Downloaded 275 times

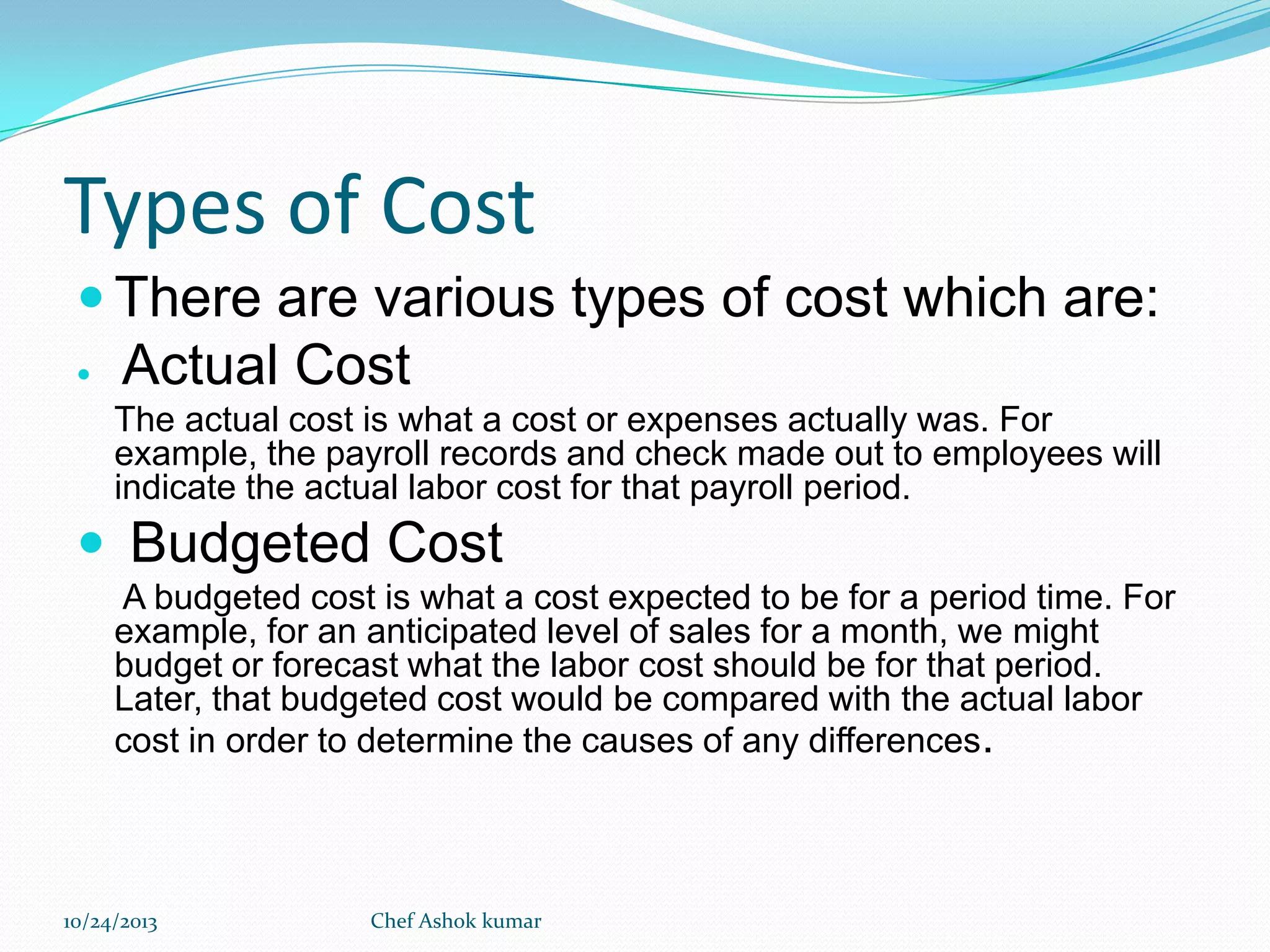

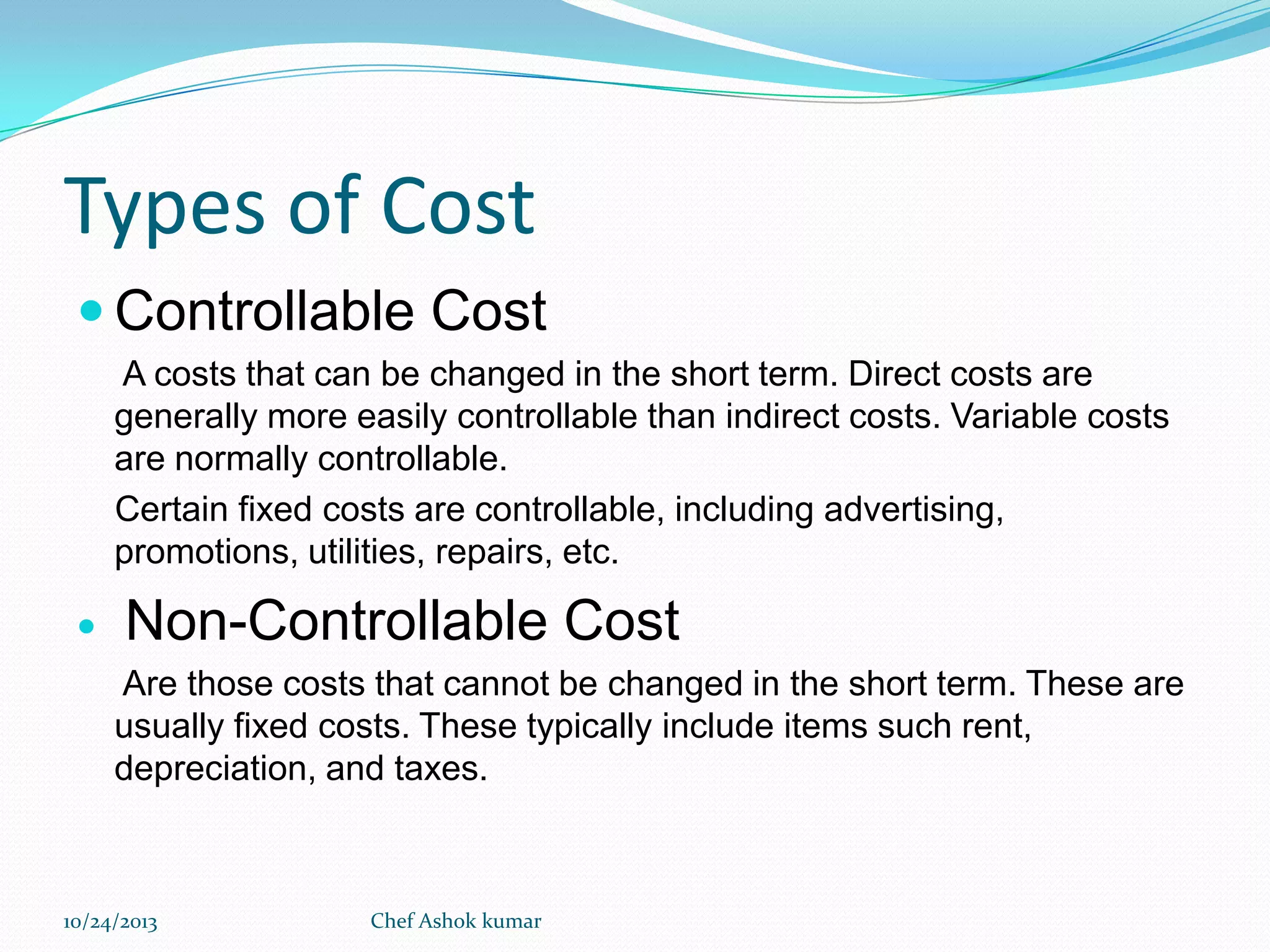

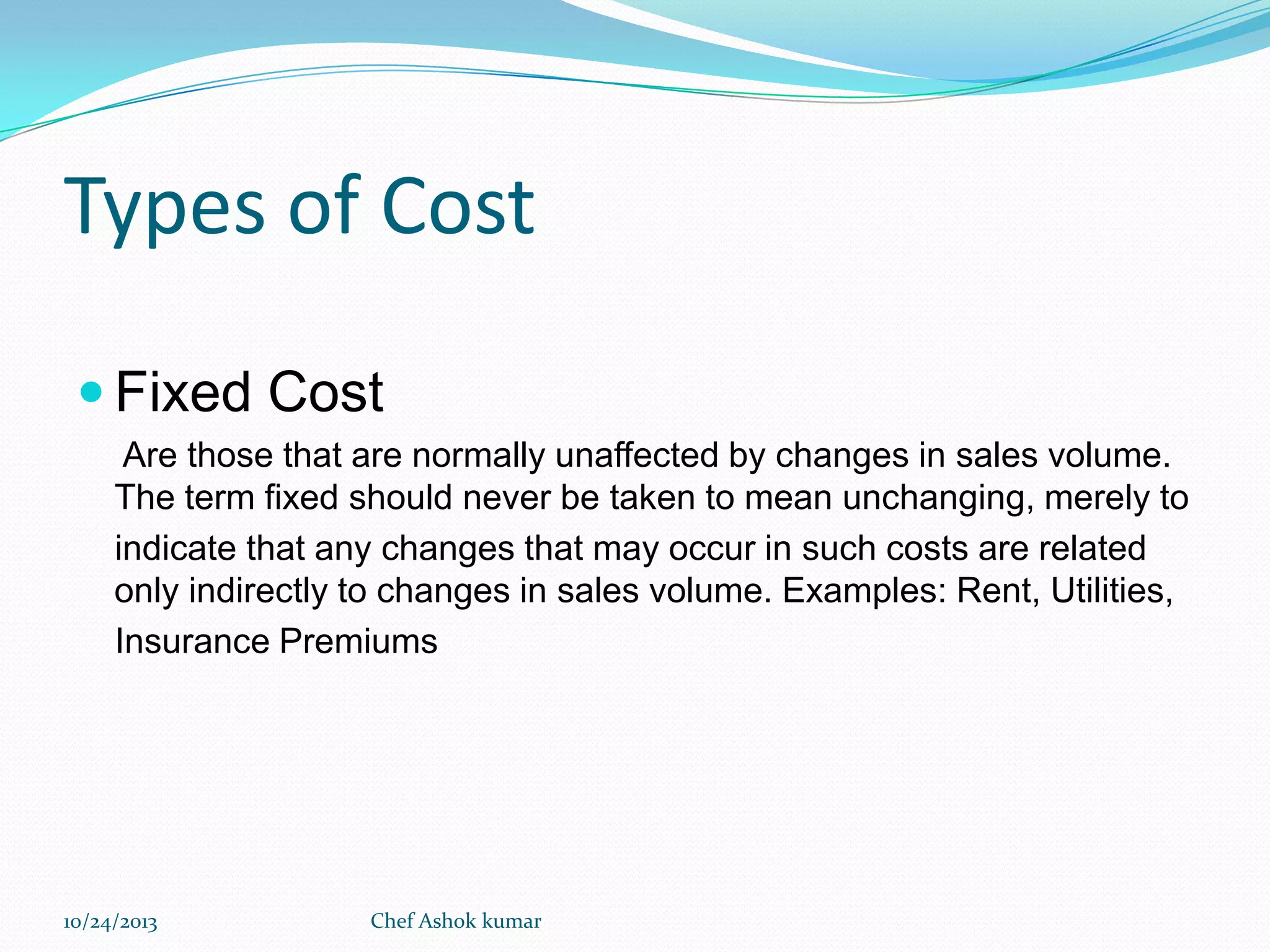

