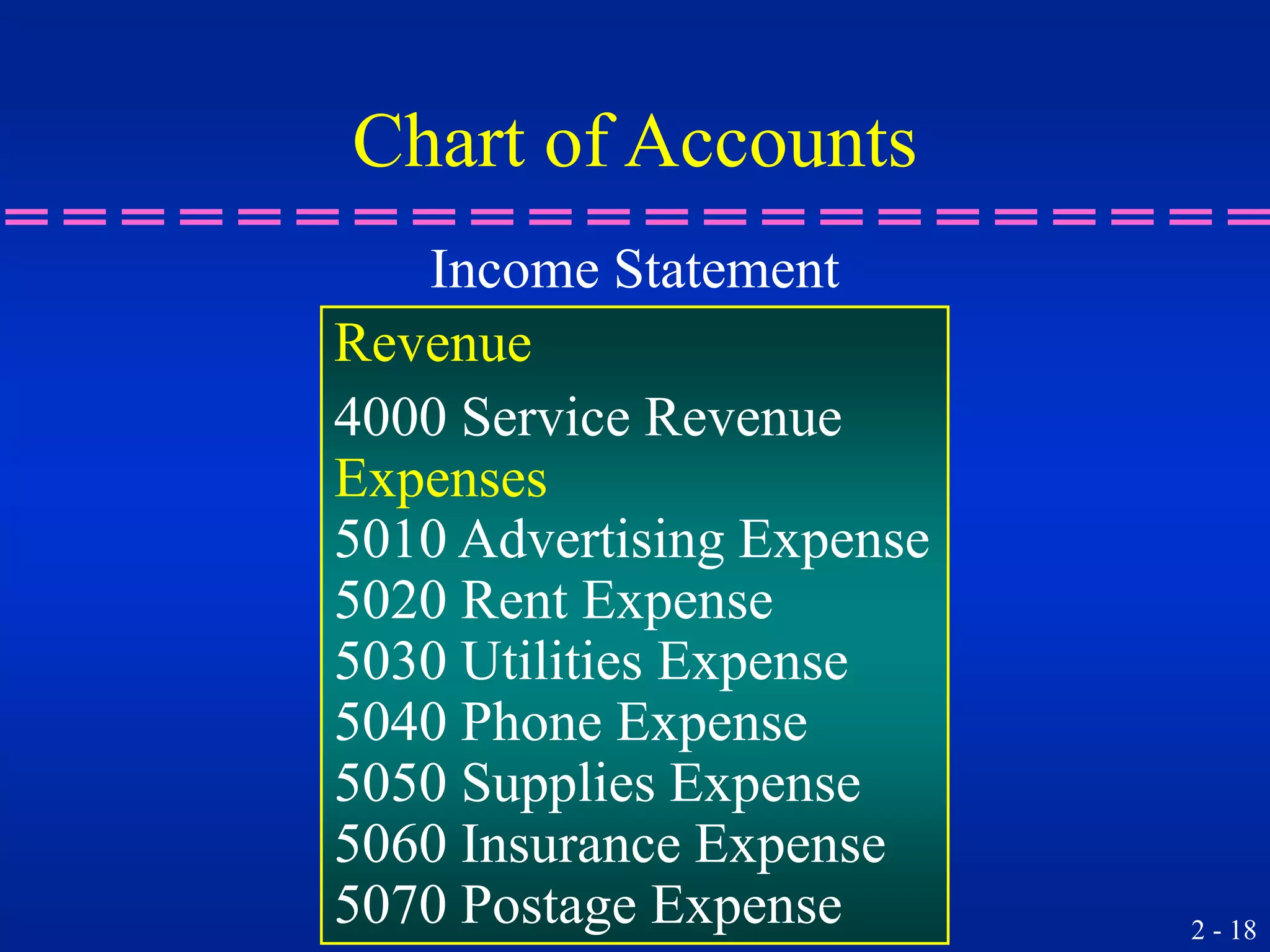

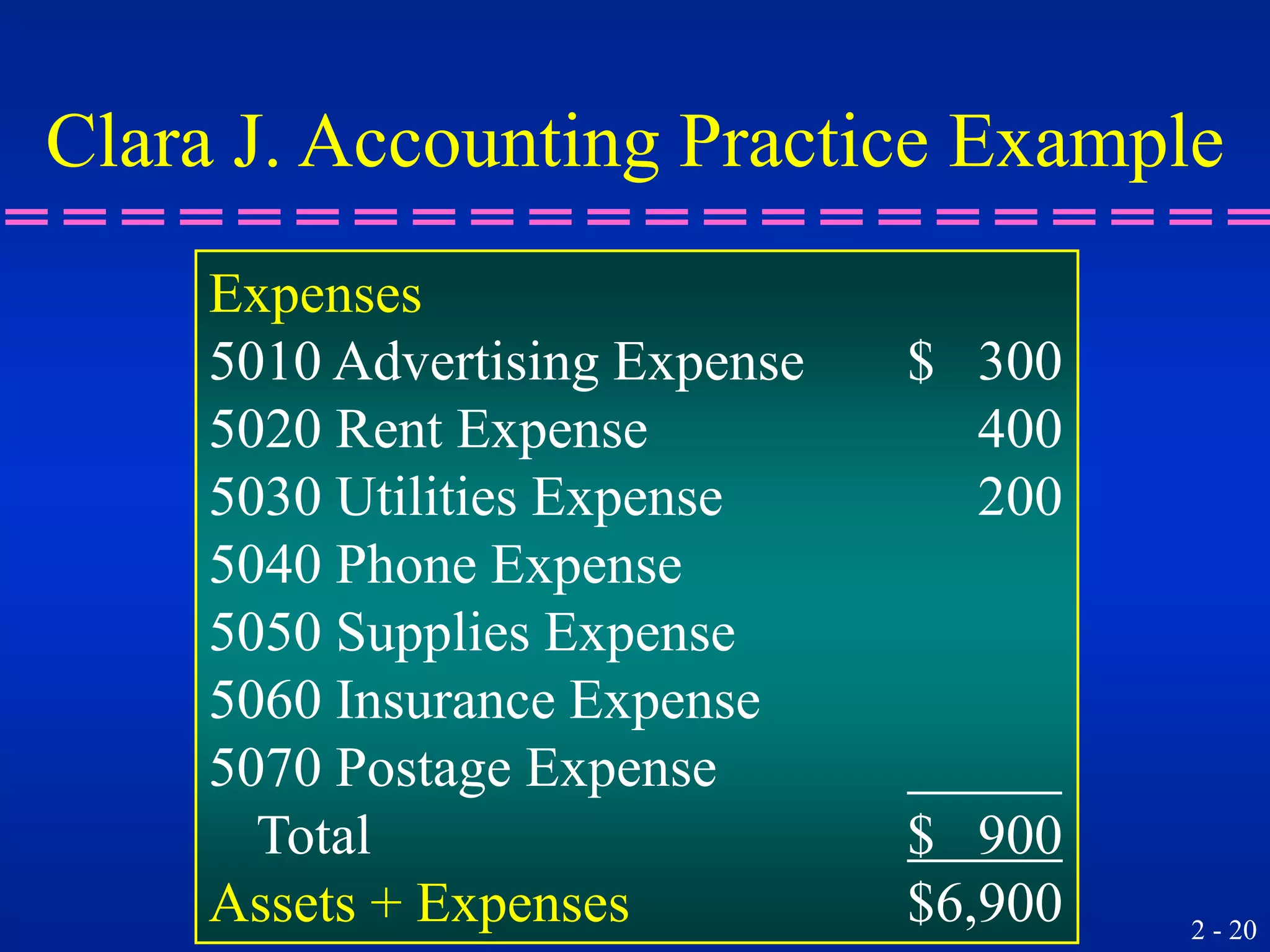

