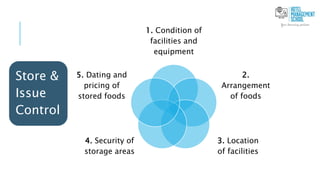

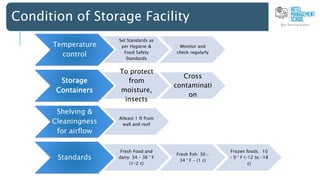

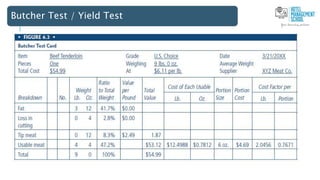

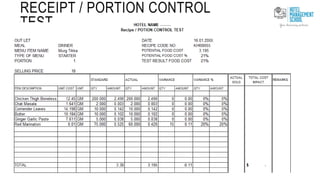

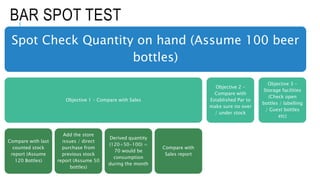

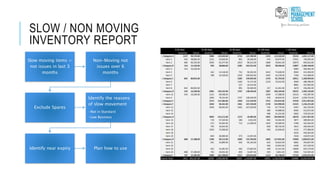

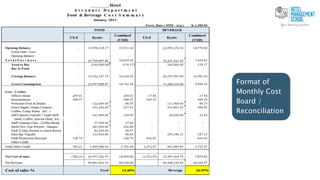

The document outlines essential cost control operations for hotel management, focusing on various aspects like purchasing, receiving, storing, issuing, producing, and selling food and beverages. Key concepts include standard costs, portion control, inventory management, and auditing practices to maintain quality and consistency, with detailed guidelines for each operational phase. Additionally, it emphasizes the importance of market trends, leadership, and corrective measures to ensure financial accountability and operational efficiency.