Downloaded 18 times

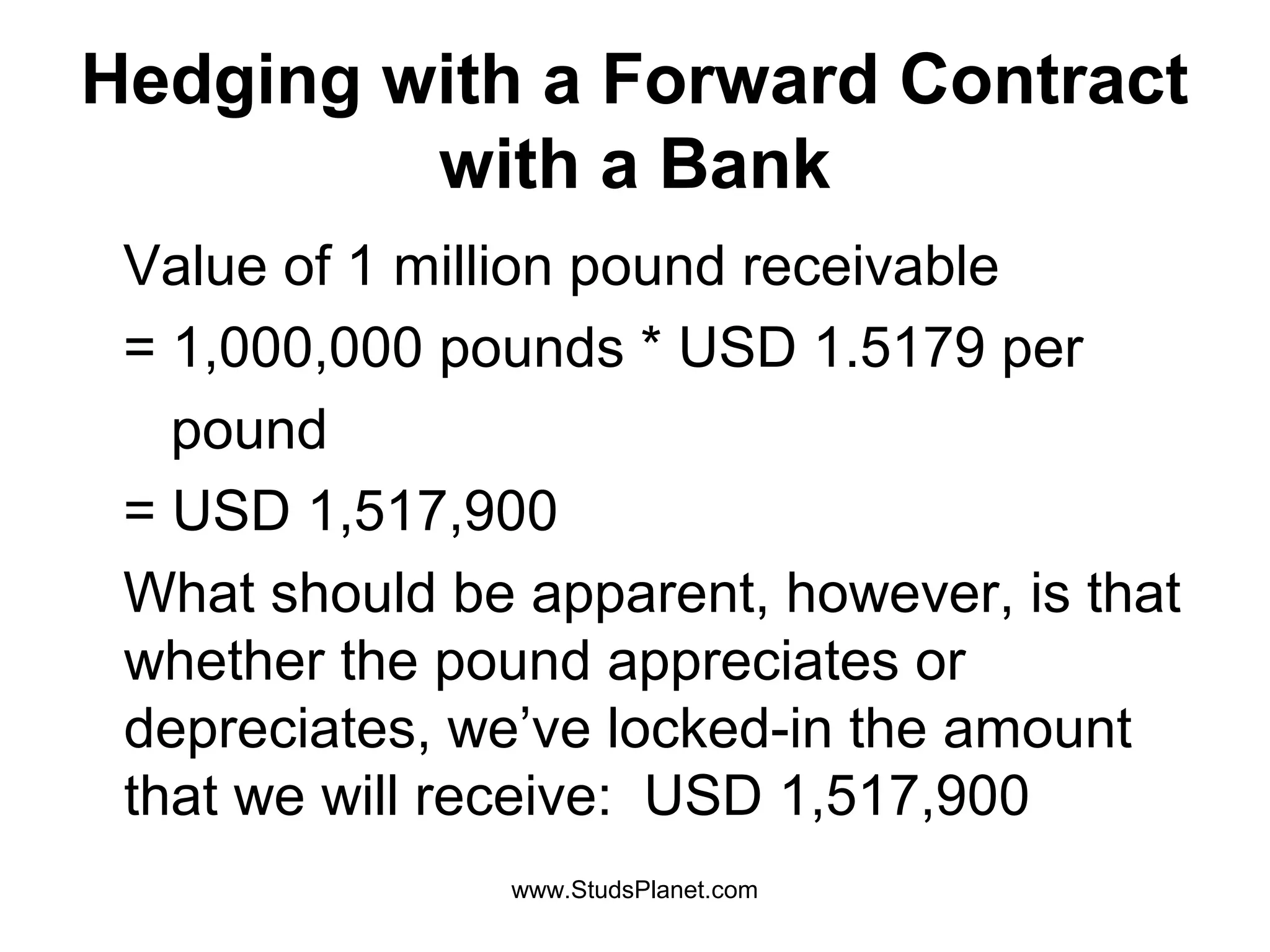

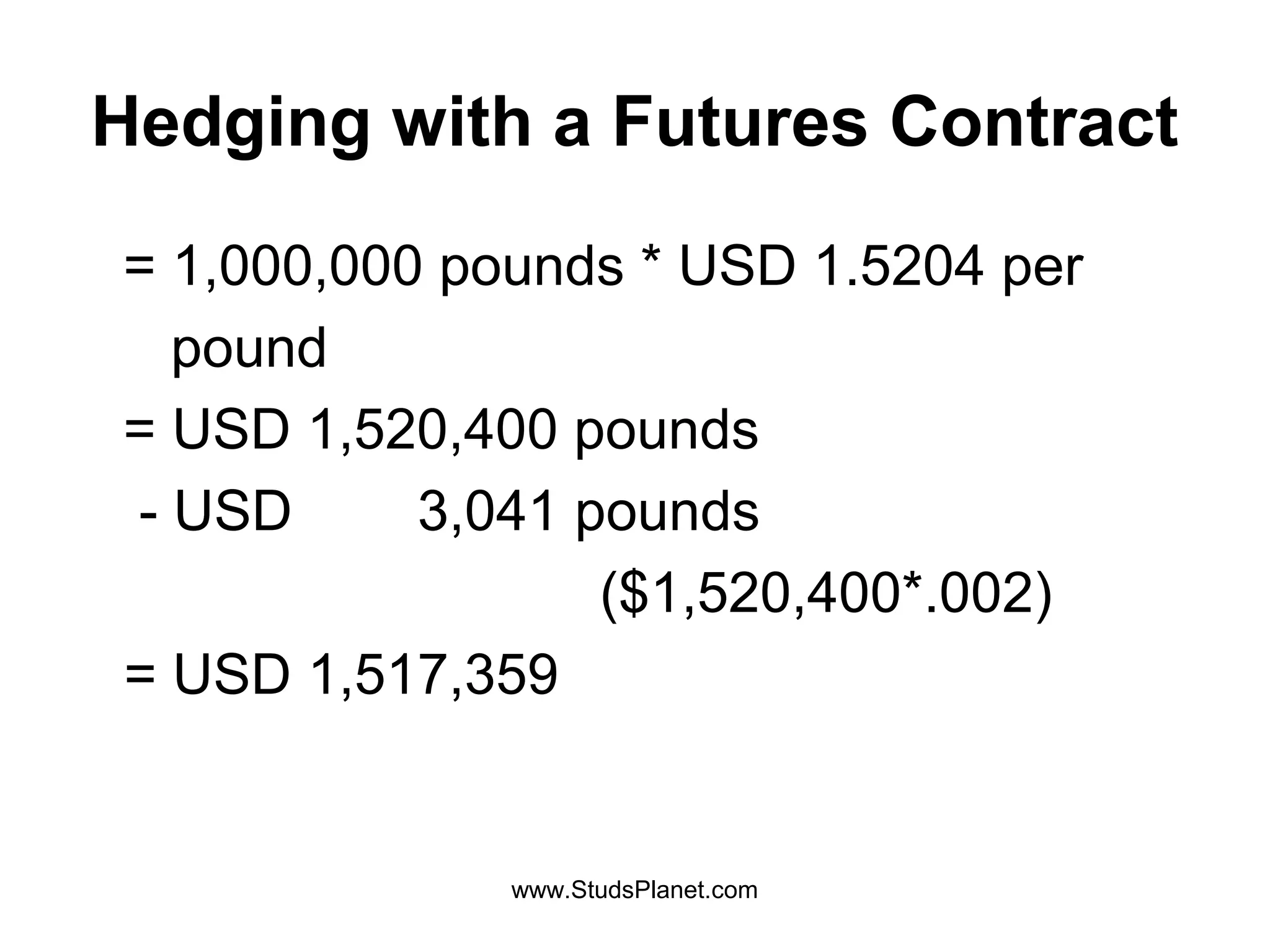

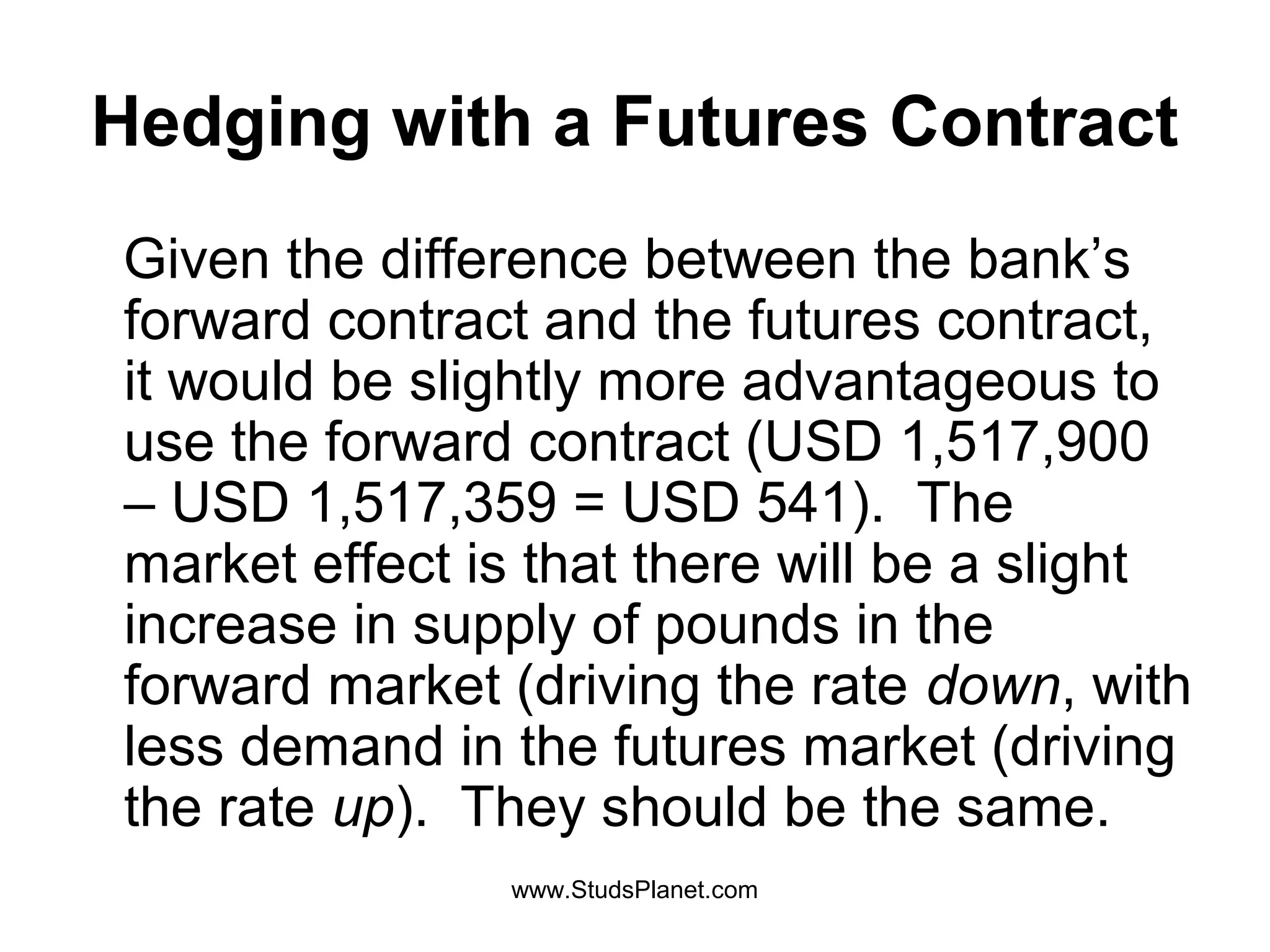

