Downloaded 20 times

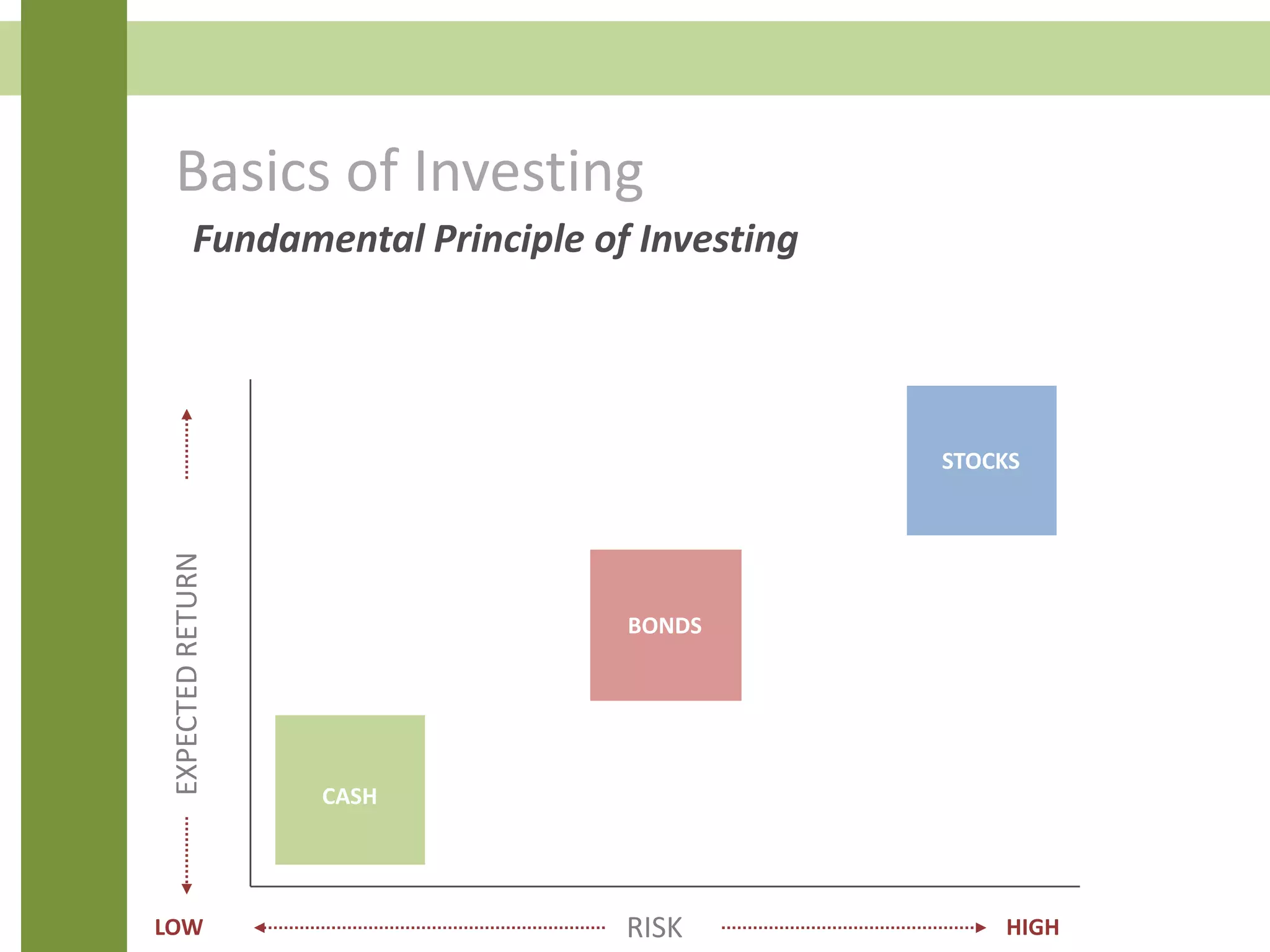

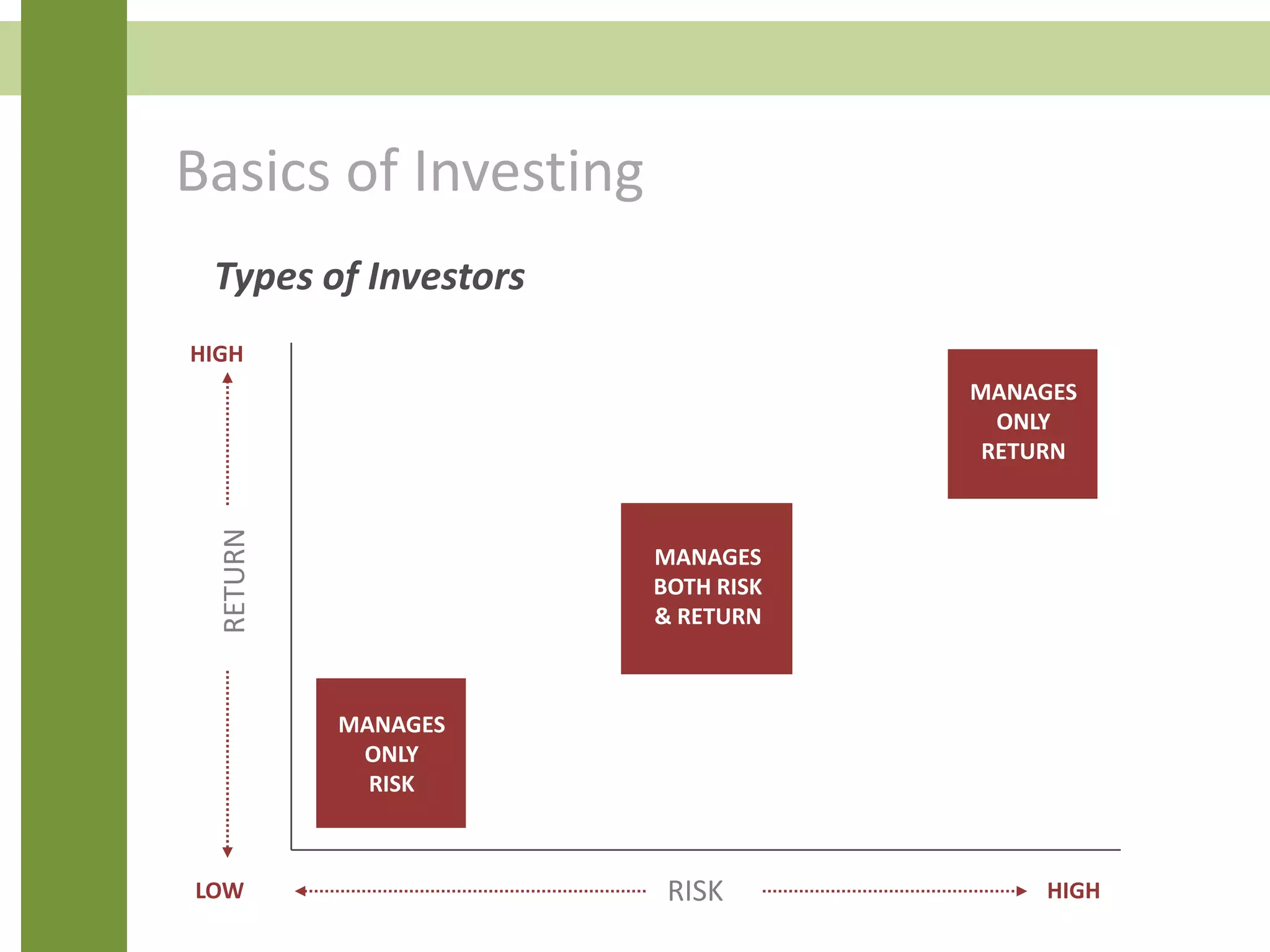

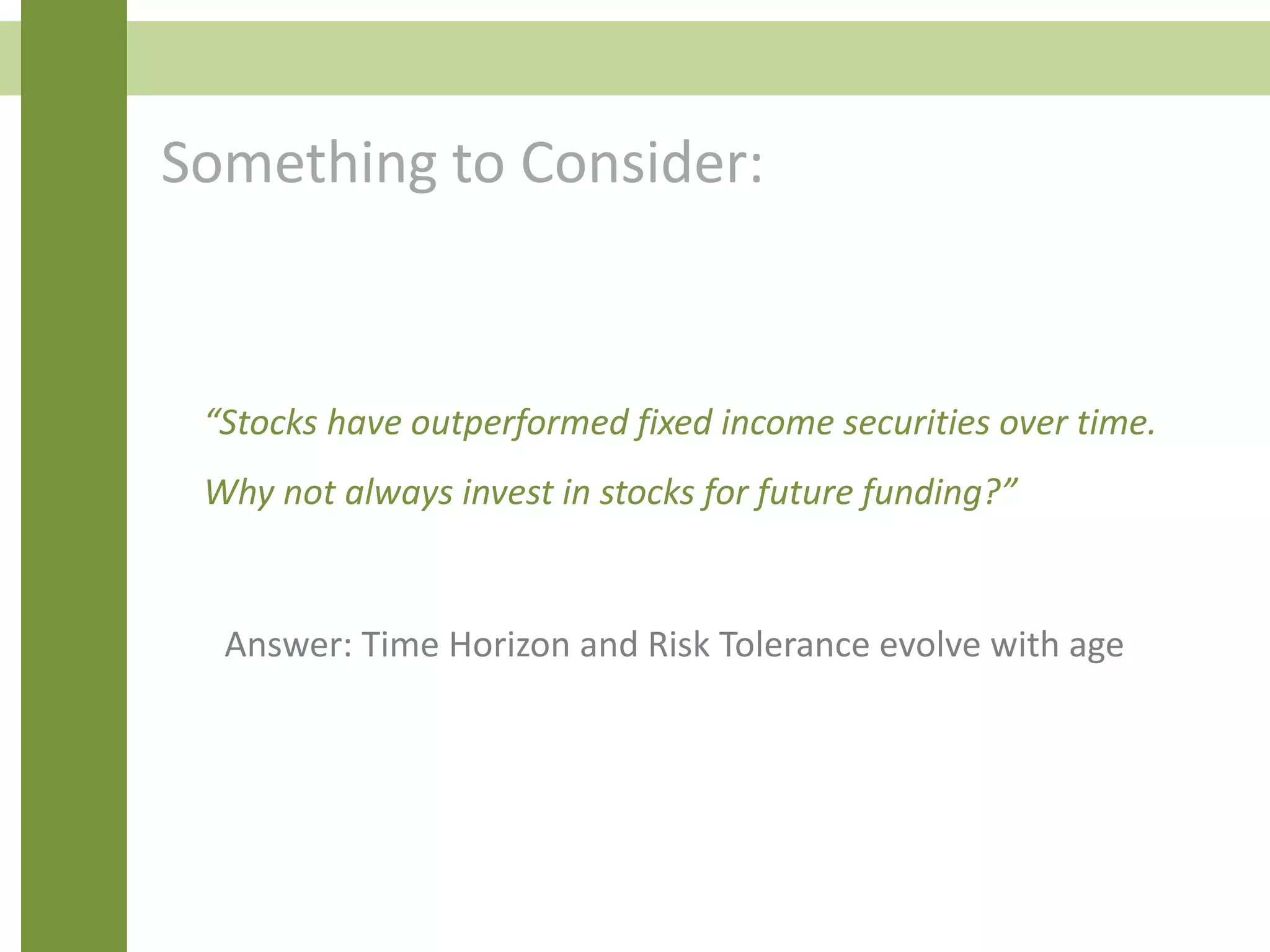