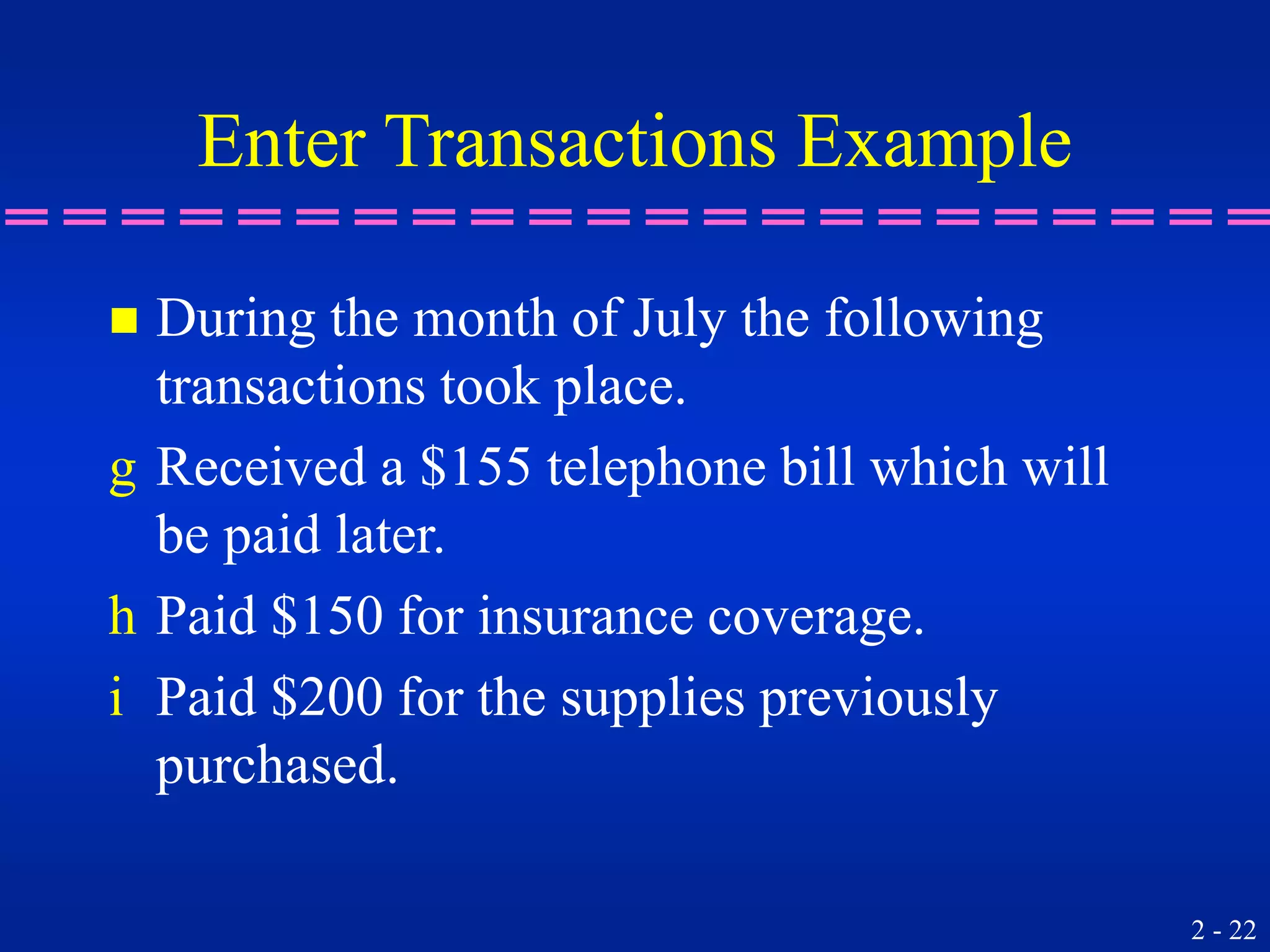

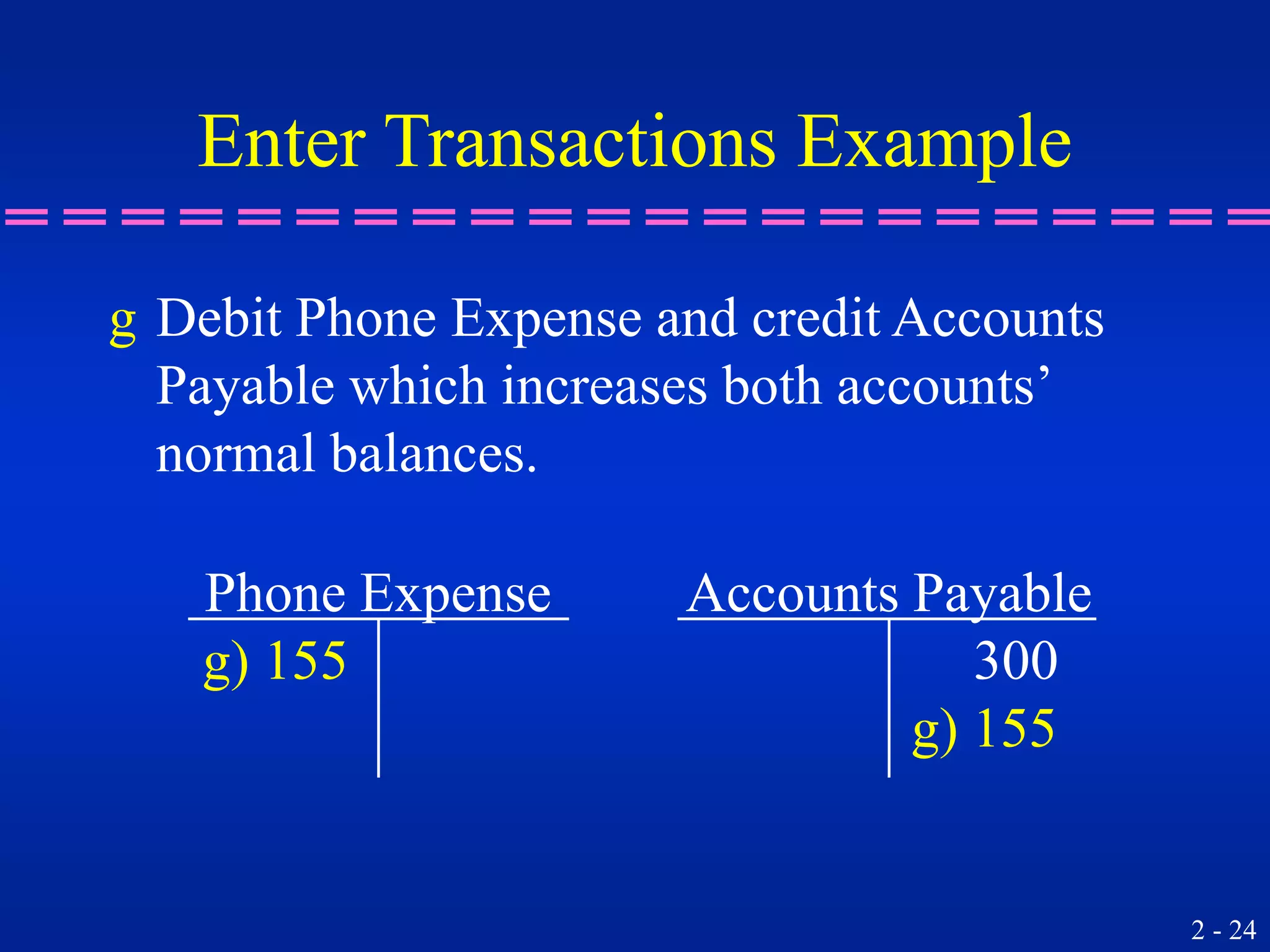

The document discusses accounting concepts related to debits and credits, including:

