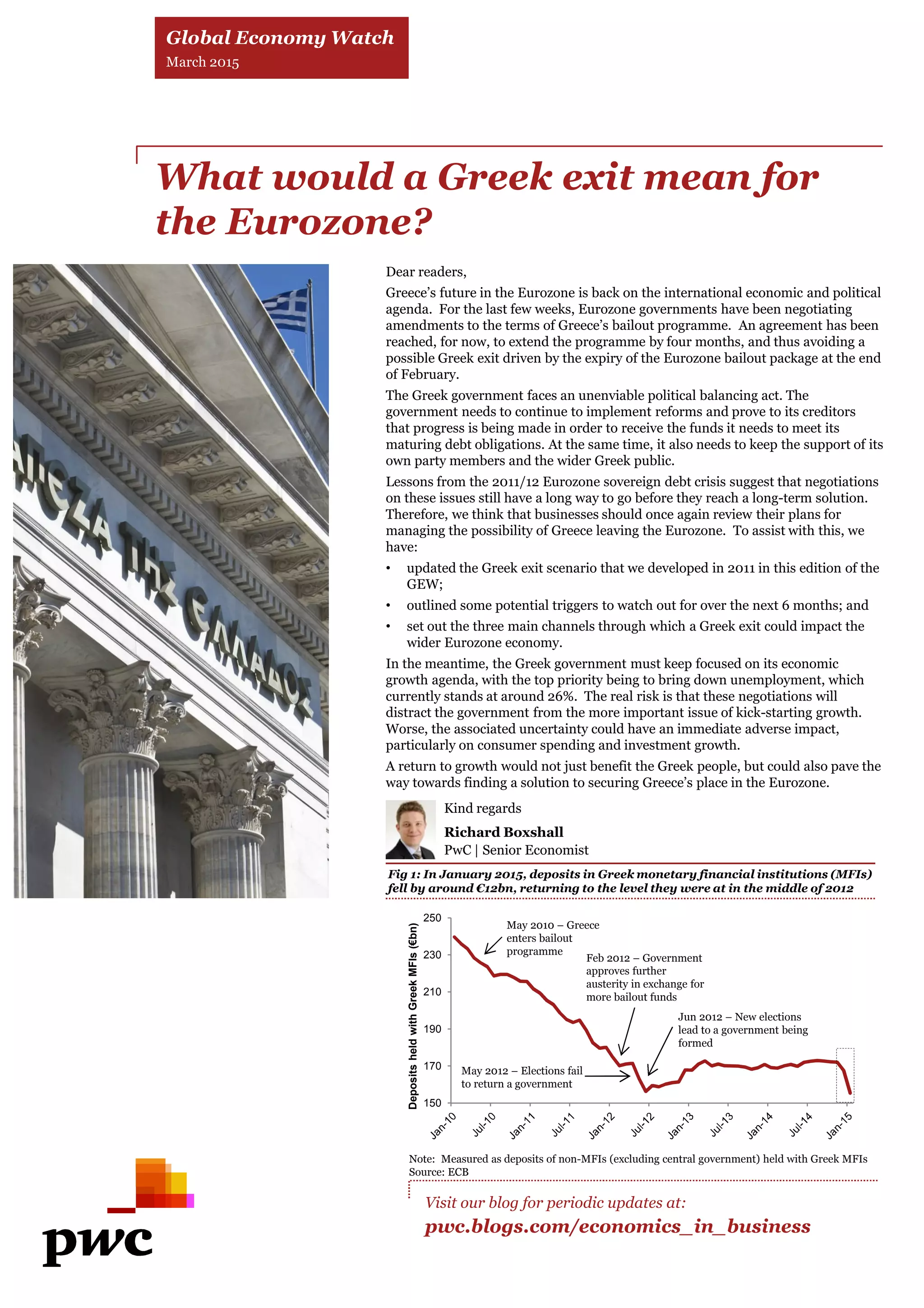

This document discusses the potential economic impacts if Greece were to exit the Eurozone. It outlines two potential triggers that could lead to a Greek exit, including a credit crunch in Greek banks and risks in implementing economic reforms. It then describes three main channels through which a Greek exit could affect the wider Eurozone economy: exposure of European banks, holders of Greek government debt, and potential unexpected contagion. The document projects that a Greek exit could plunge the Greek economy into recession due to high inflation and currency depreciation, but the impacts on the overall Eurozone economy would be more muted and short-lived.