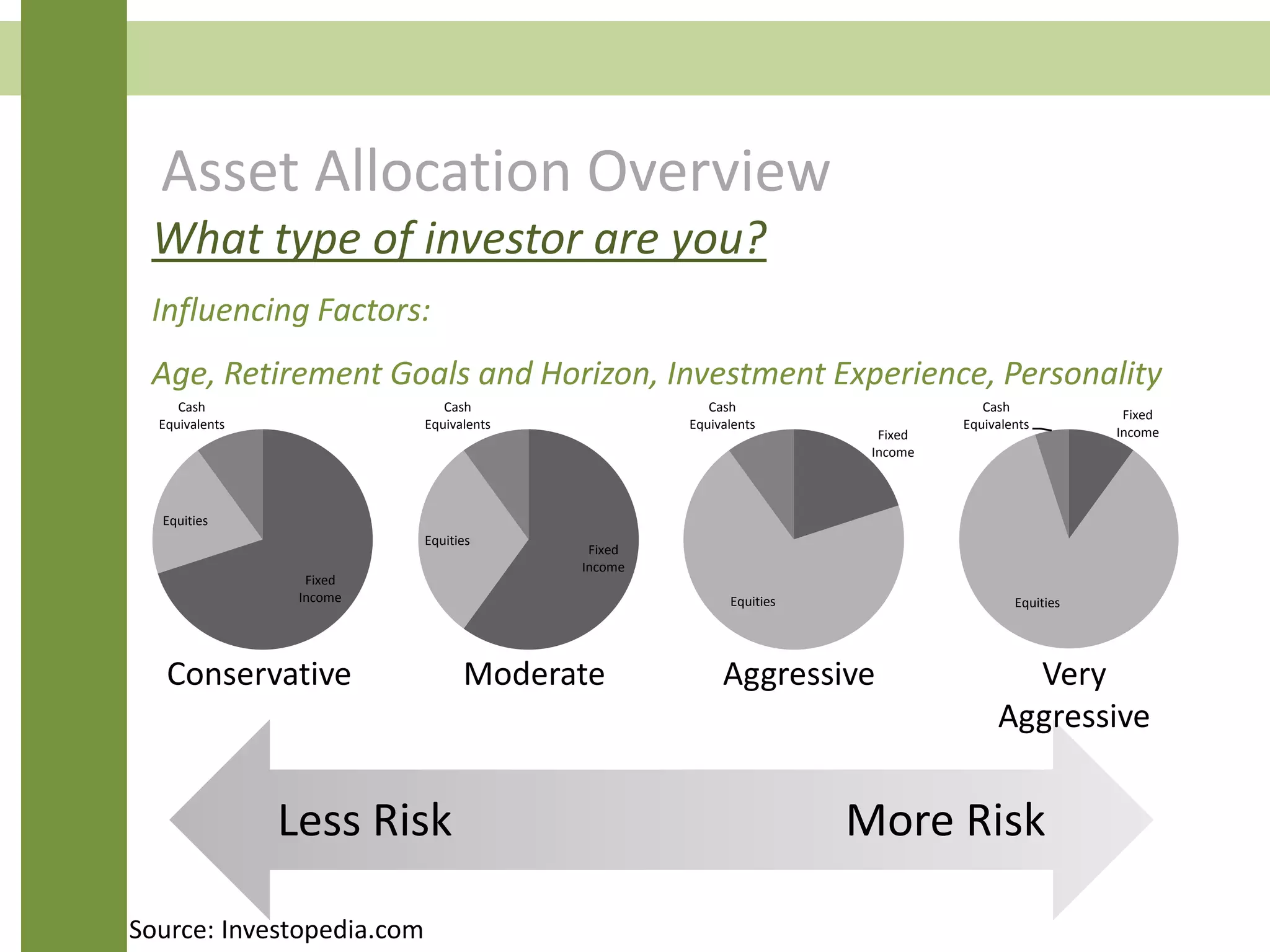

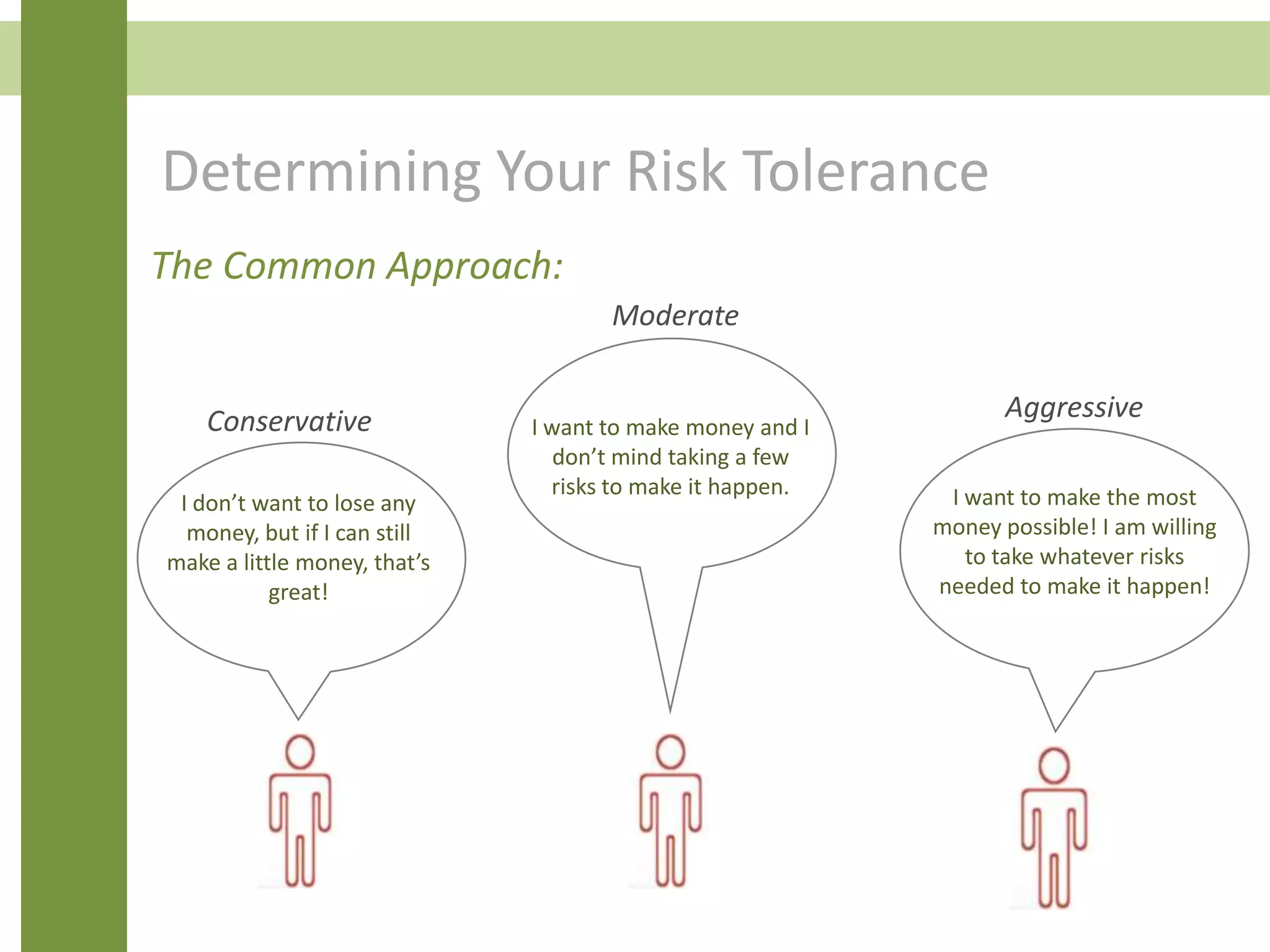

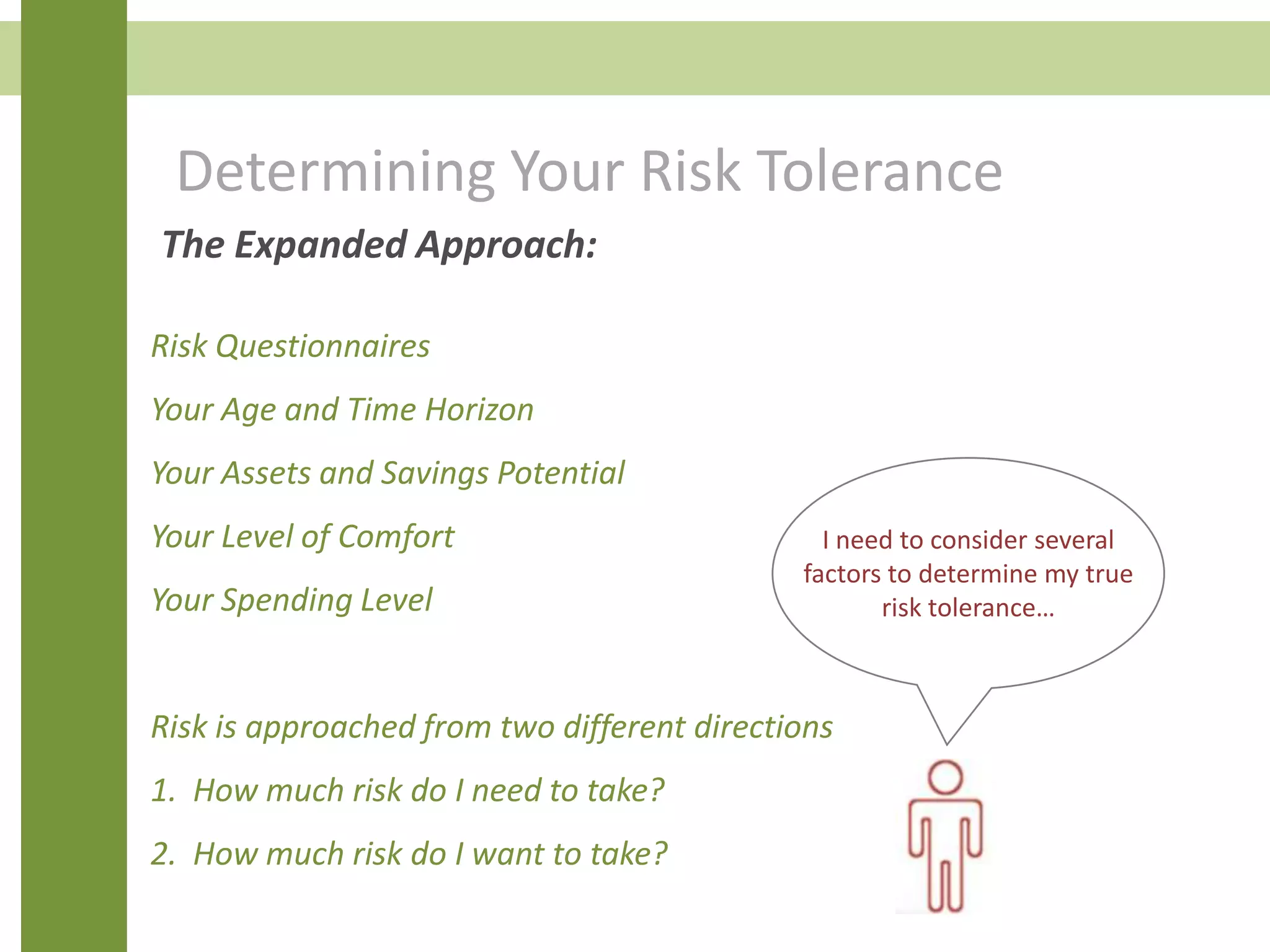