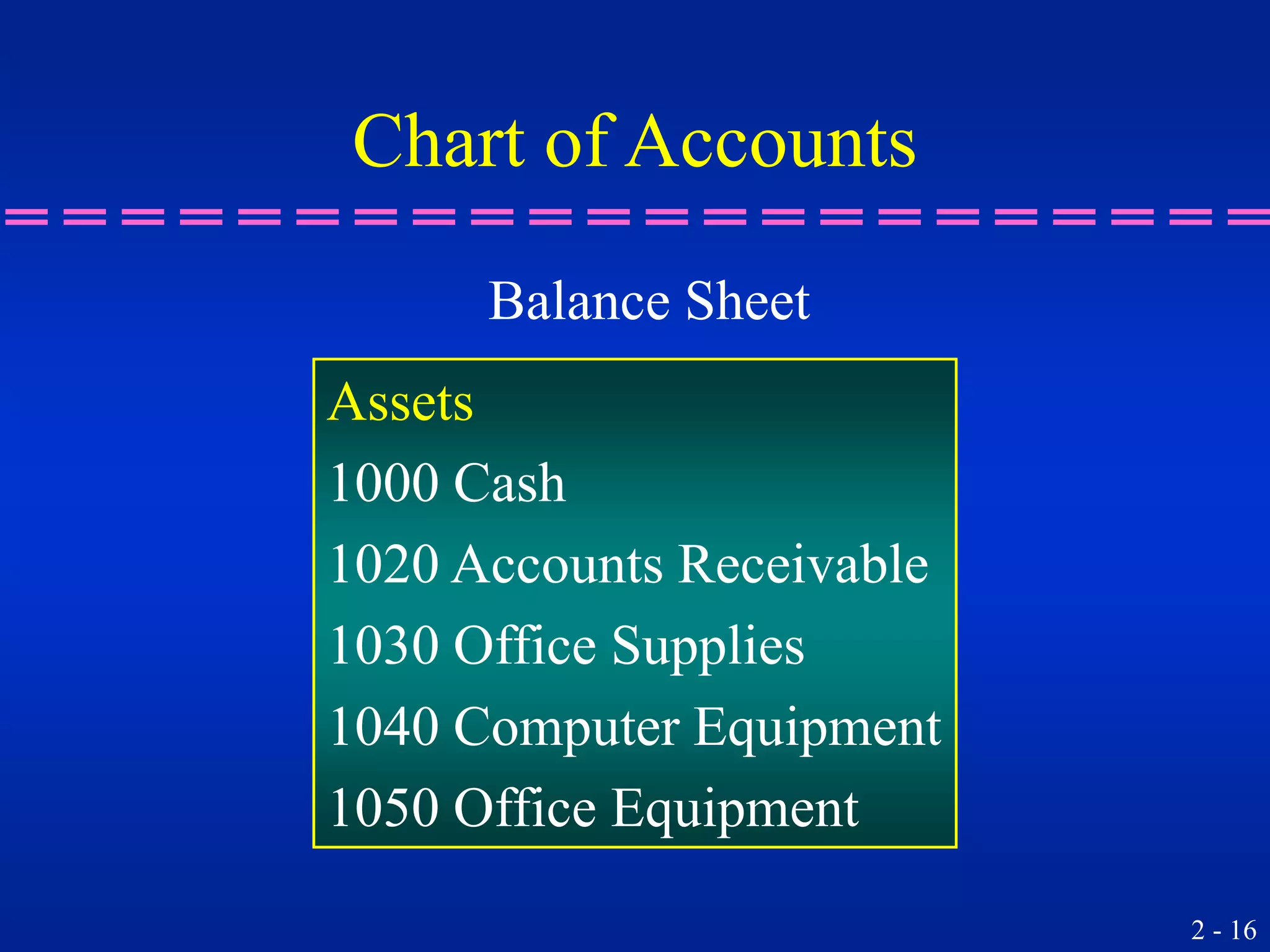

1. Setting up a chart of accounts to organize asset, liability, equity, revenue and expense accounts.

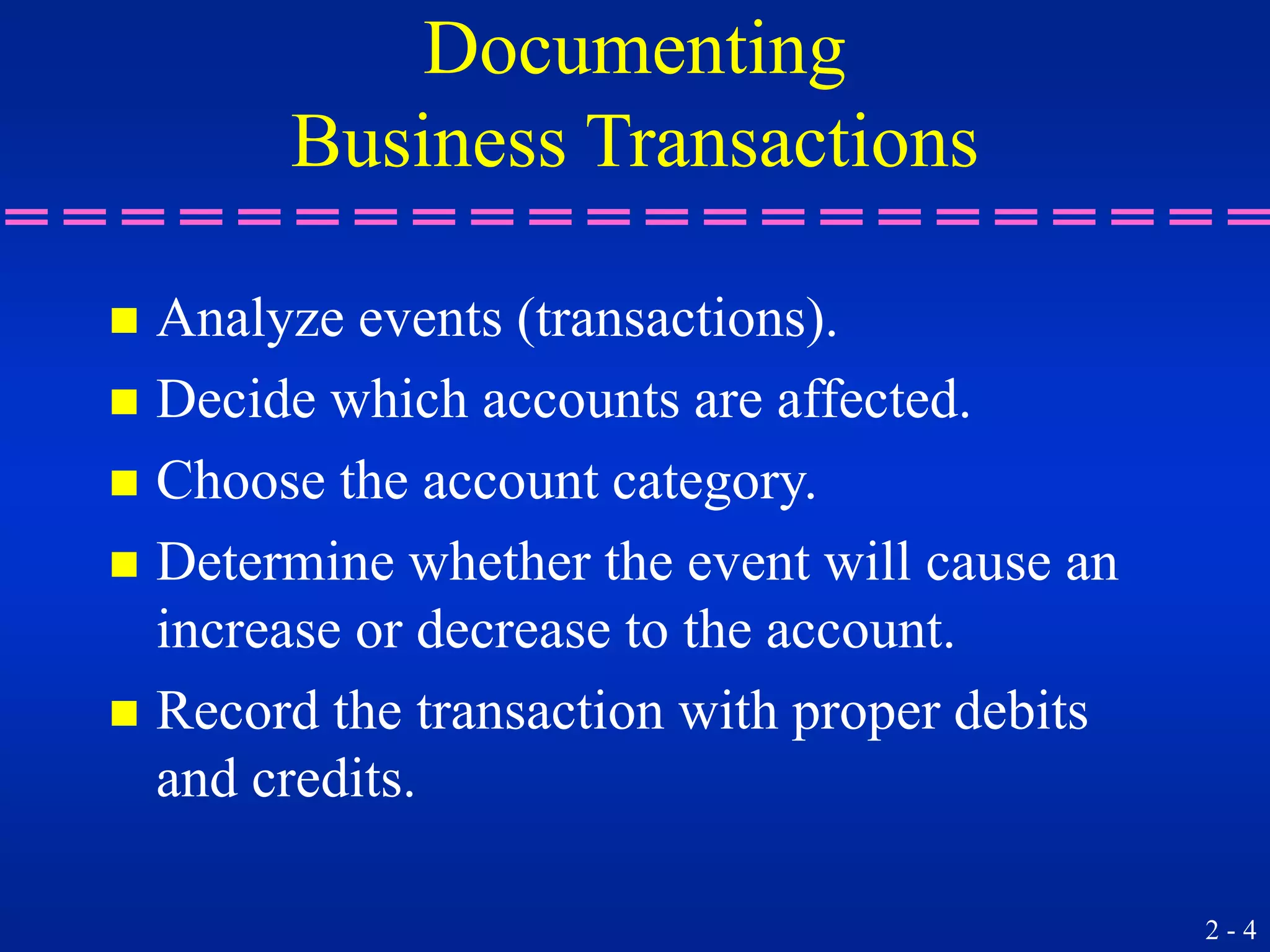