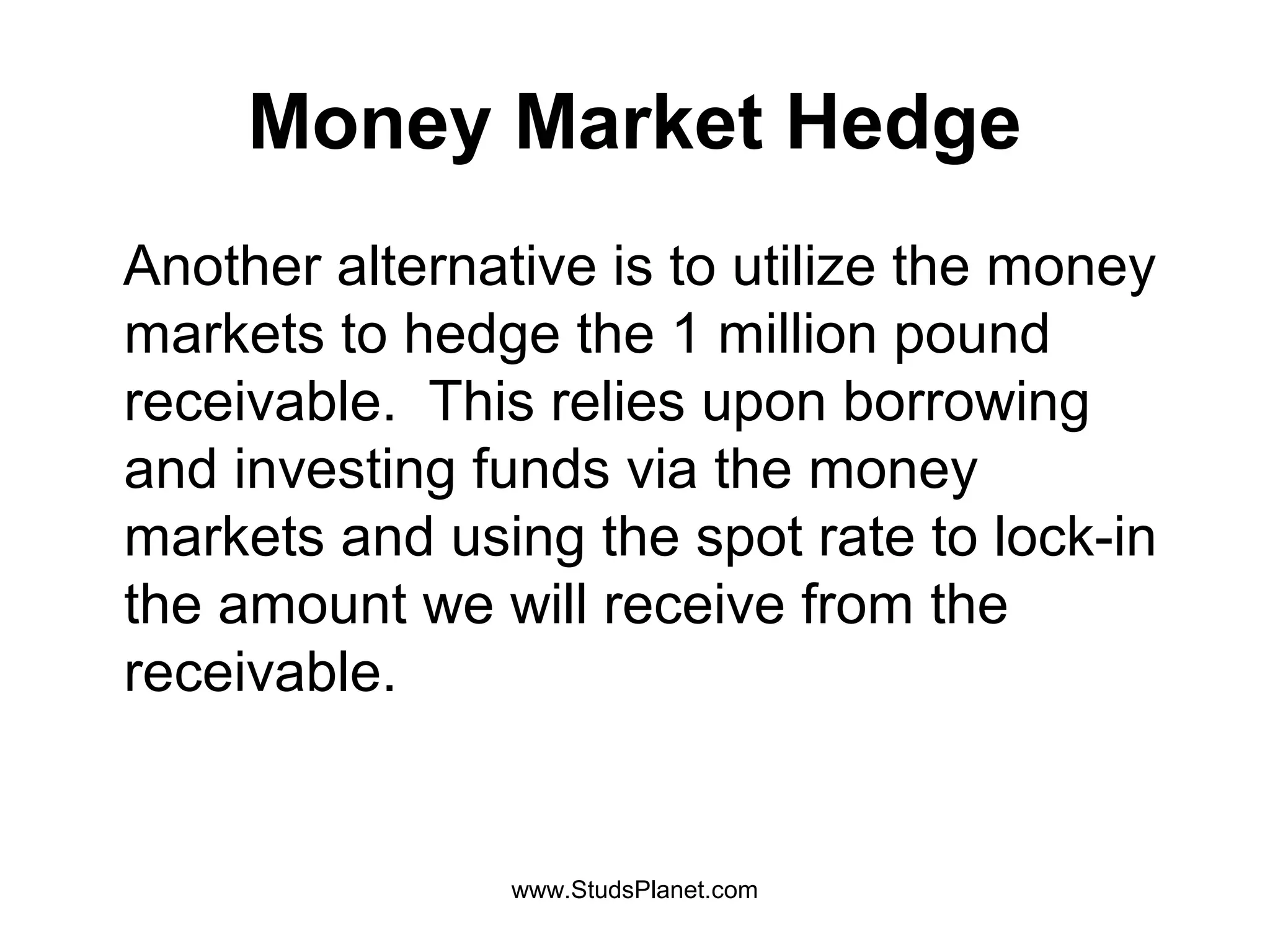

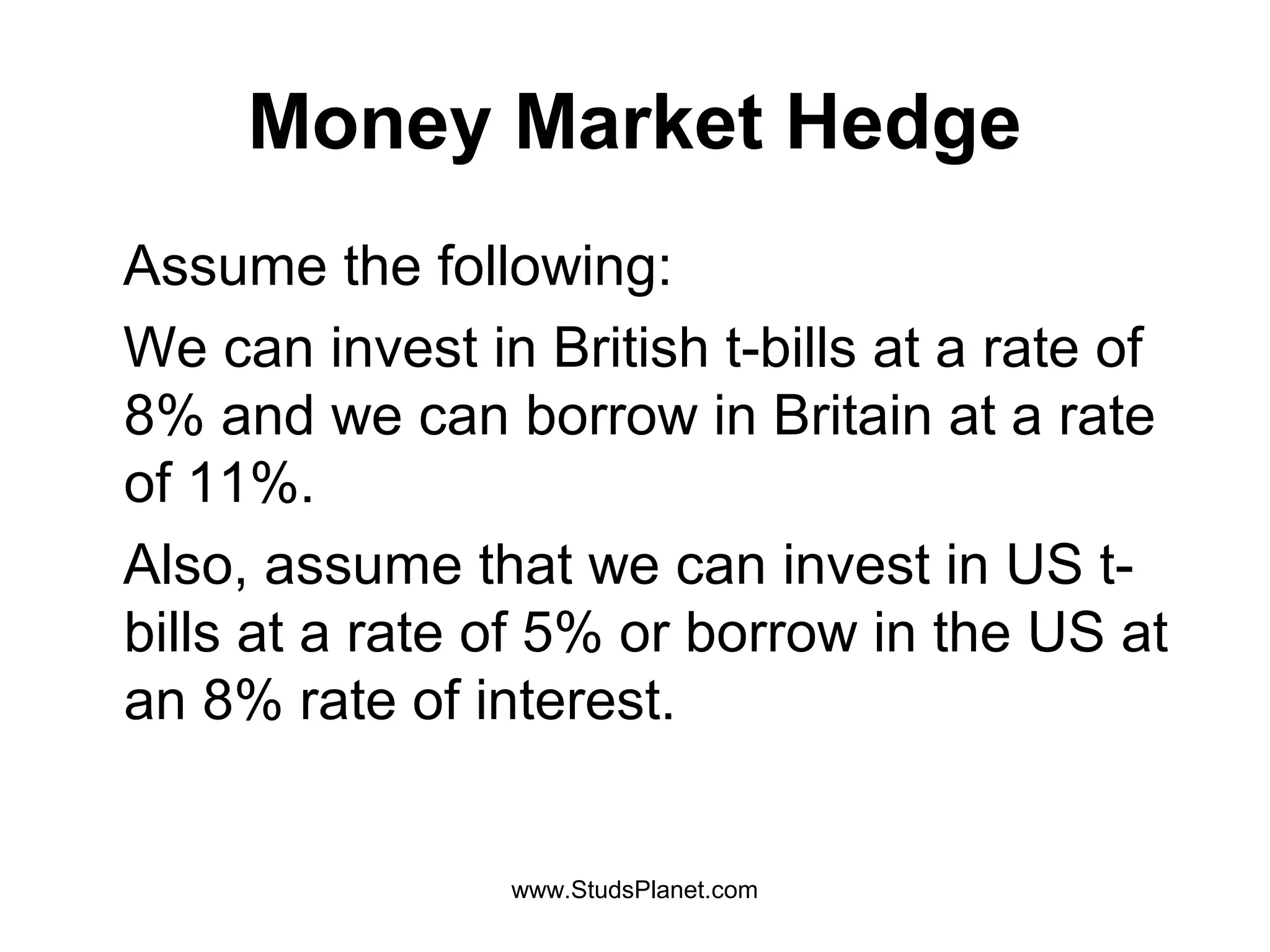

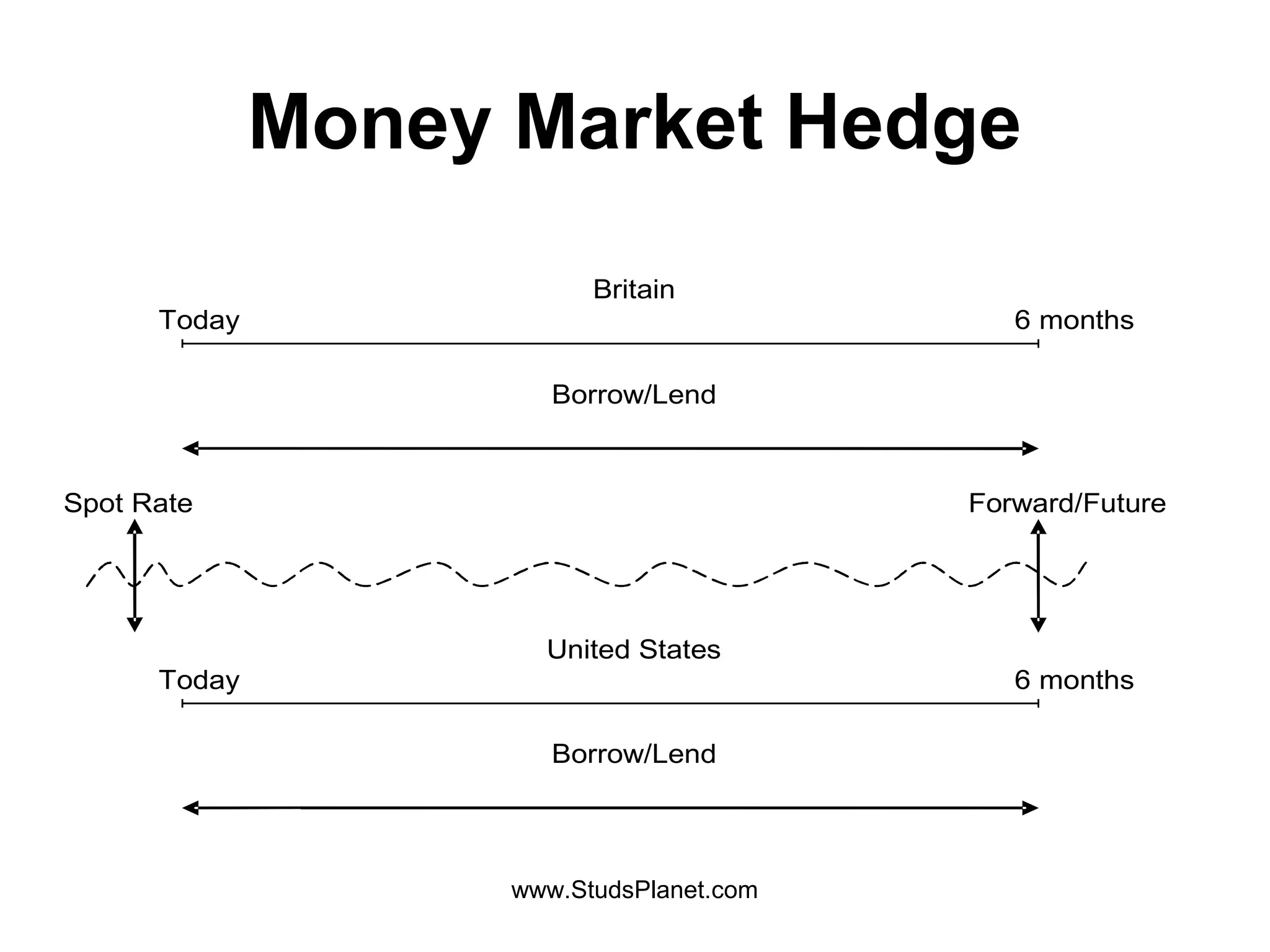