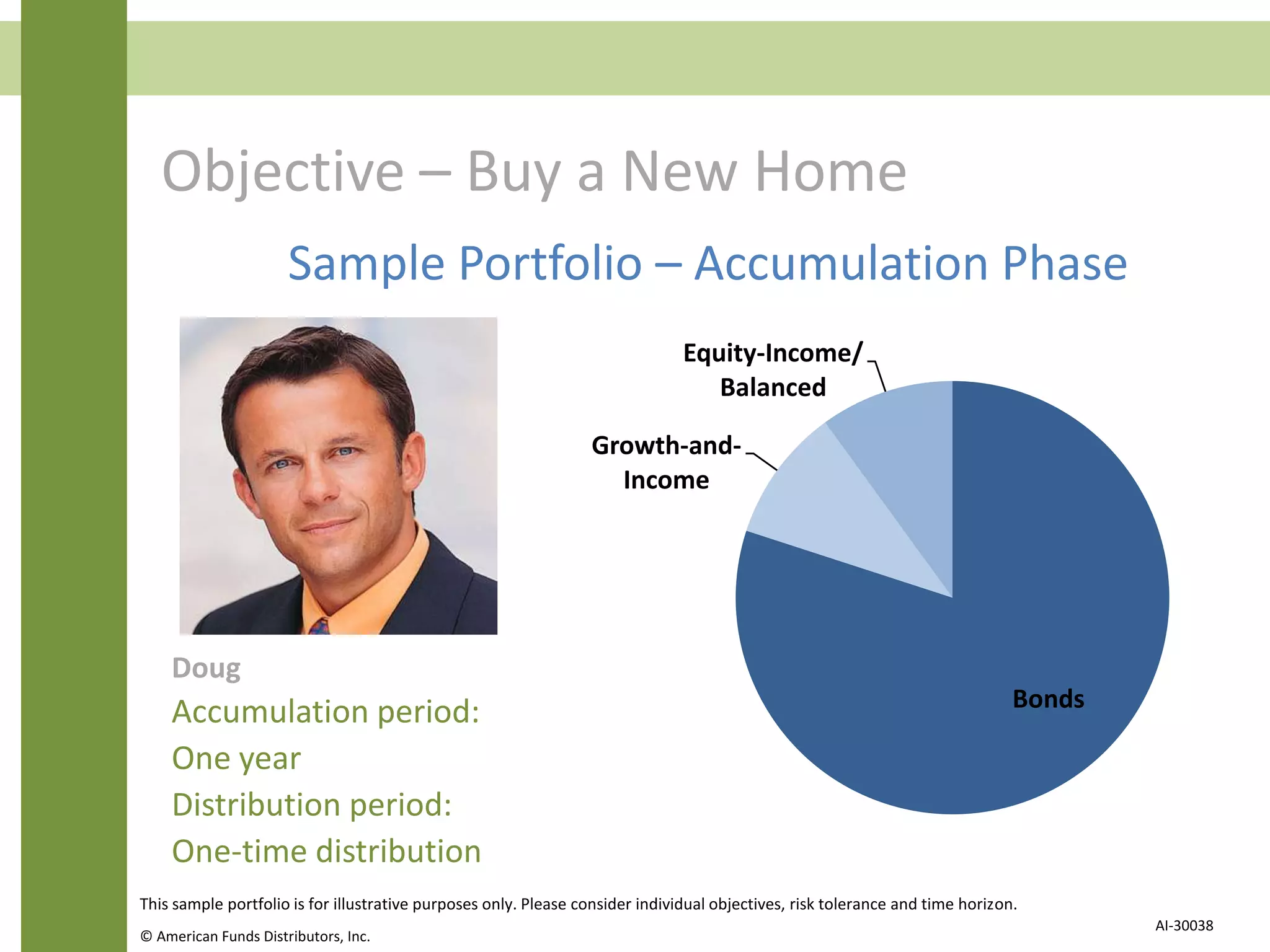

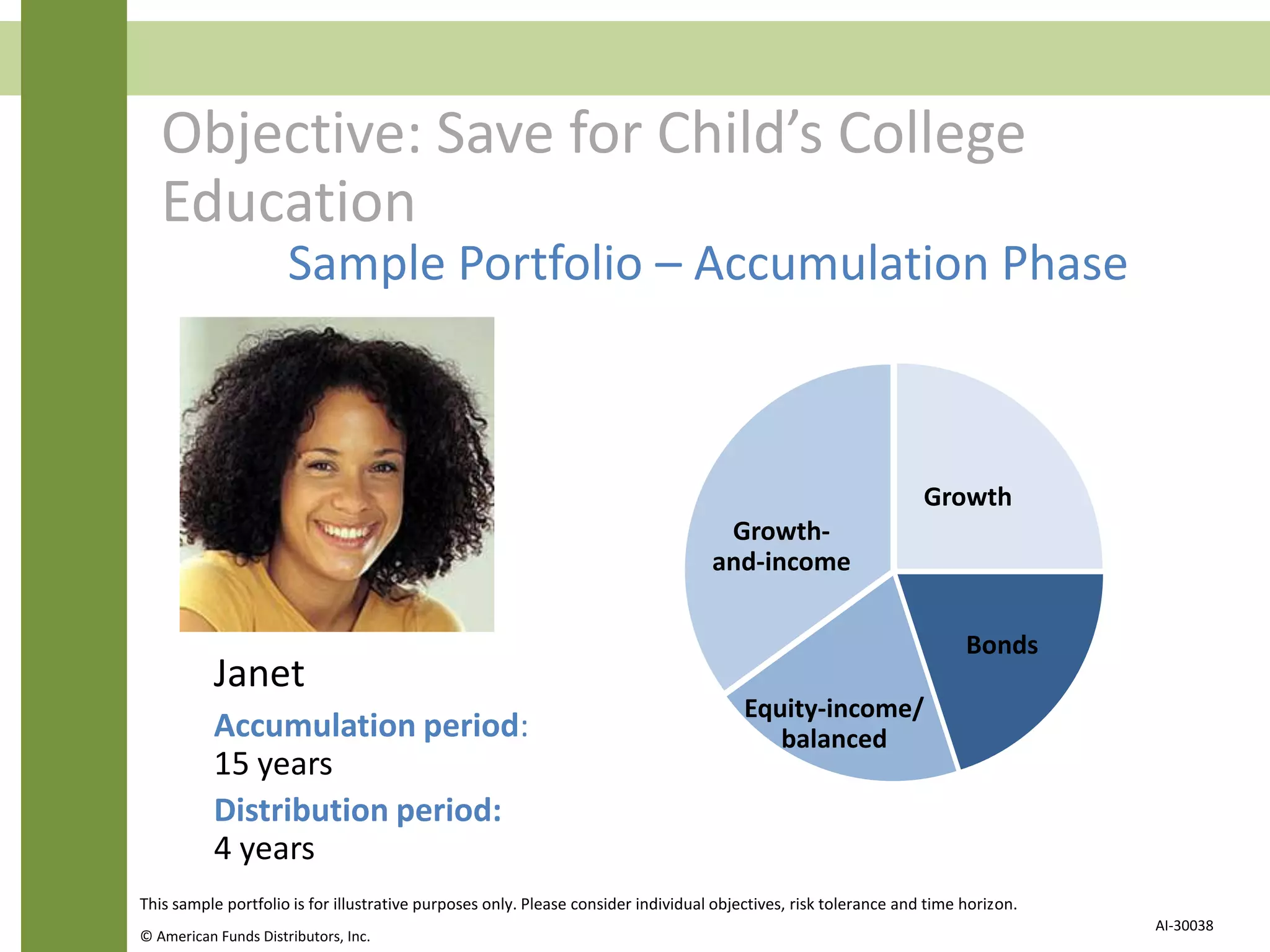

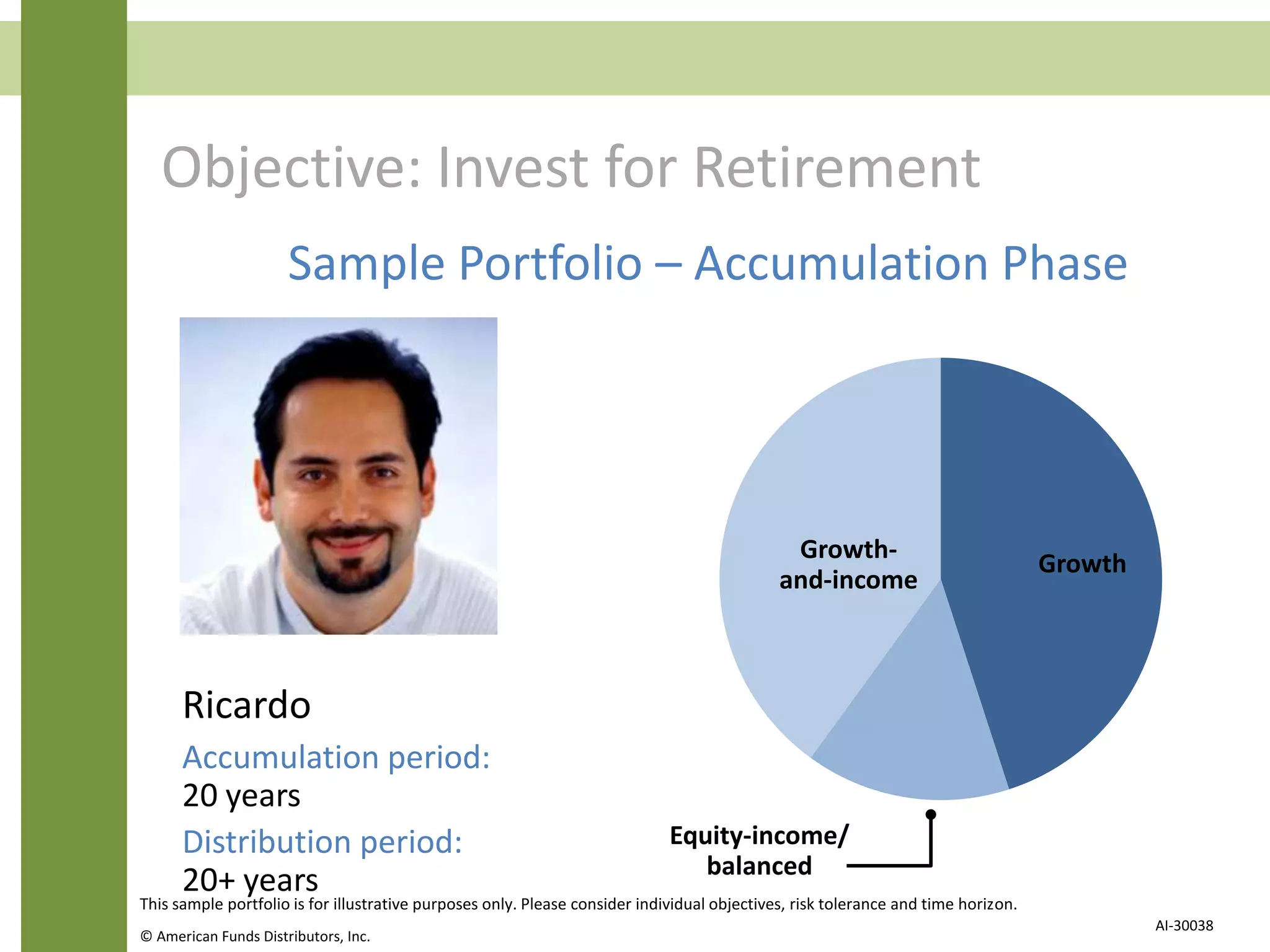