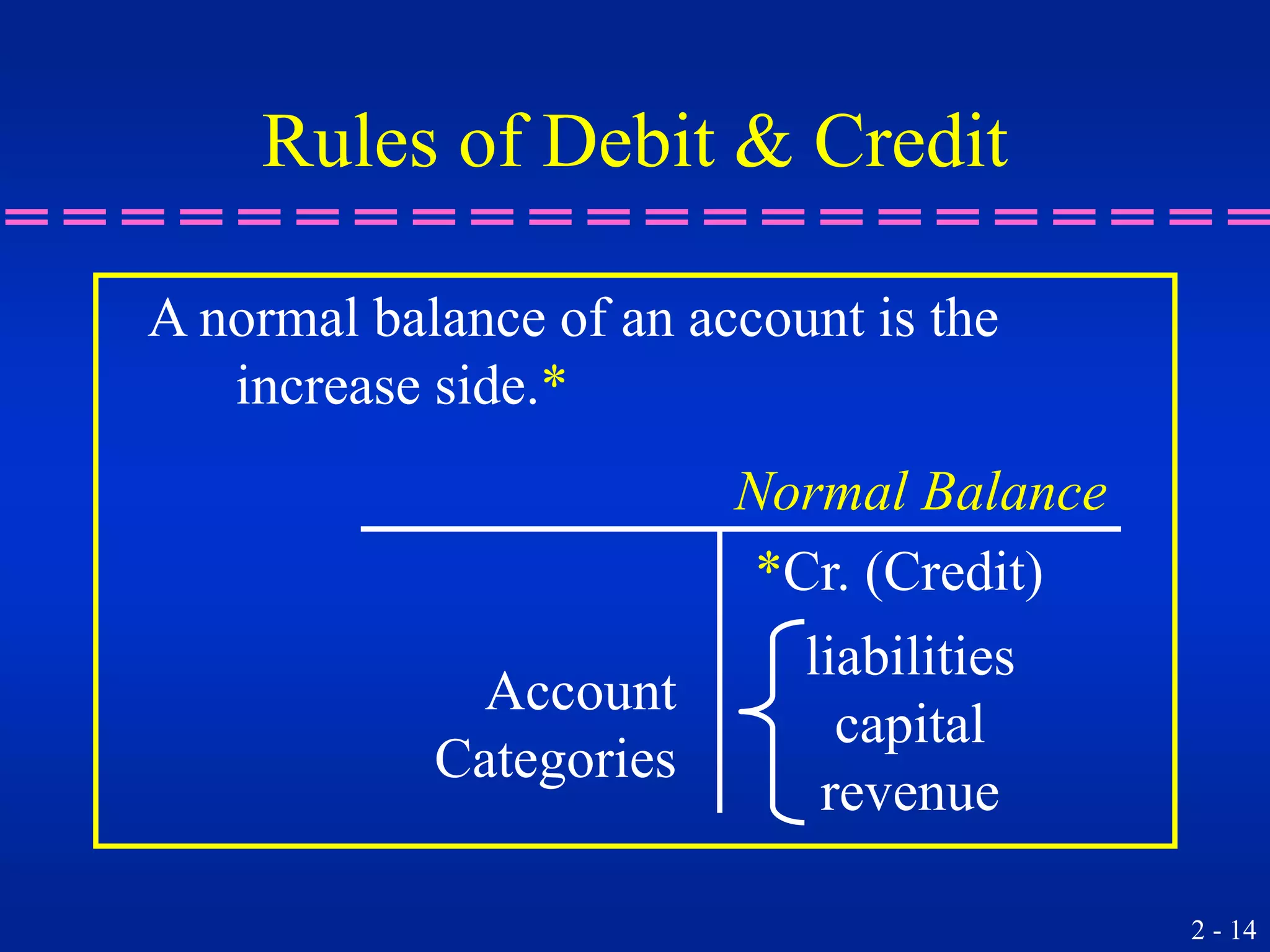

2. Analyzing business transactions and determining the proper debit and credit treatment based on whether the account balance will increase or decrease.