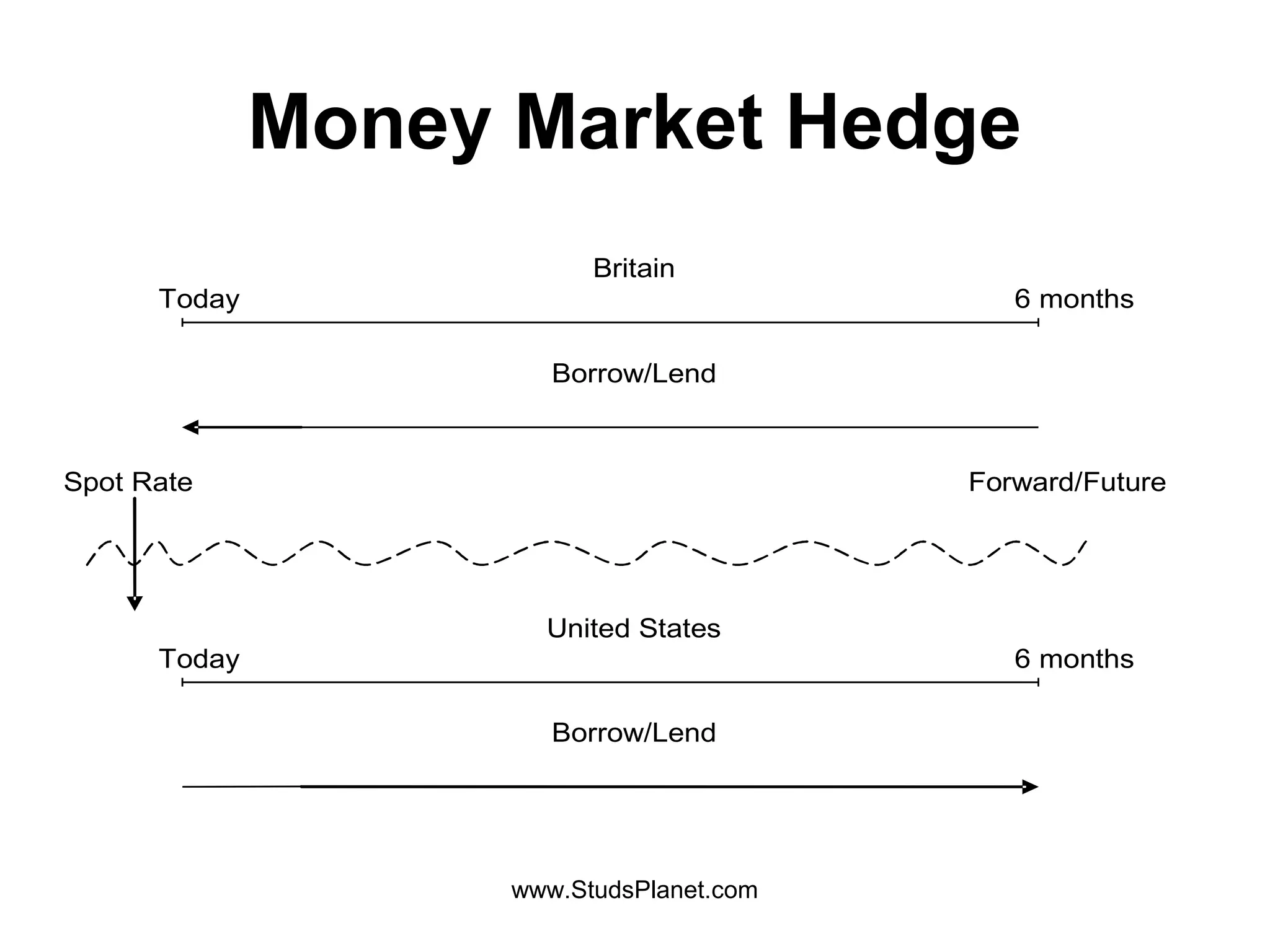

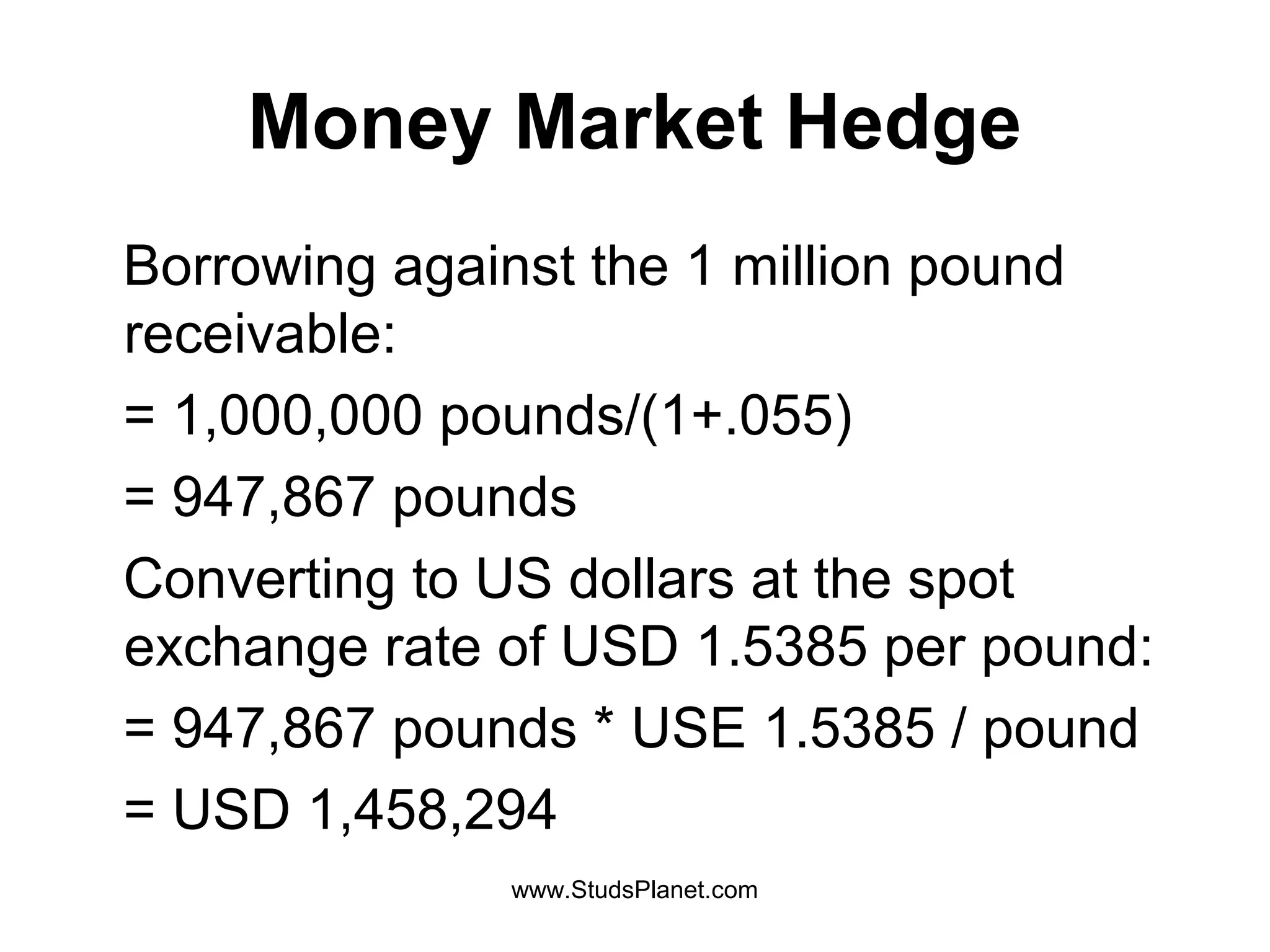

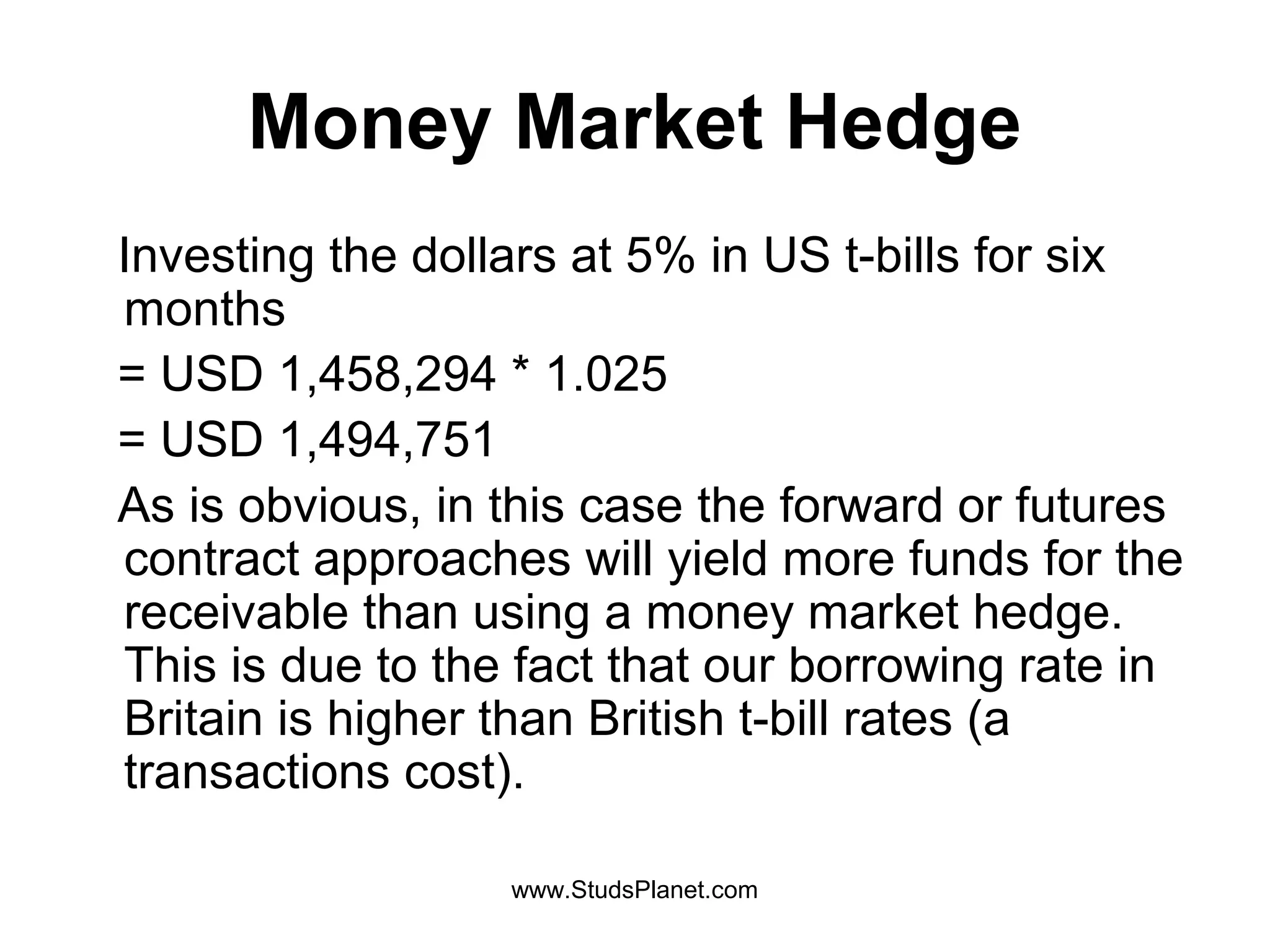