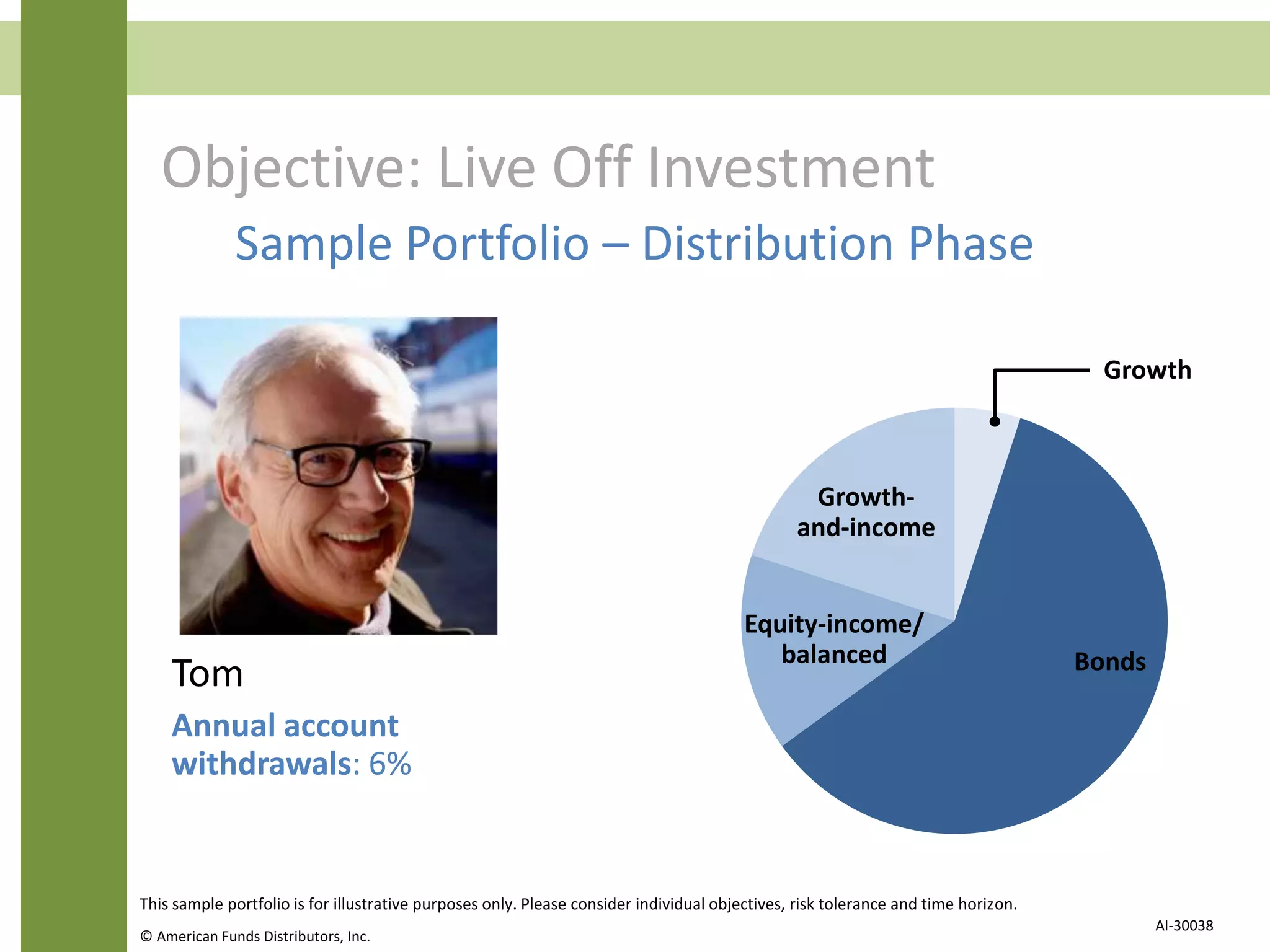

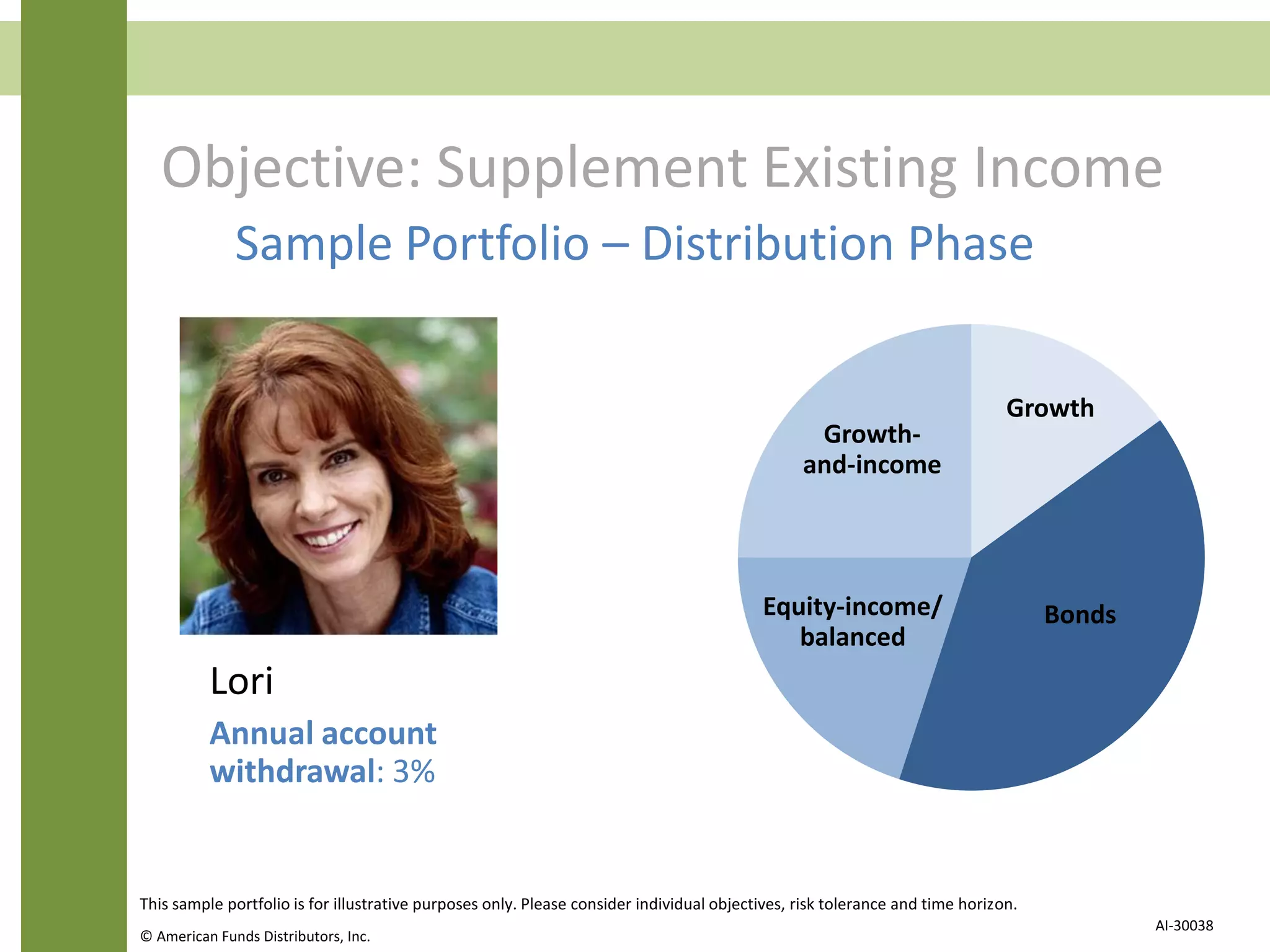

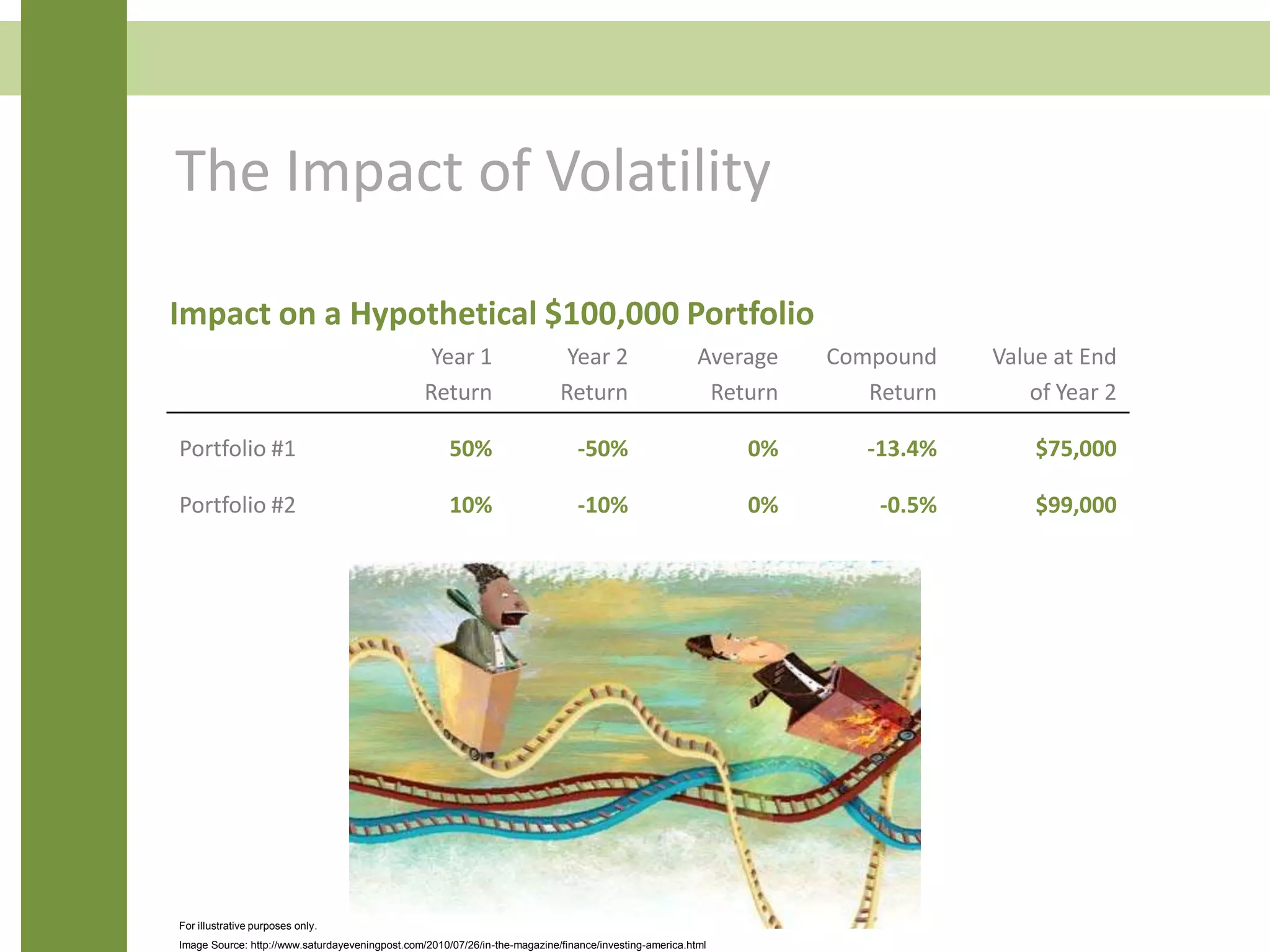