3. Preparing T-accounts and journal entries to record transactions, and ensuring debits equal credits.

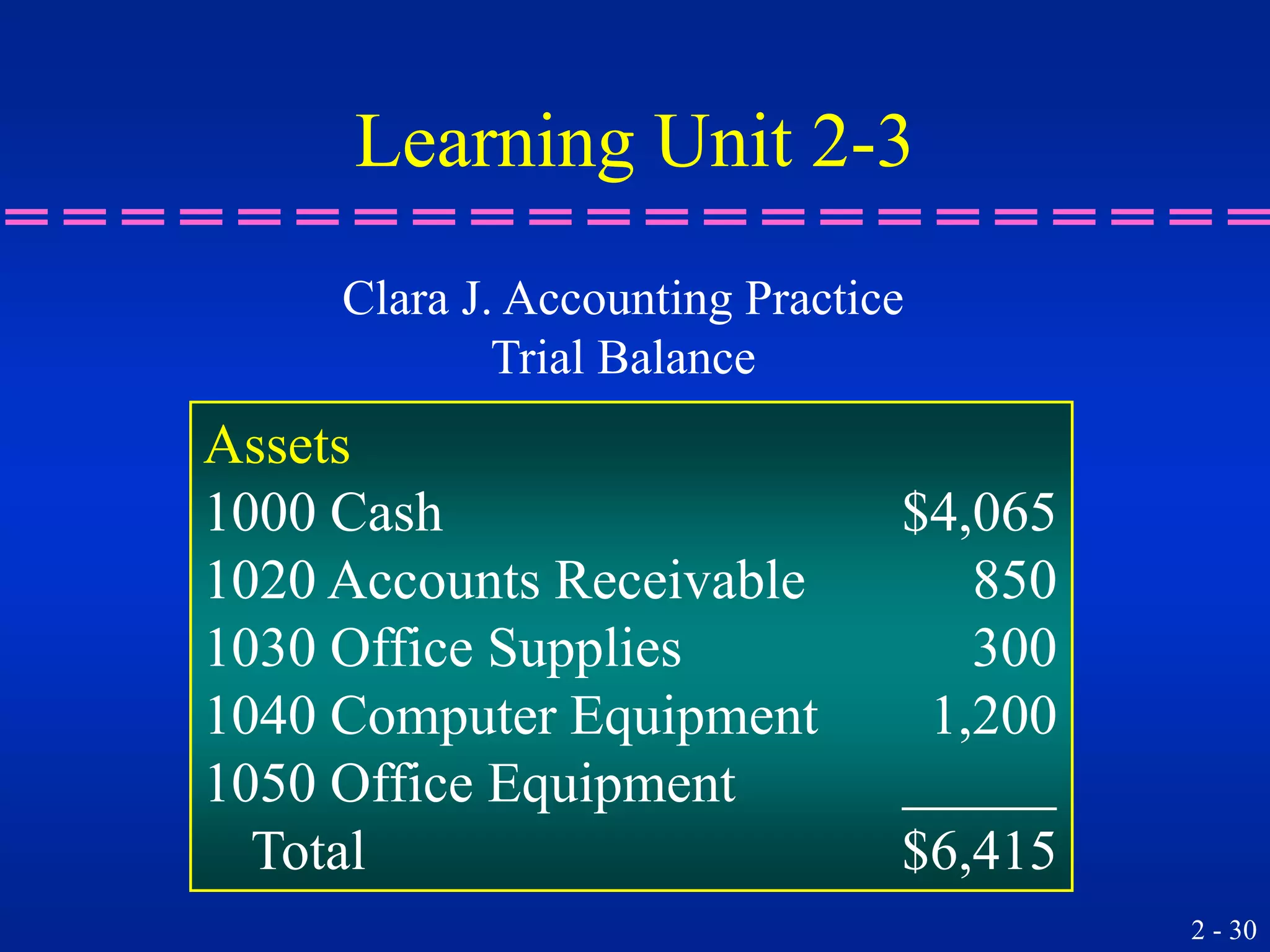

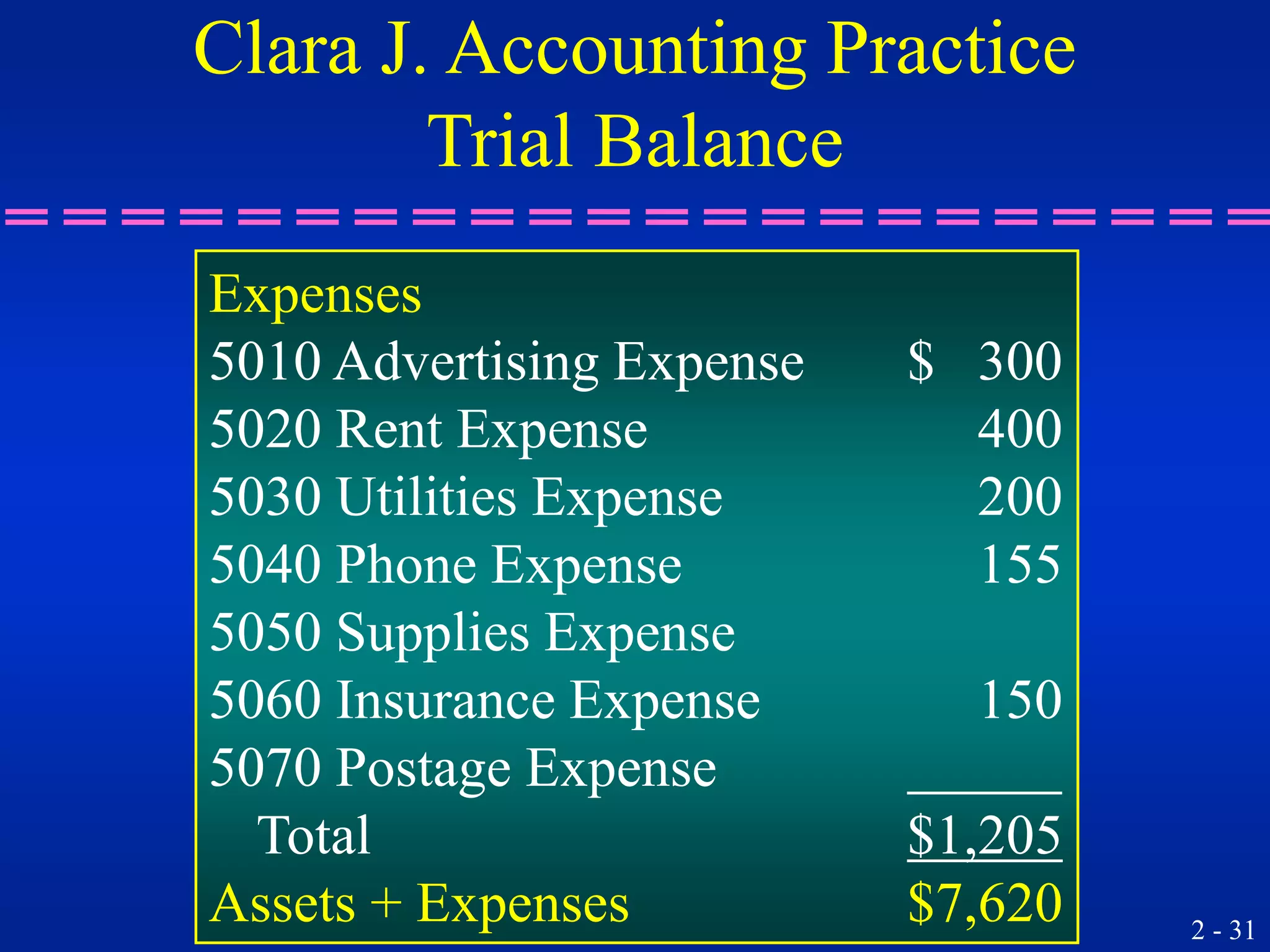