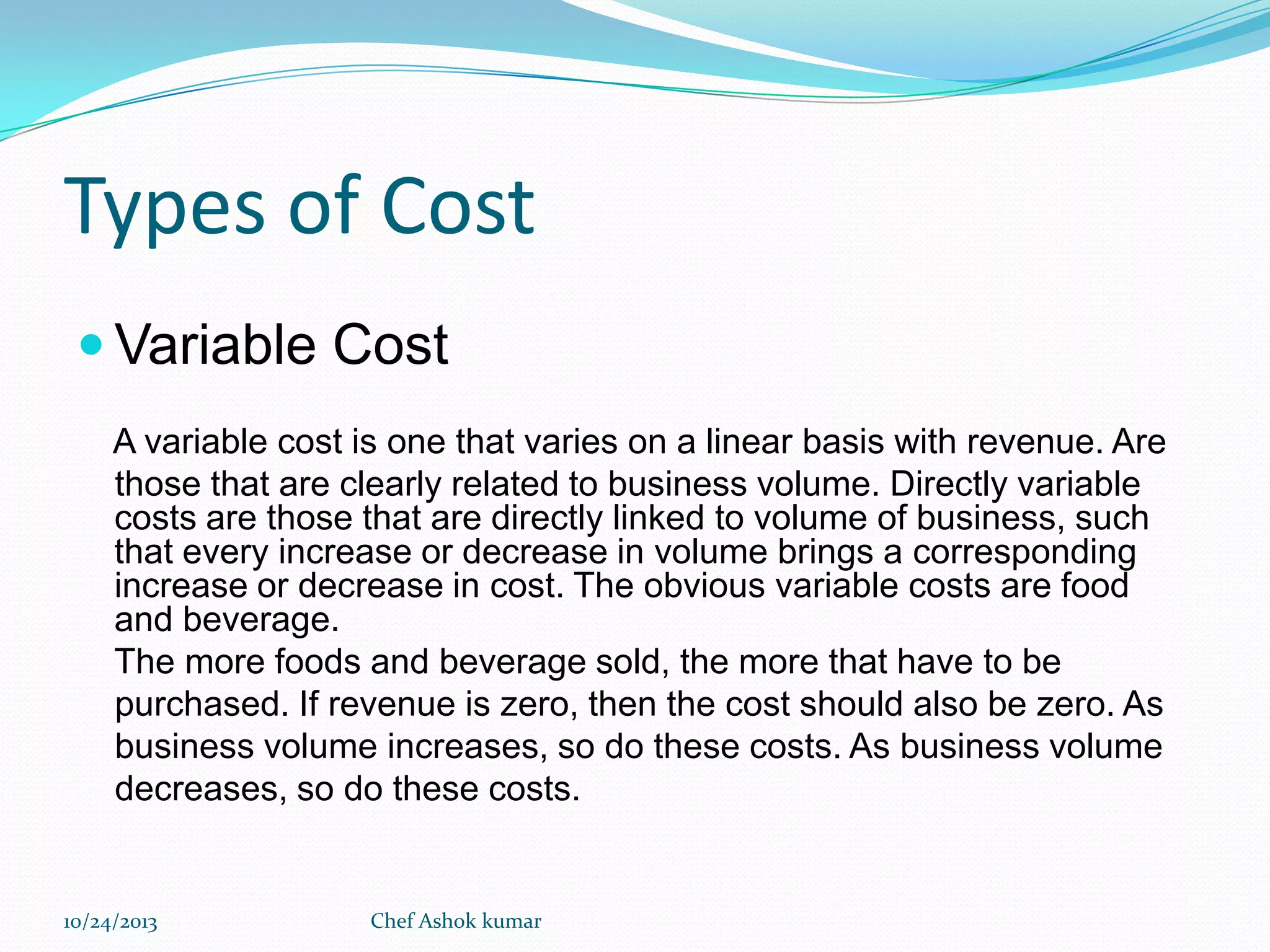

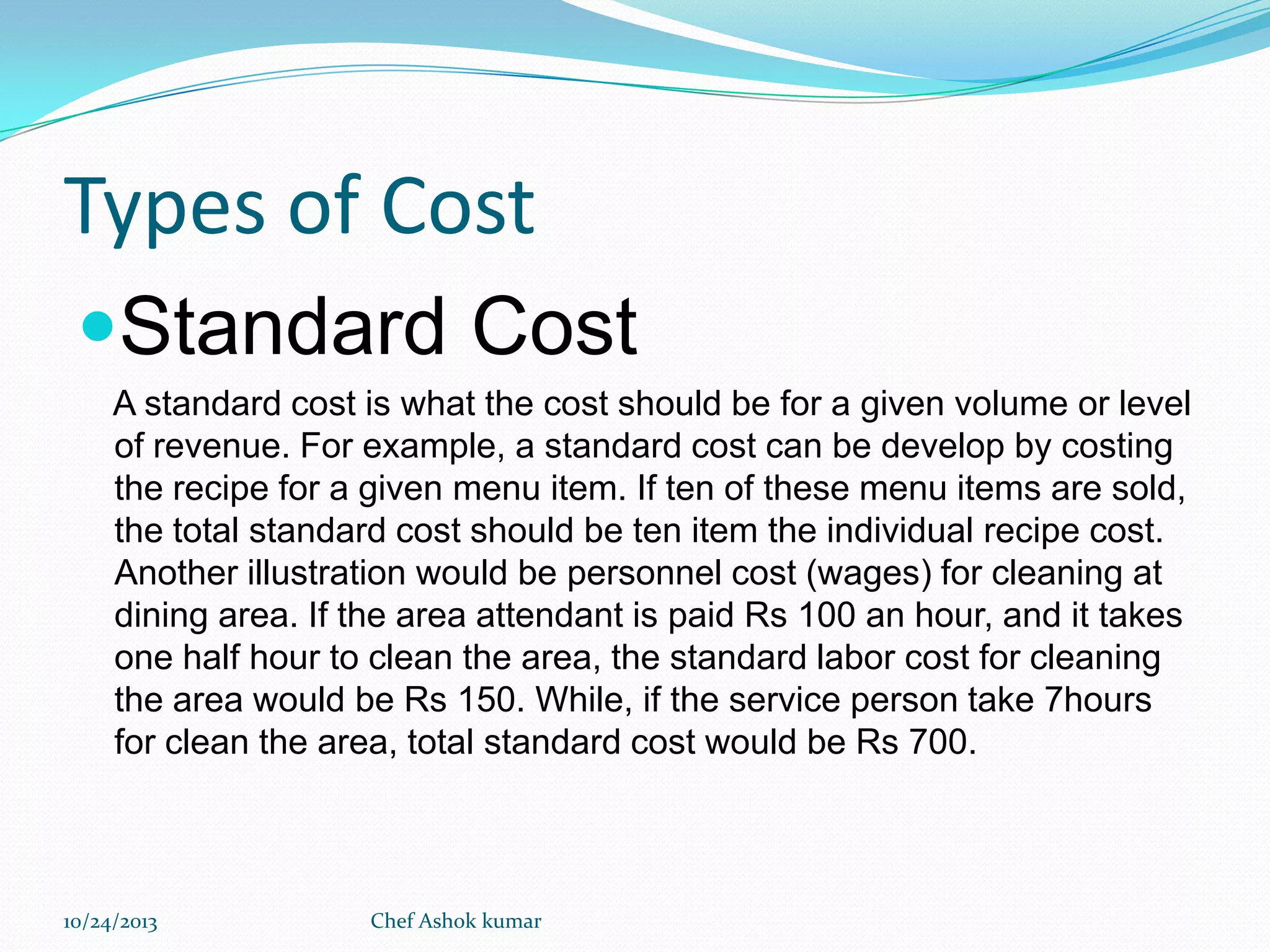

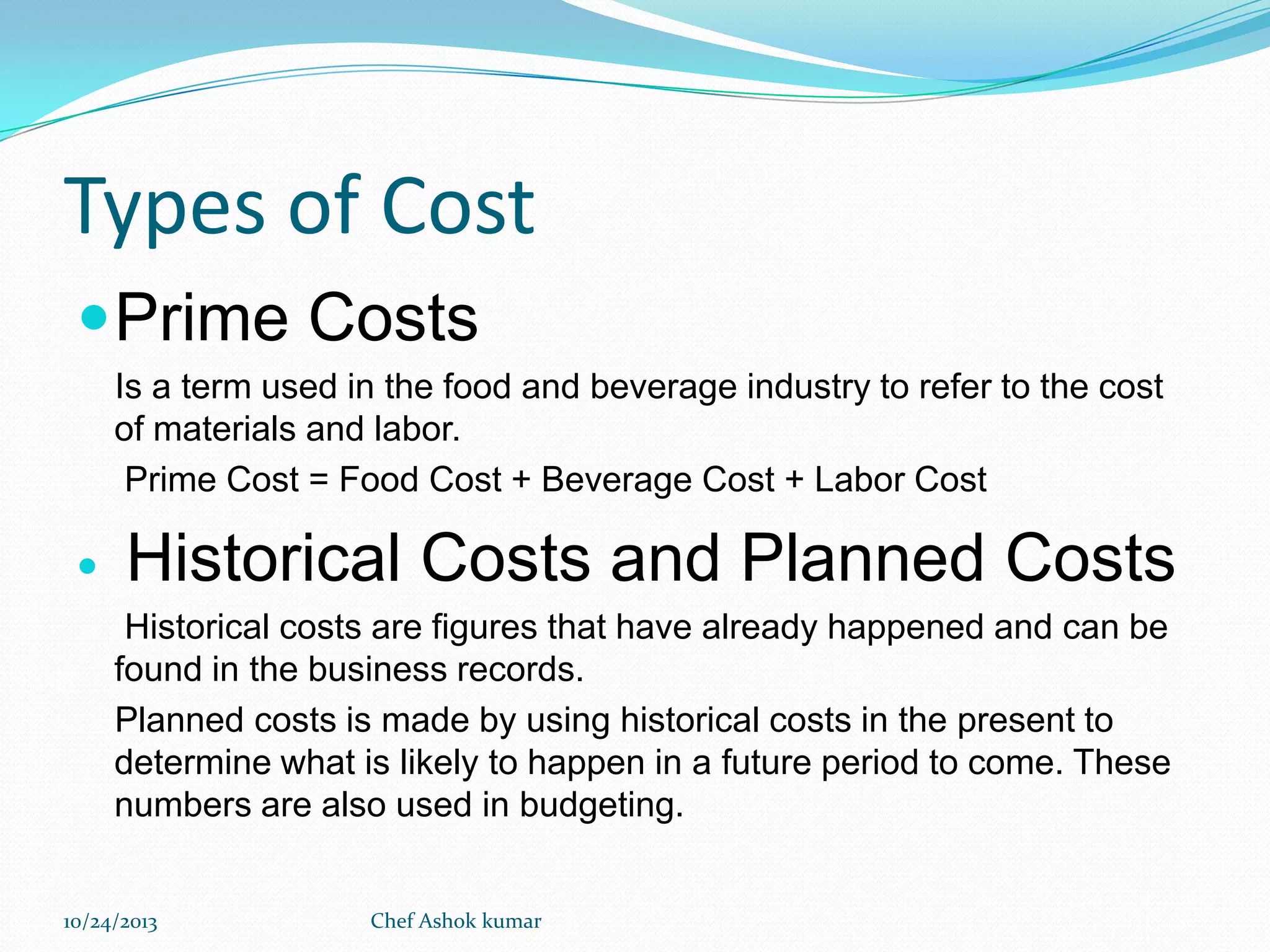