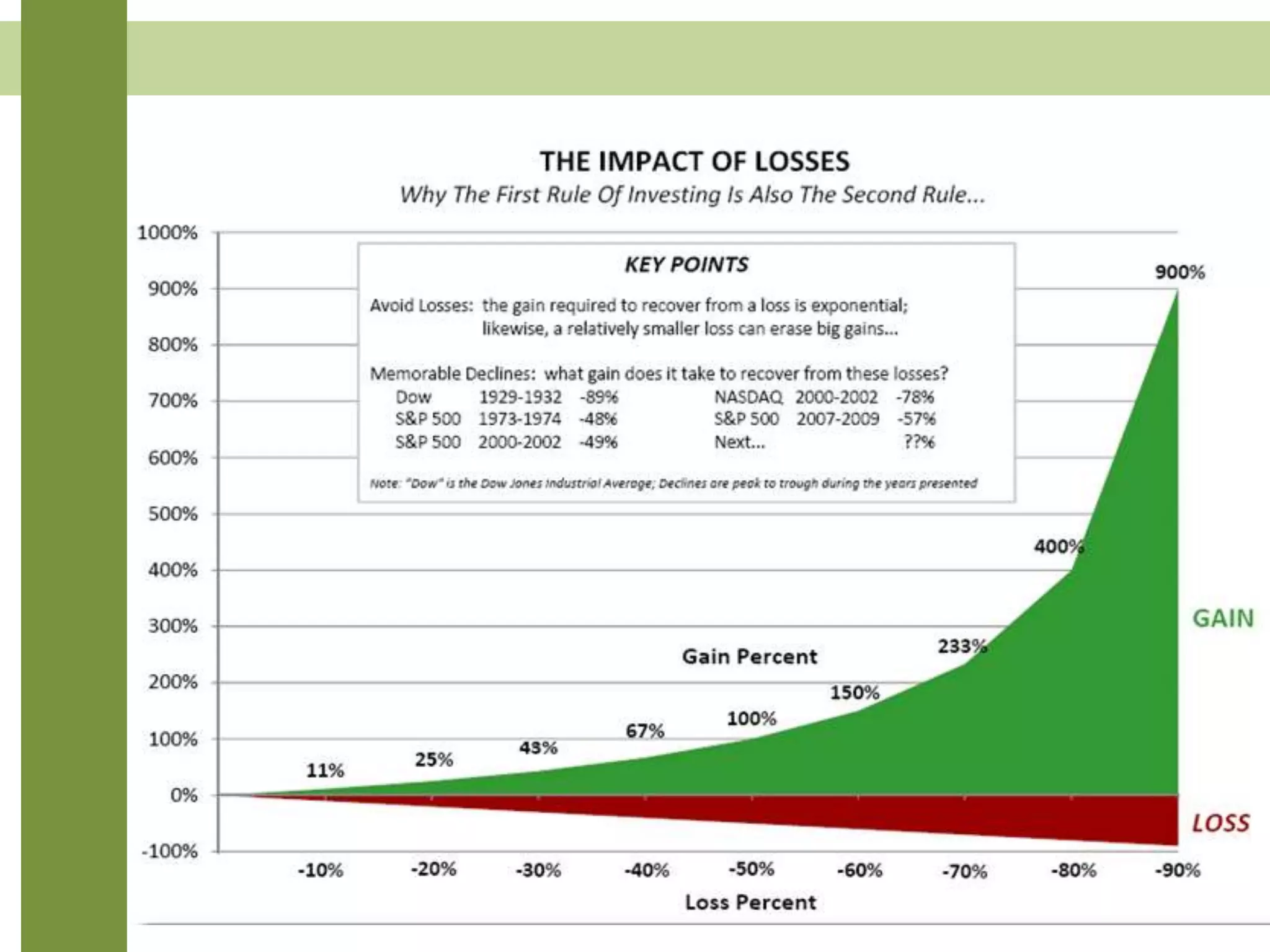

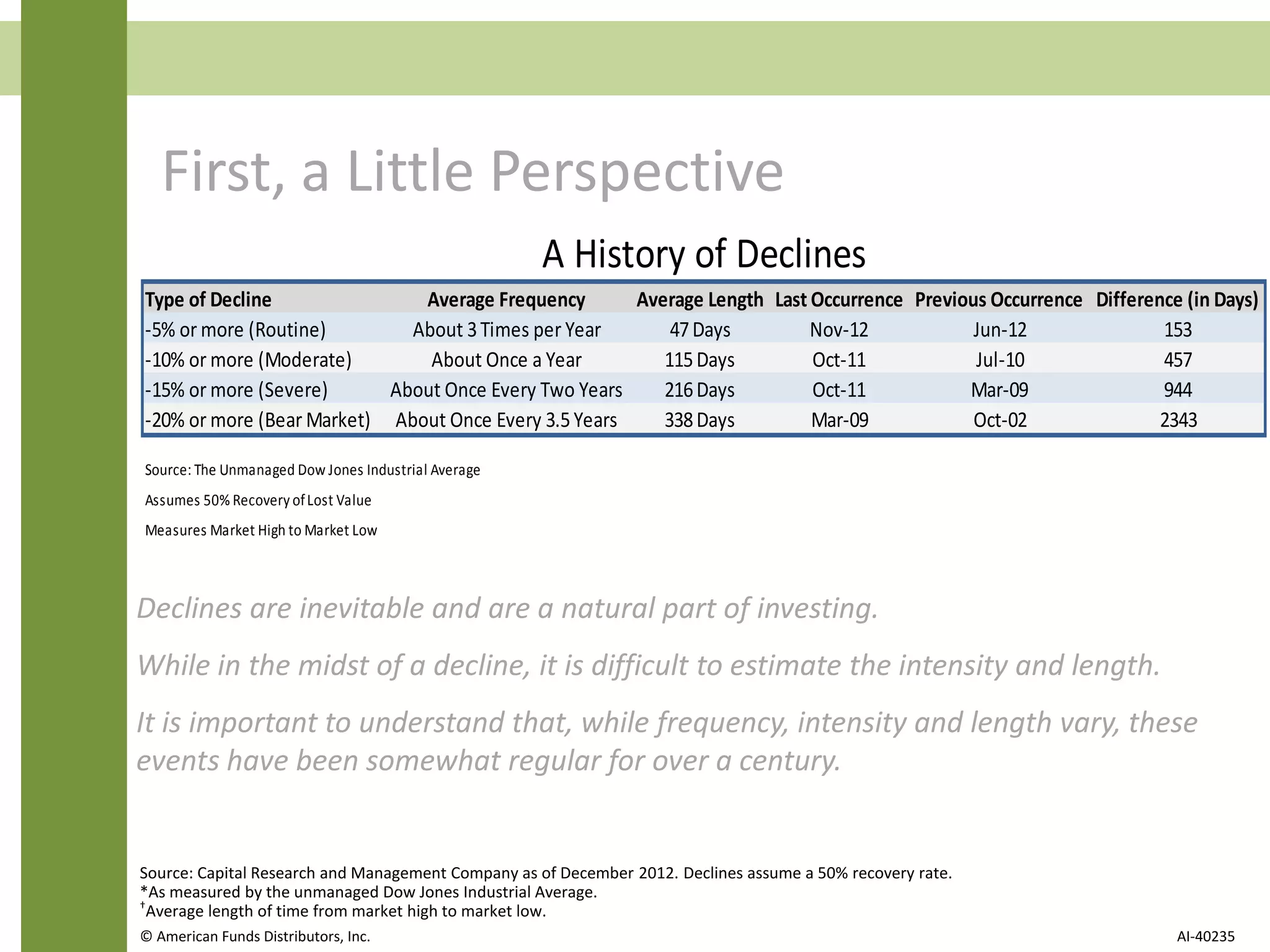

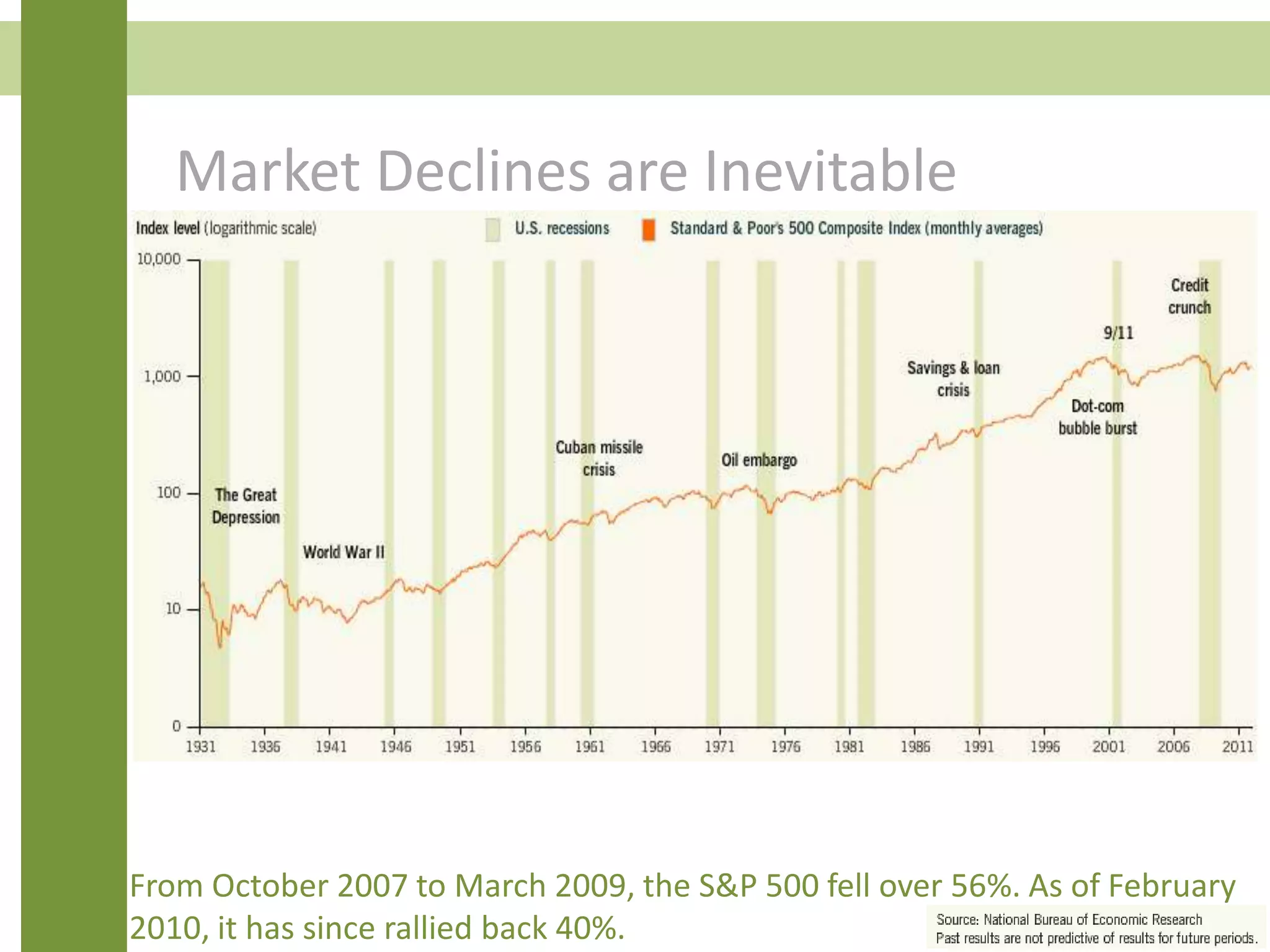