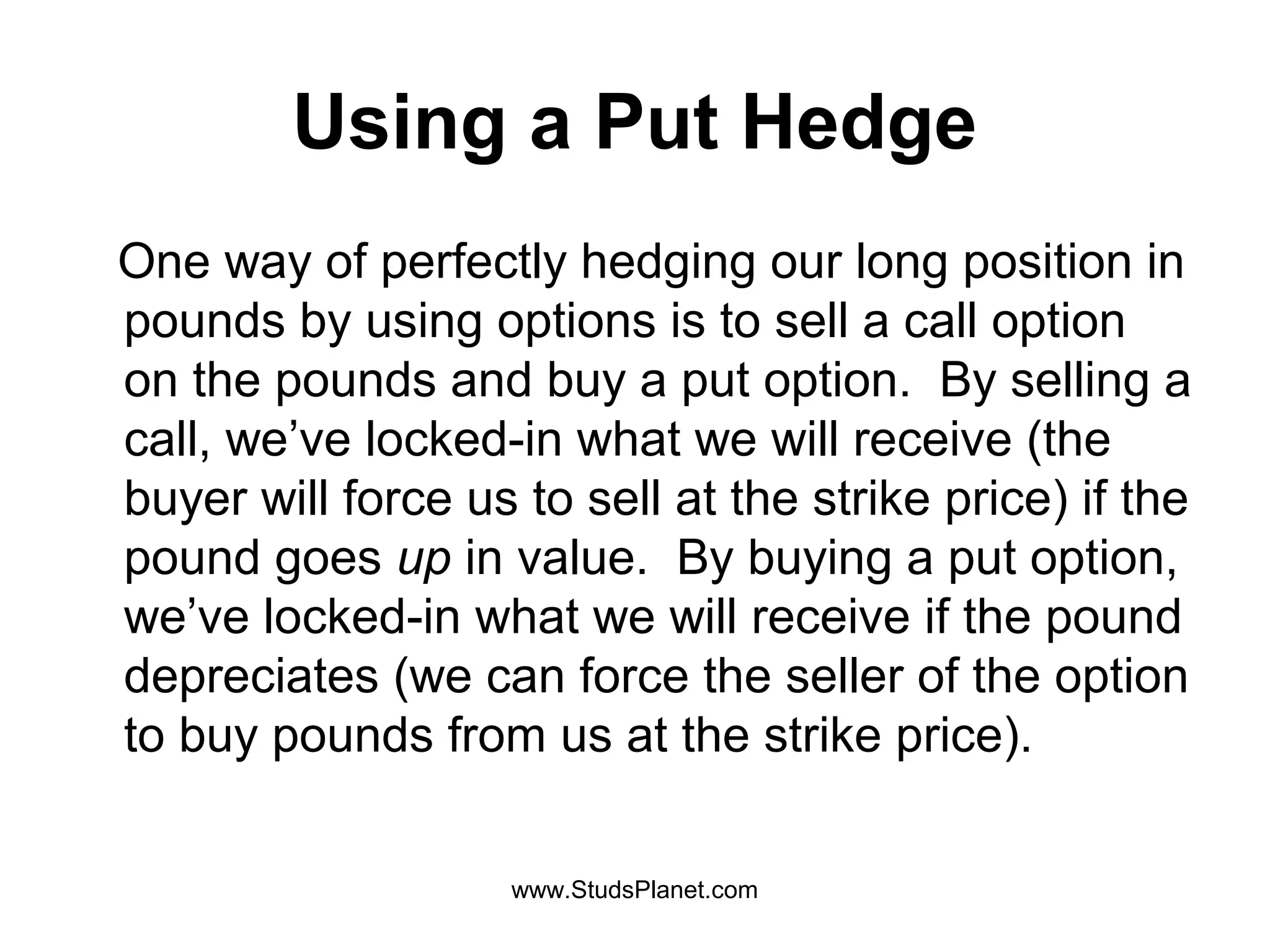

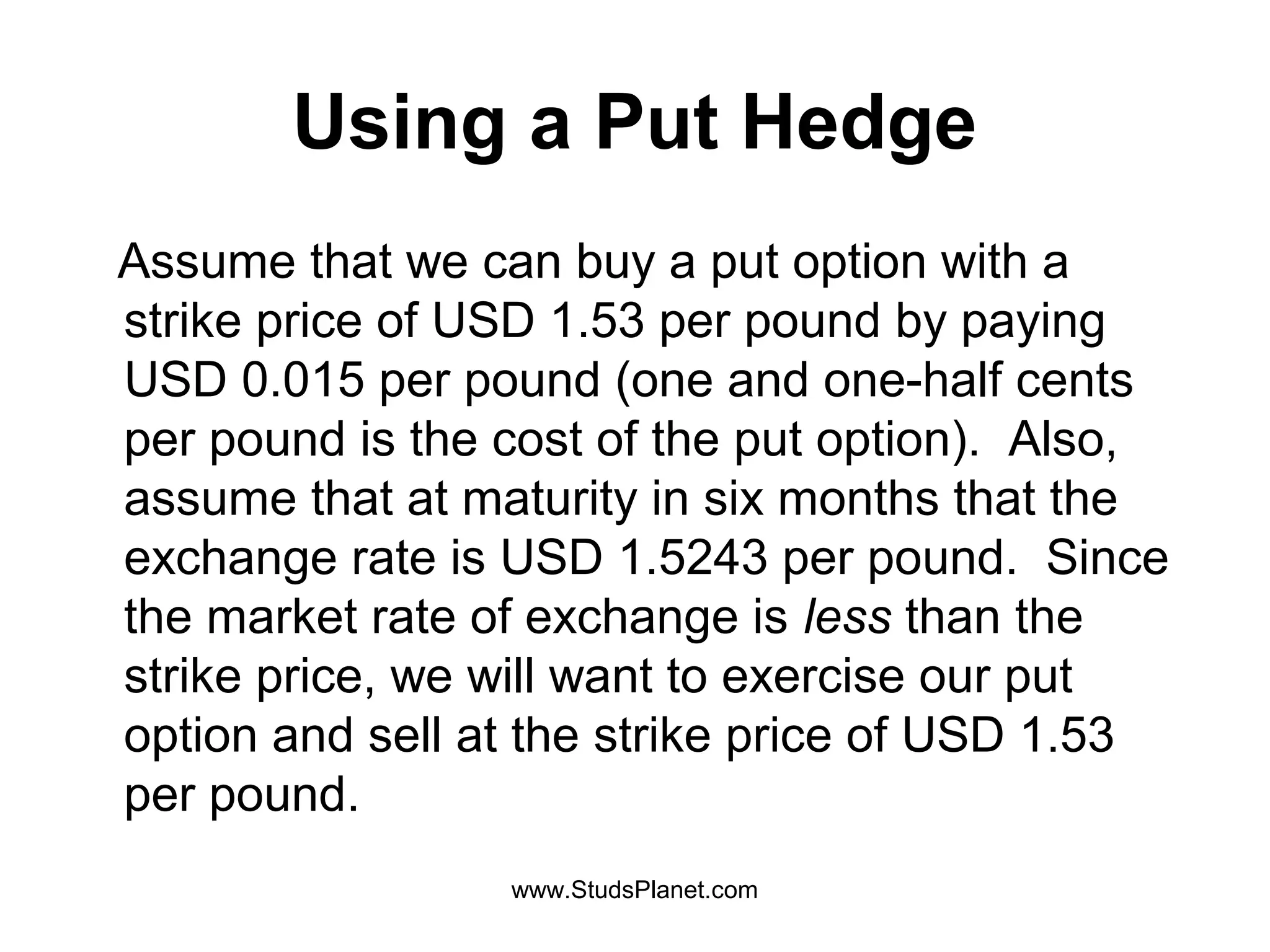

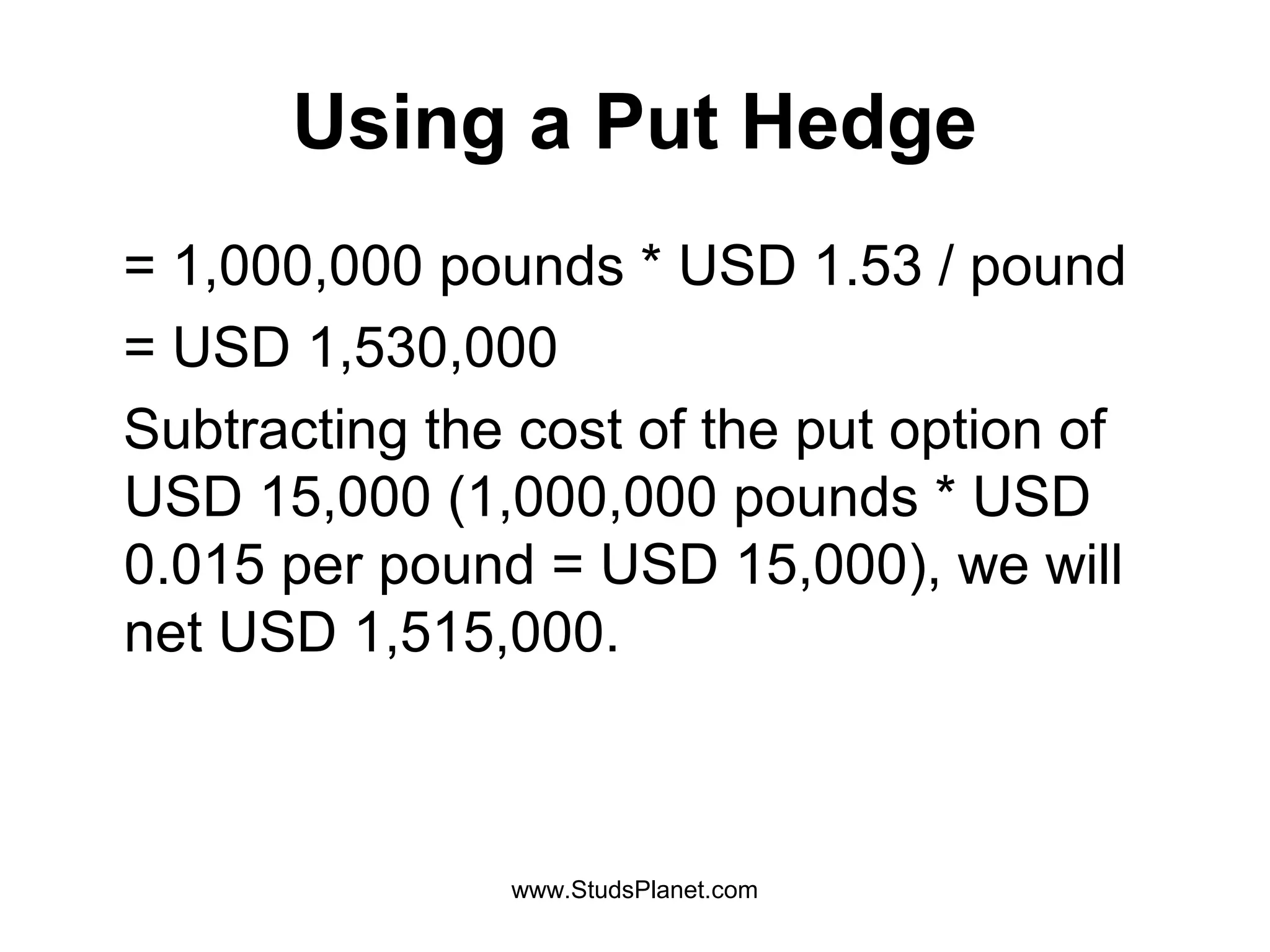

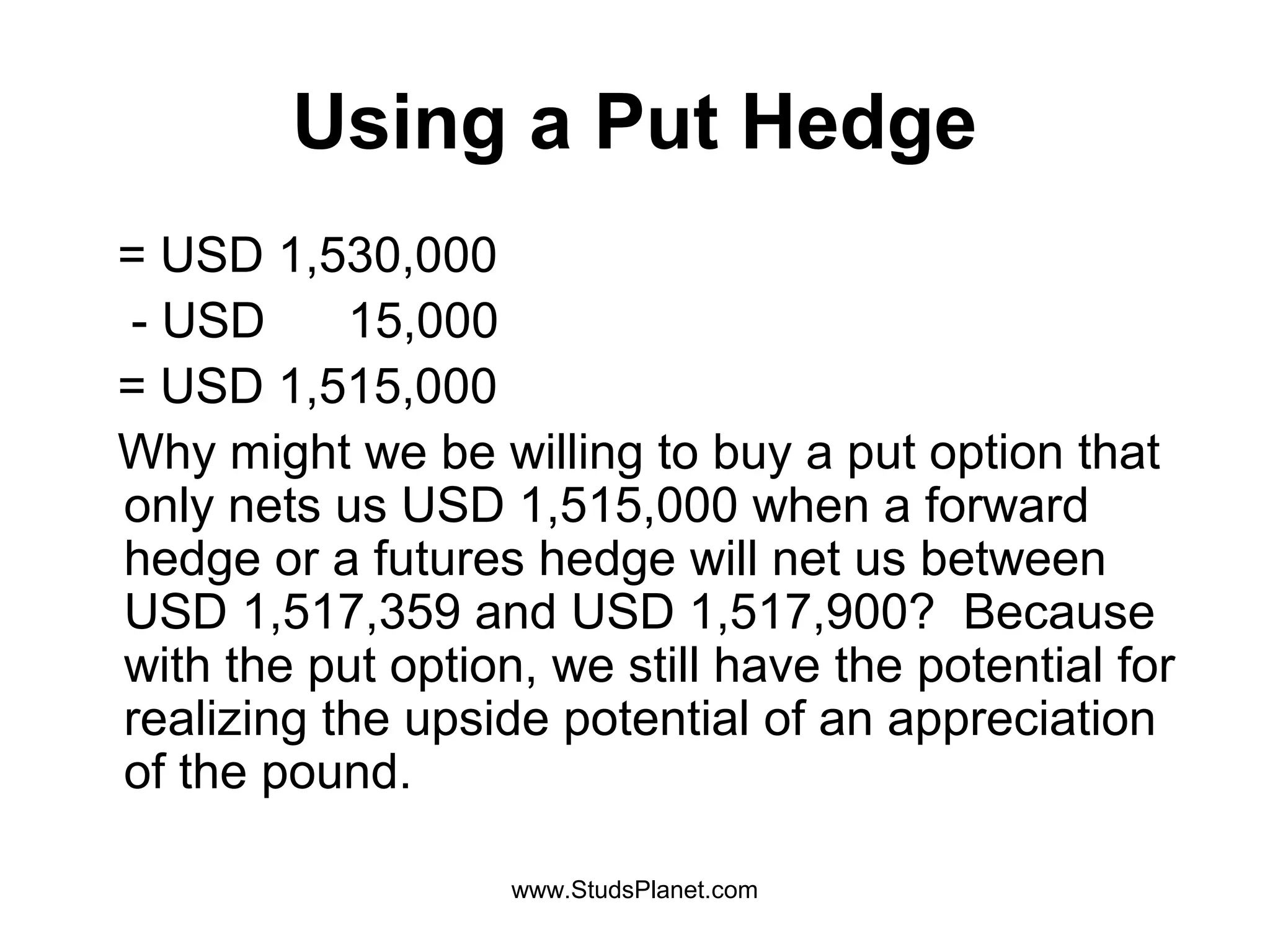

The document discusses several methods for hedging against currency risk when receiving 1 million British pounds in 6 months, including: 1) Entering a forward contract with a bank at 1.5179 USD/GBP, guaranteeing receipt of USD 1,517,900. 2) Using futures contracts at 1.5204 USD/GBP, netting USD 1,517,359 after commissions. 3) Borrowing pounds at 11% interest and converting/investing dollars at a 5% rate, receiving less than the forward methods. 4) Buying a put option at 1.53 USD/GBP for a net of USD 1,515,000, but retaining upside potential if