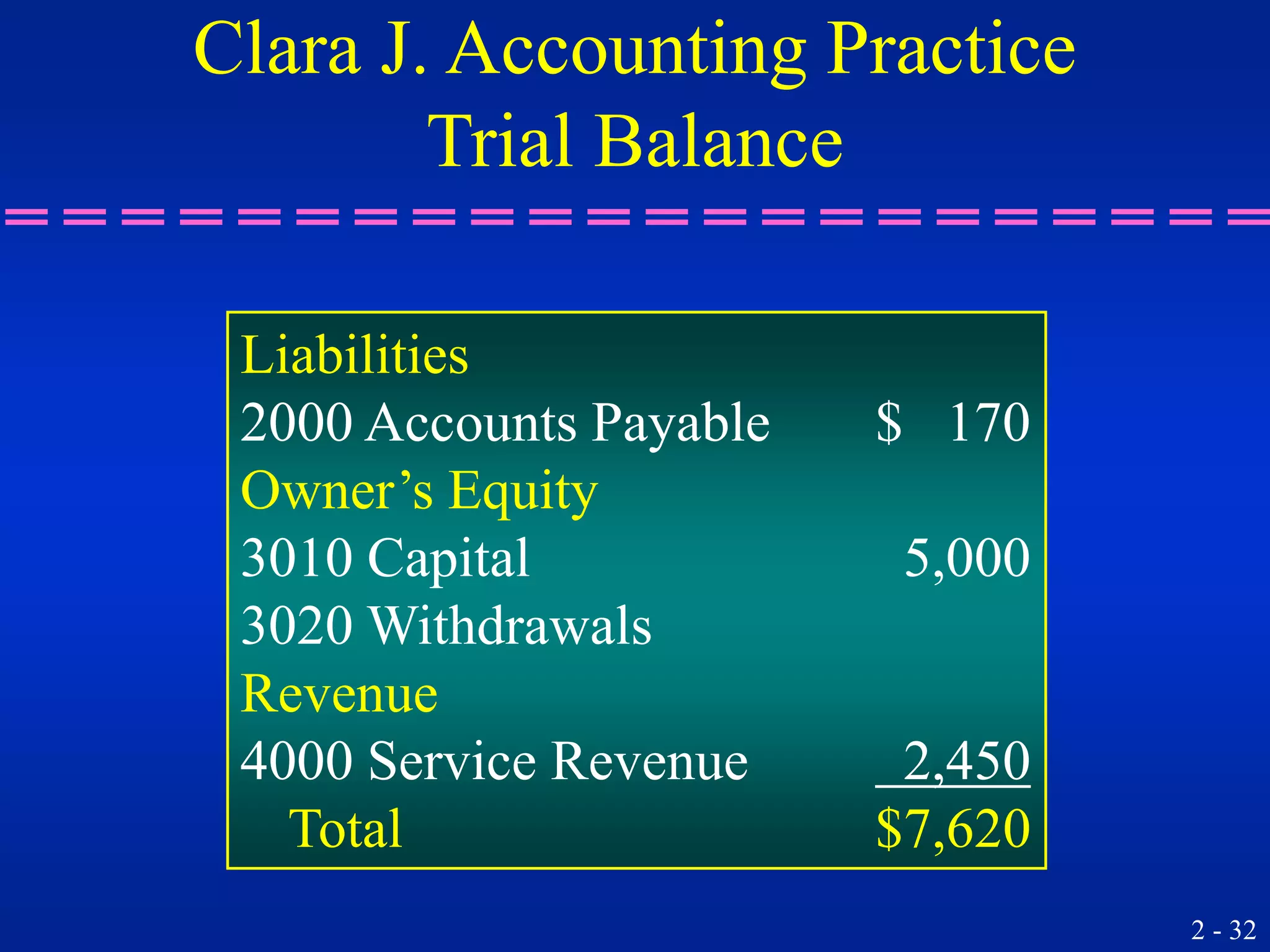

4. Preparing a trial balance from the journal entries to check that accounts balance.

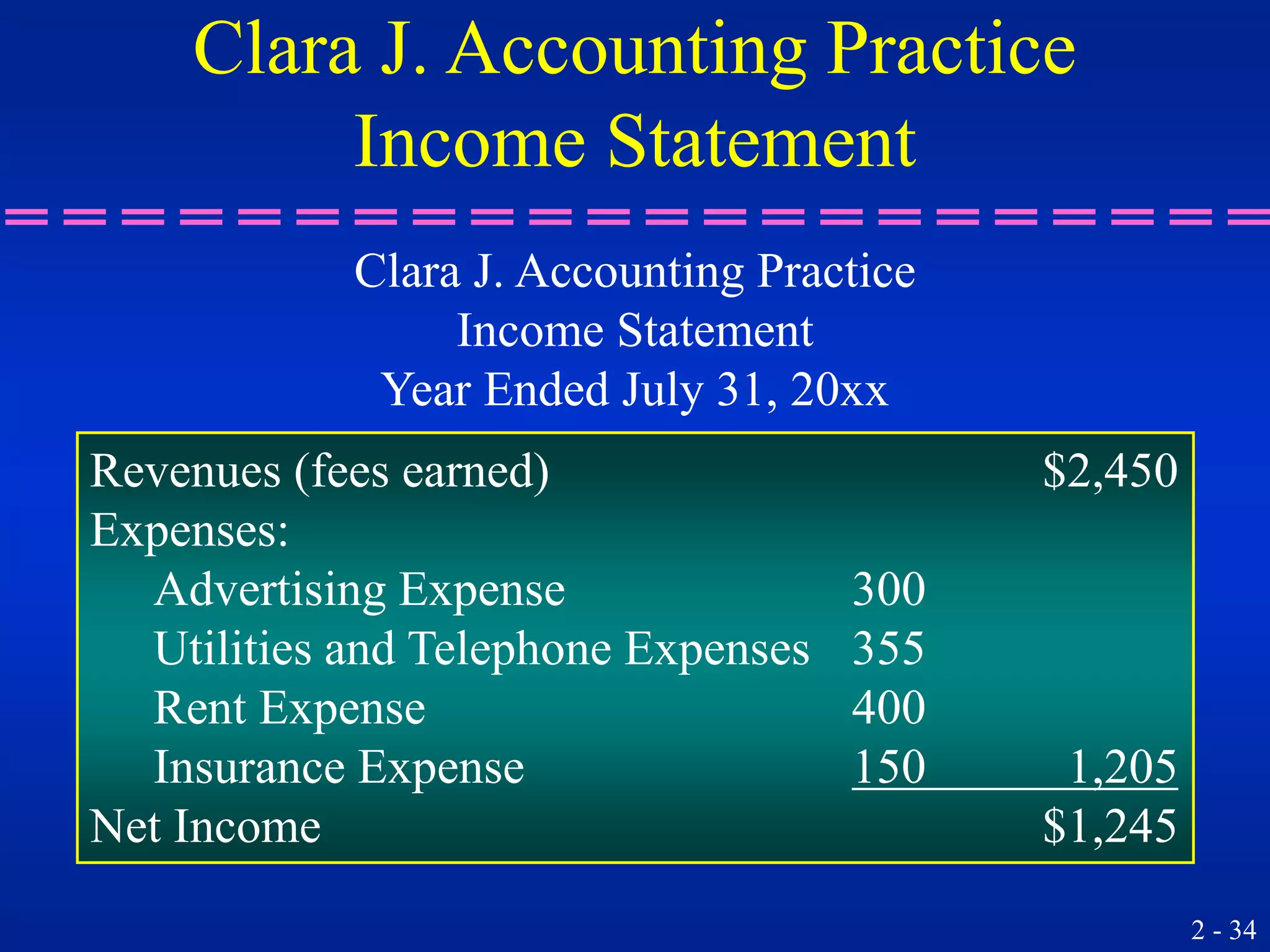