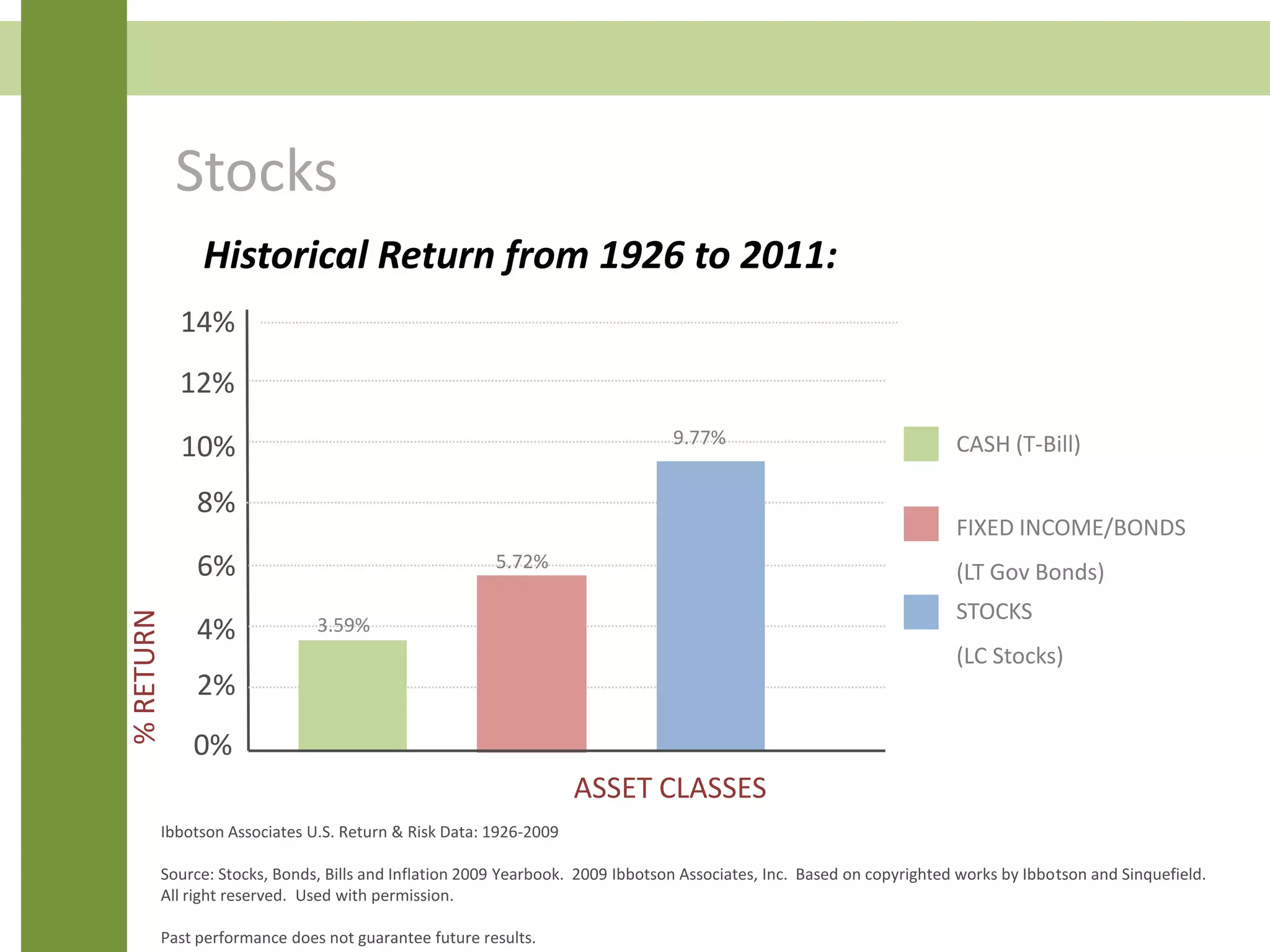

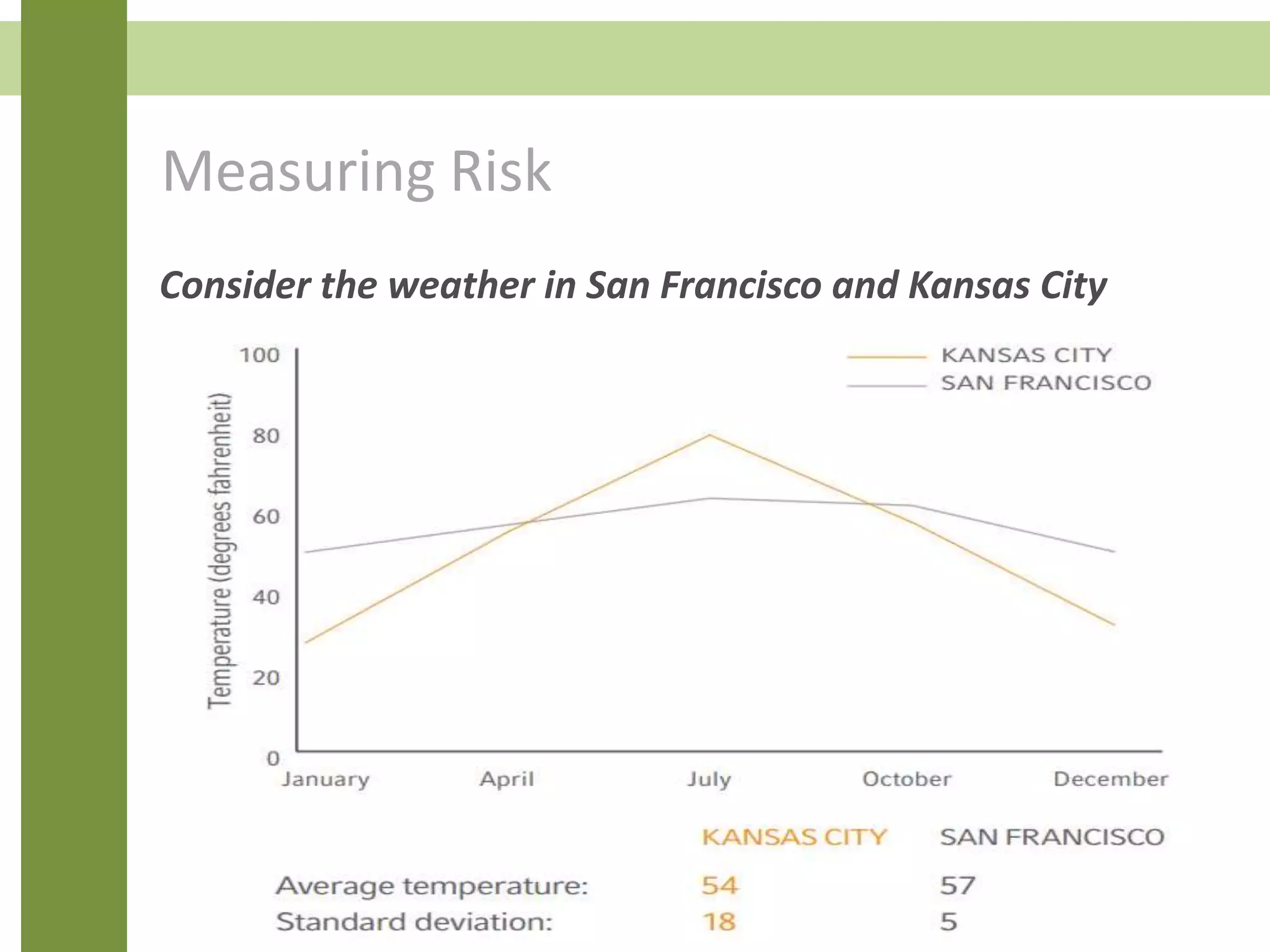

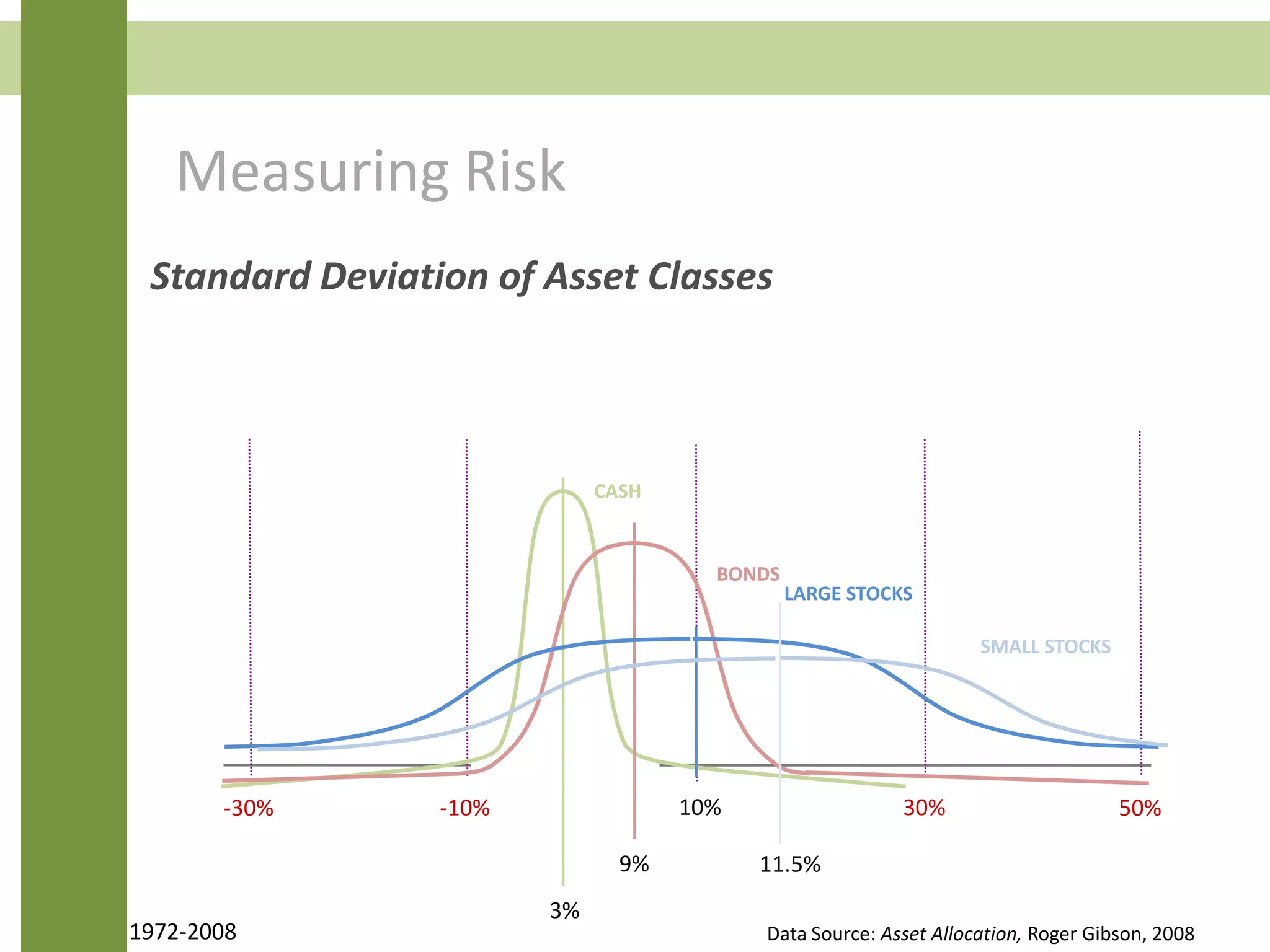