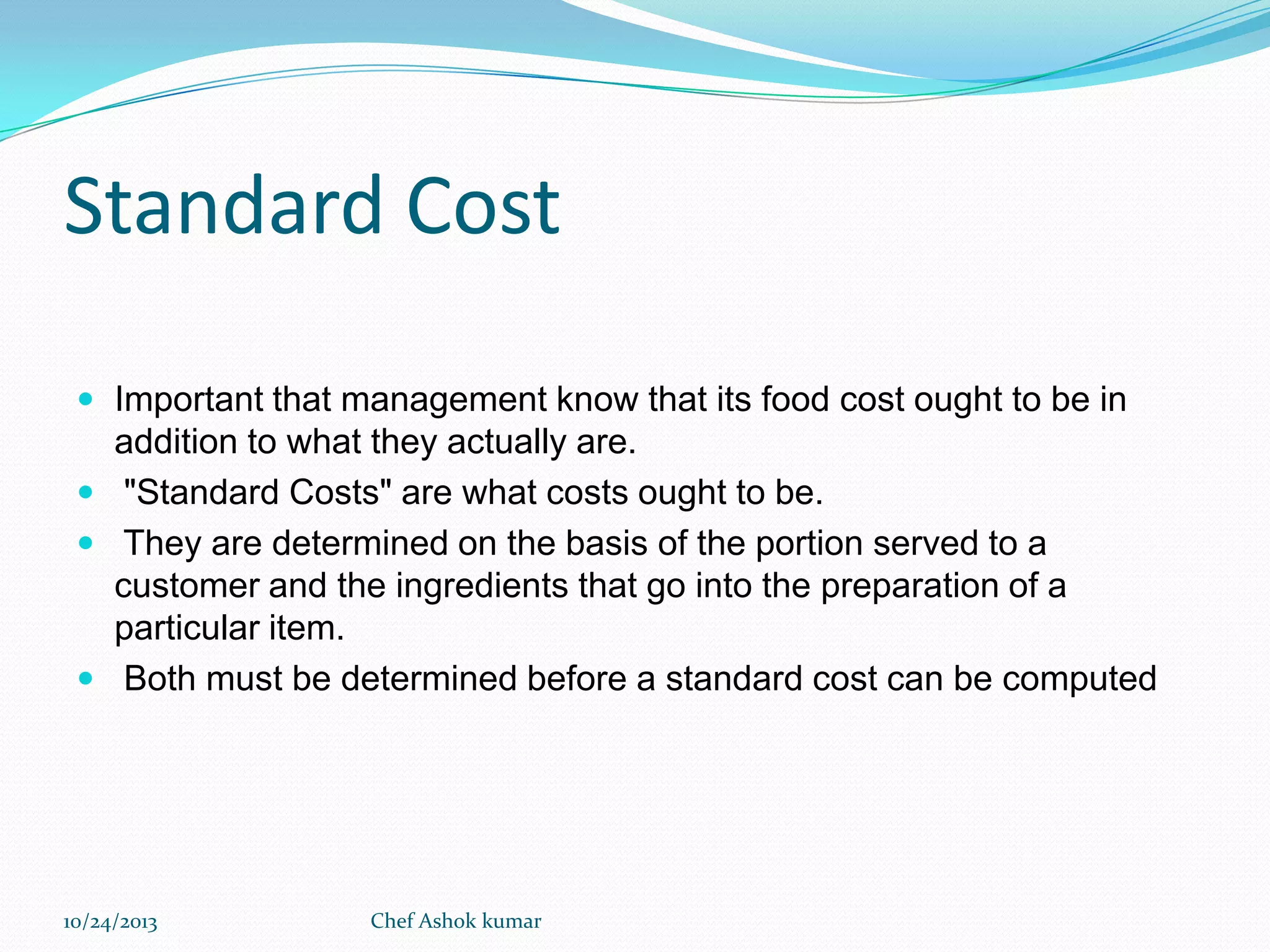

This document discusses food and beverage cost control. It defines cost control as the process by which managers attempt to regulate costs and prevent excessive costs. It explains that the total responsibility for cost control rests with management, though specific responsibilities may be delegated. It identifies the key factors needed for cost control as controlling inefficiency, waste, and keeping costs aligned with acceptable bounds. It then describes different types of costs including fixed, variable, direct, indirect, joint, sunk, opportunity, standard, and prime costs.