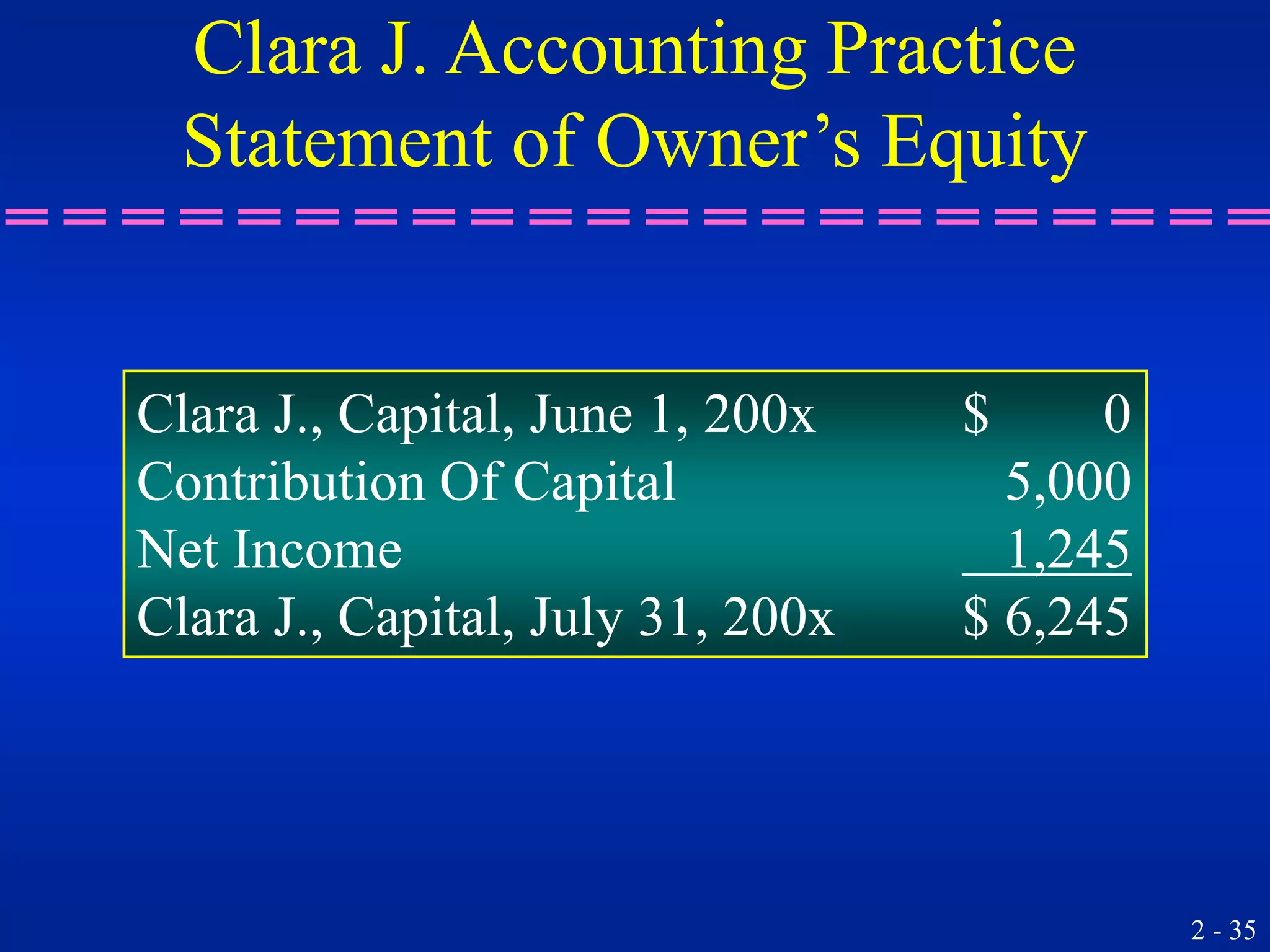

5. Using the trial balance to generate basic financial statements - the income statement, statement of owner's equity, and balance sheet.