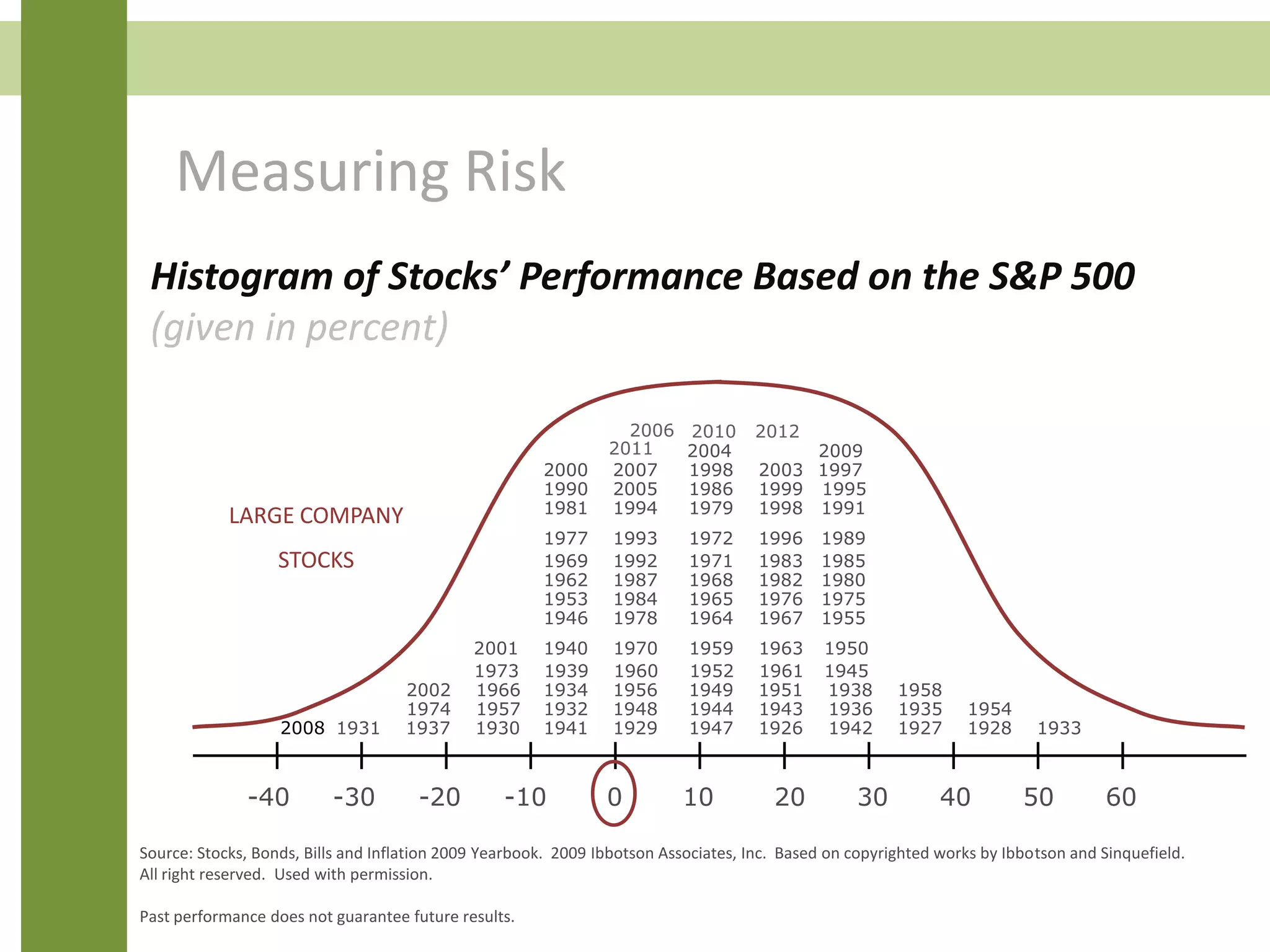

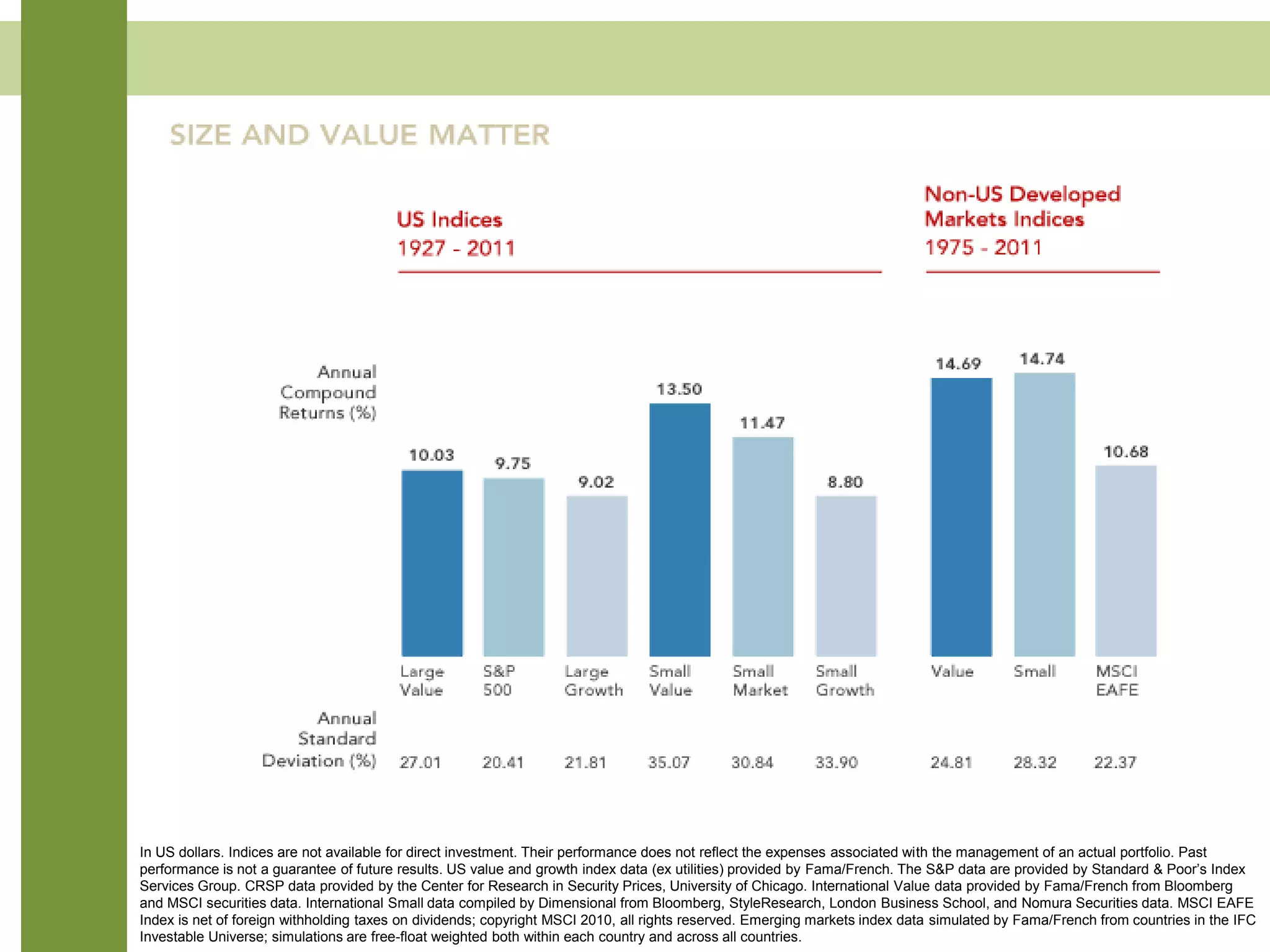

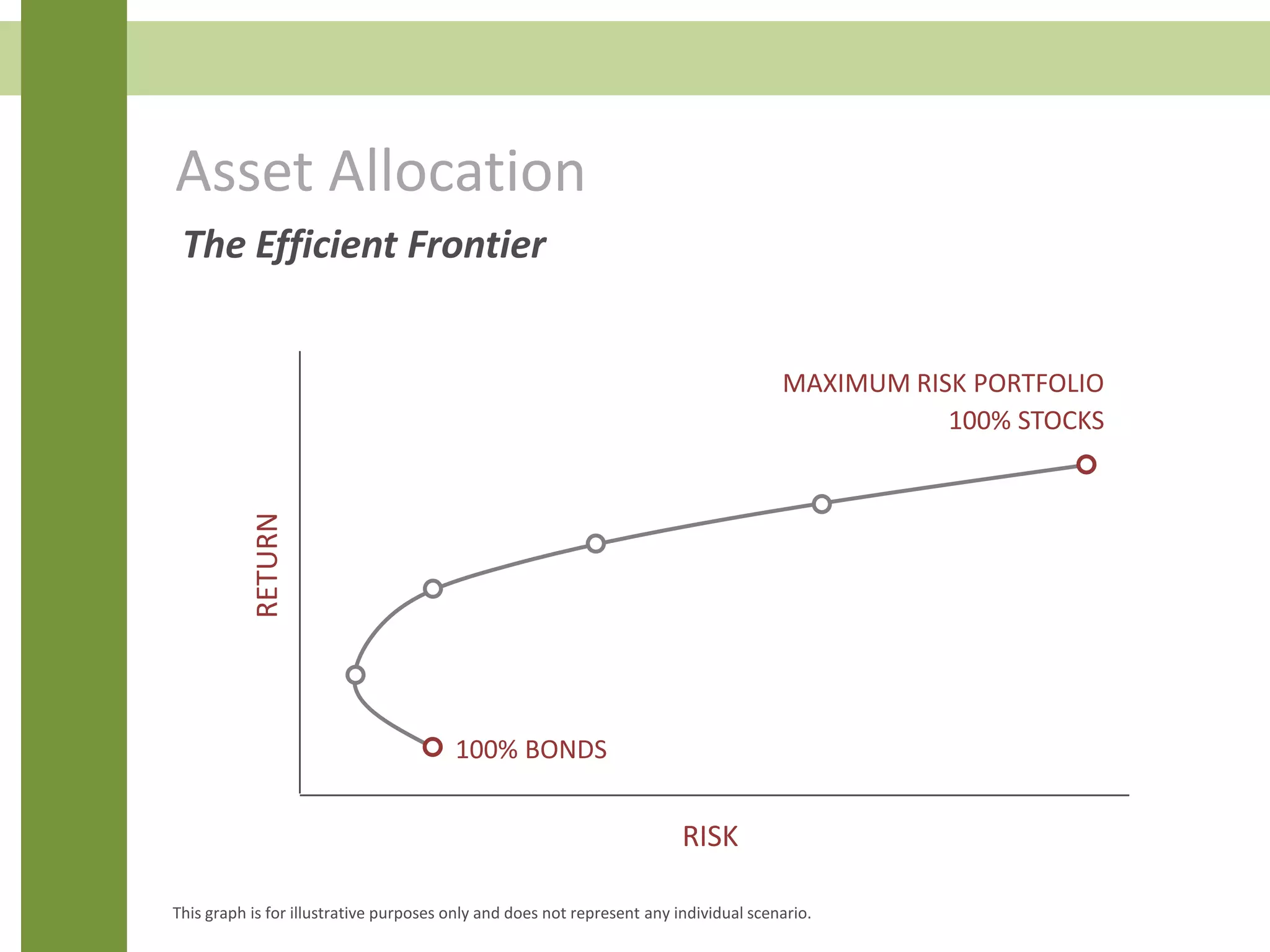

