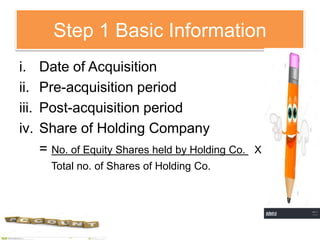

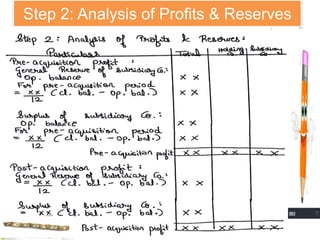

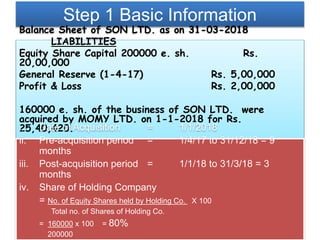

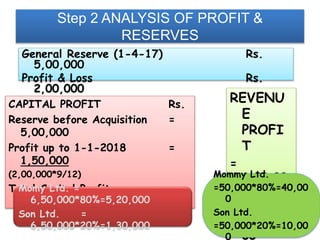

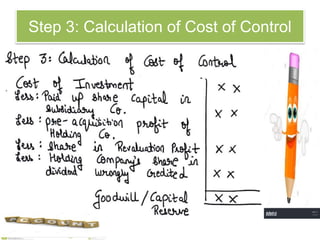

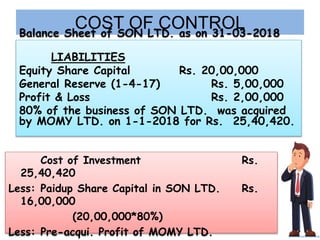

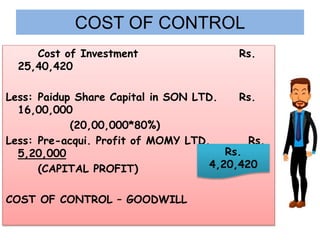

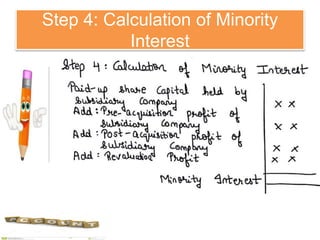

The document discusses the process of preparing a consolidated balance sheet for a holding company and its subsidiaries. It provides a 4 step process: 1) collecting basic information on acquisition date, ownership percentage, pre/post-acquisition periods, 2) analyzing profits and reserves for pre-acquisition periods, 3) calculating the cost of control and goodwill, and 4) calculating minority interest. It also discusses the treatment of various items like unrealized profits, intercompany transactions, contingent liabilities, unclaimed dividends and others in the consolidated balance sheet.