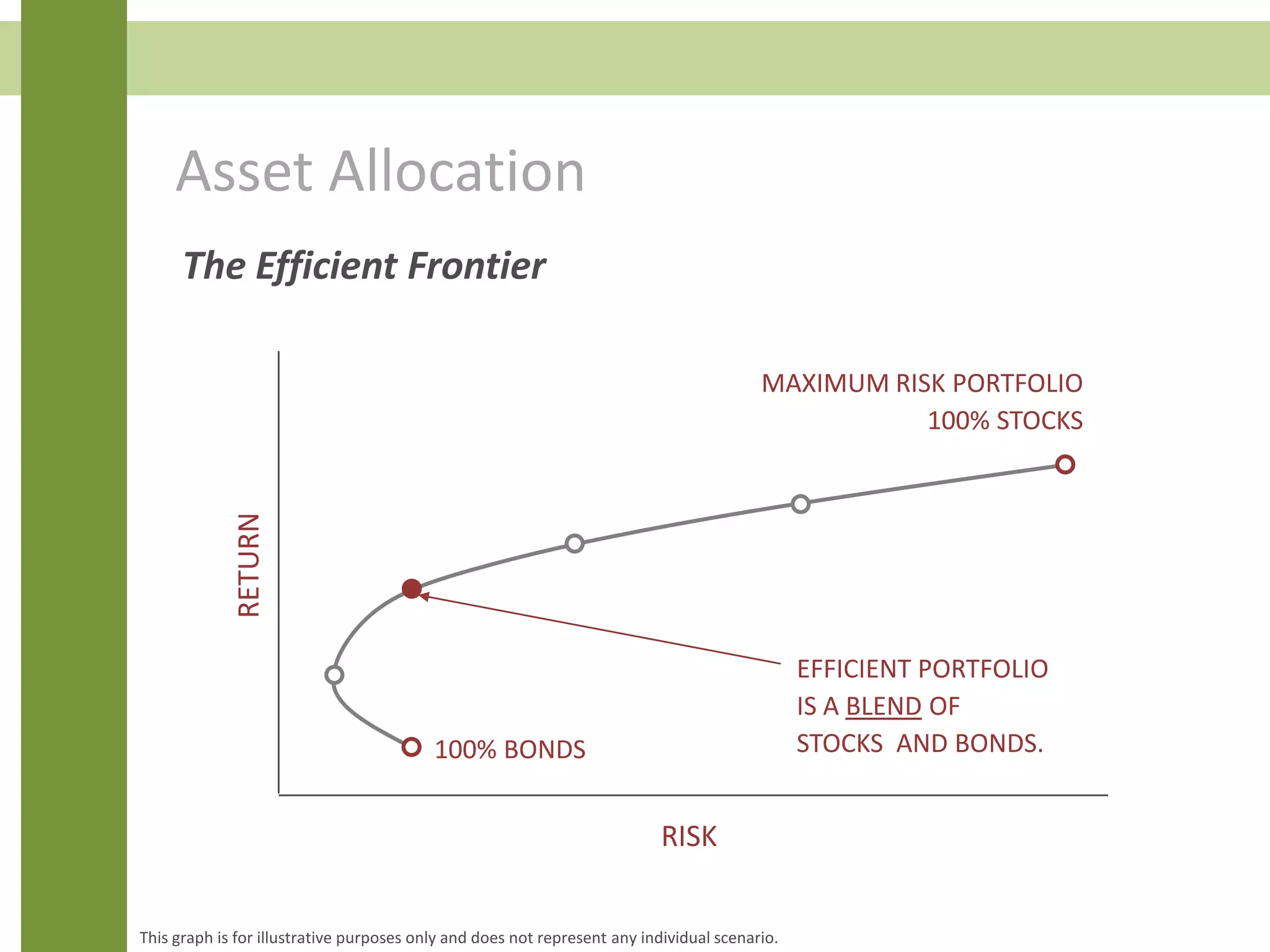

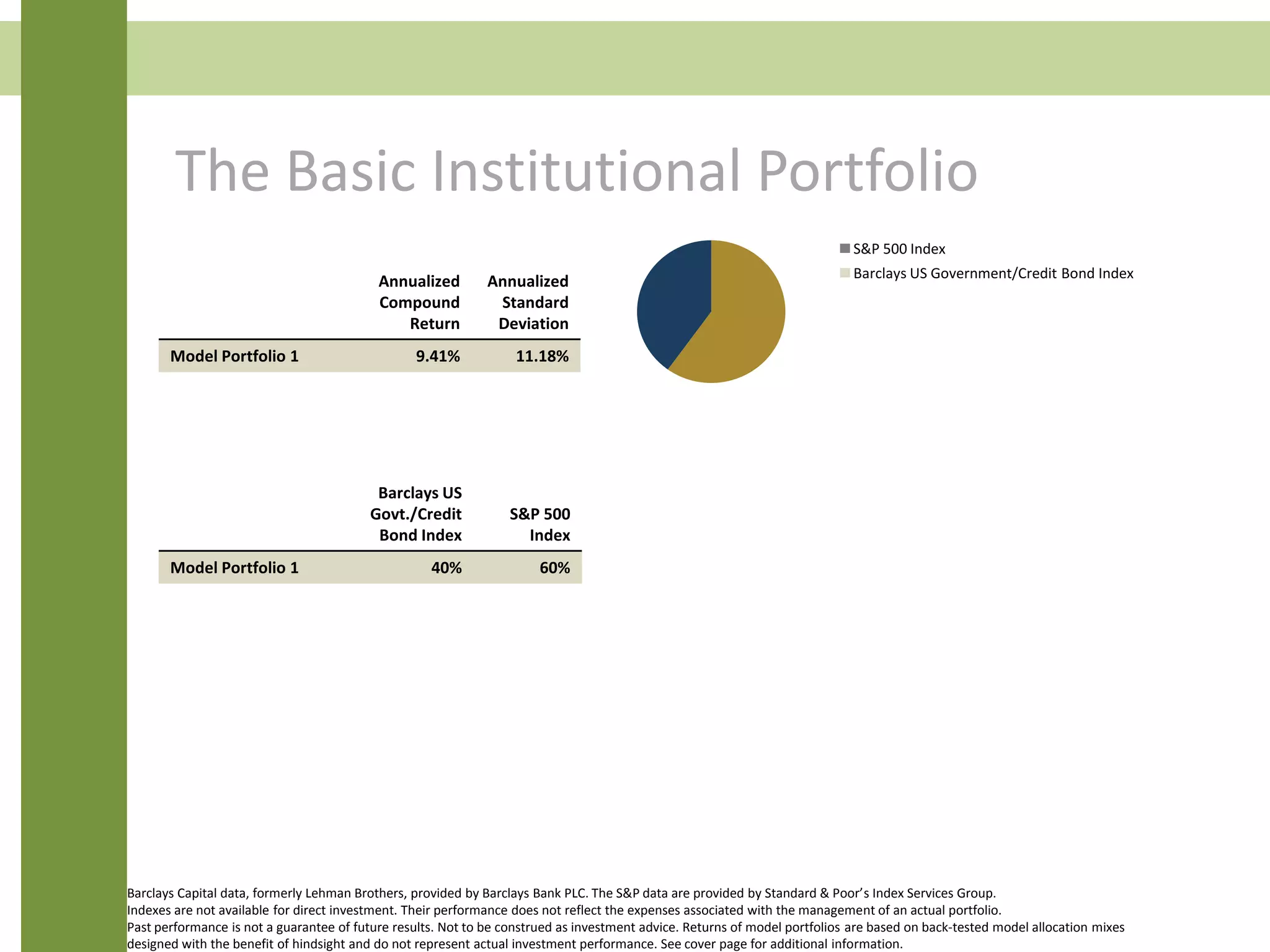

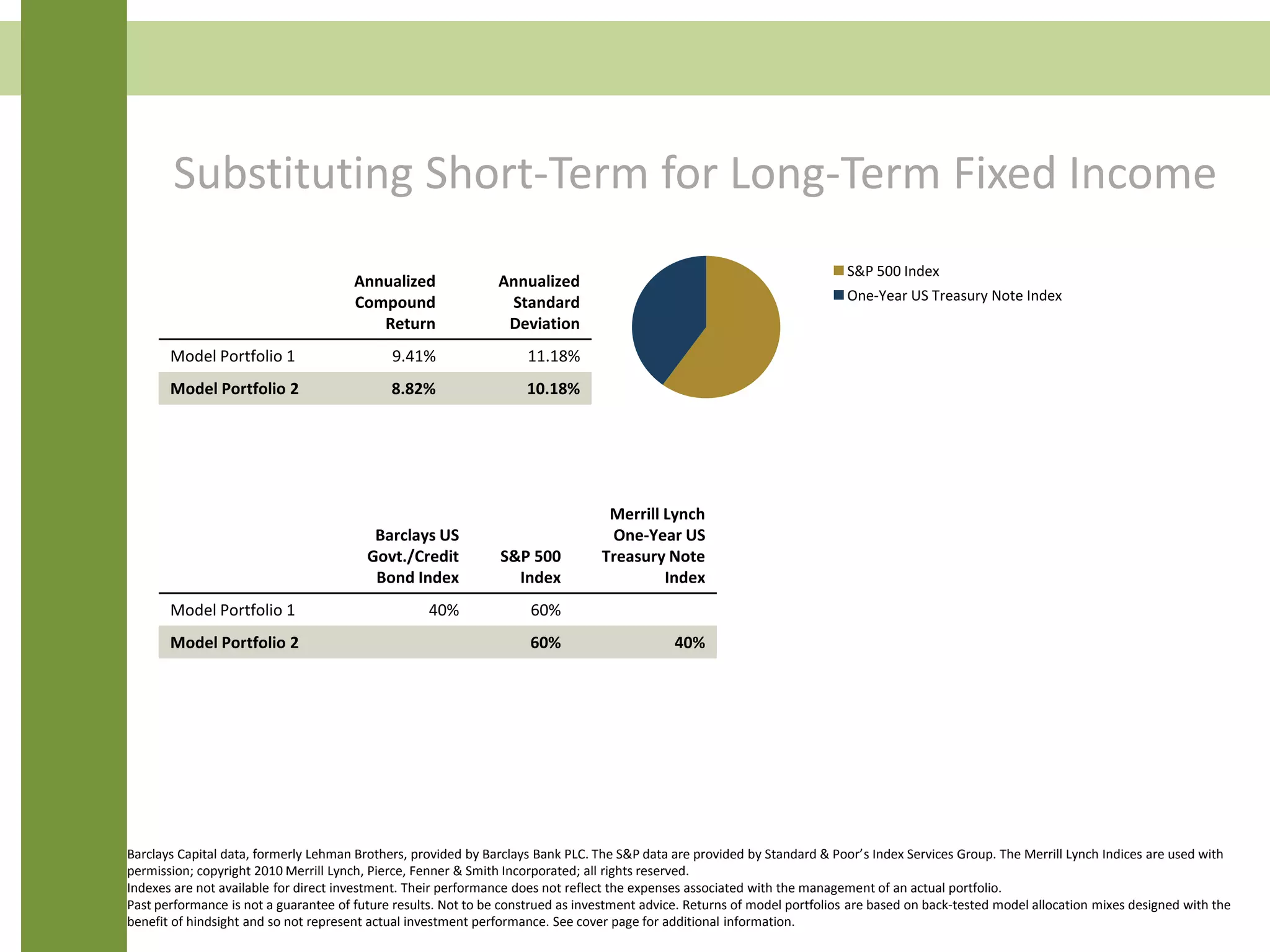

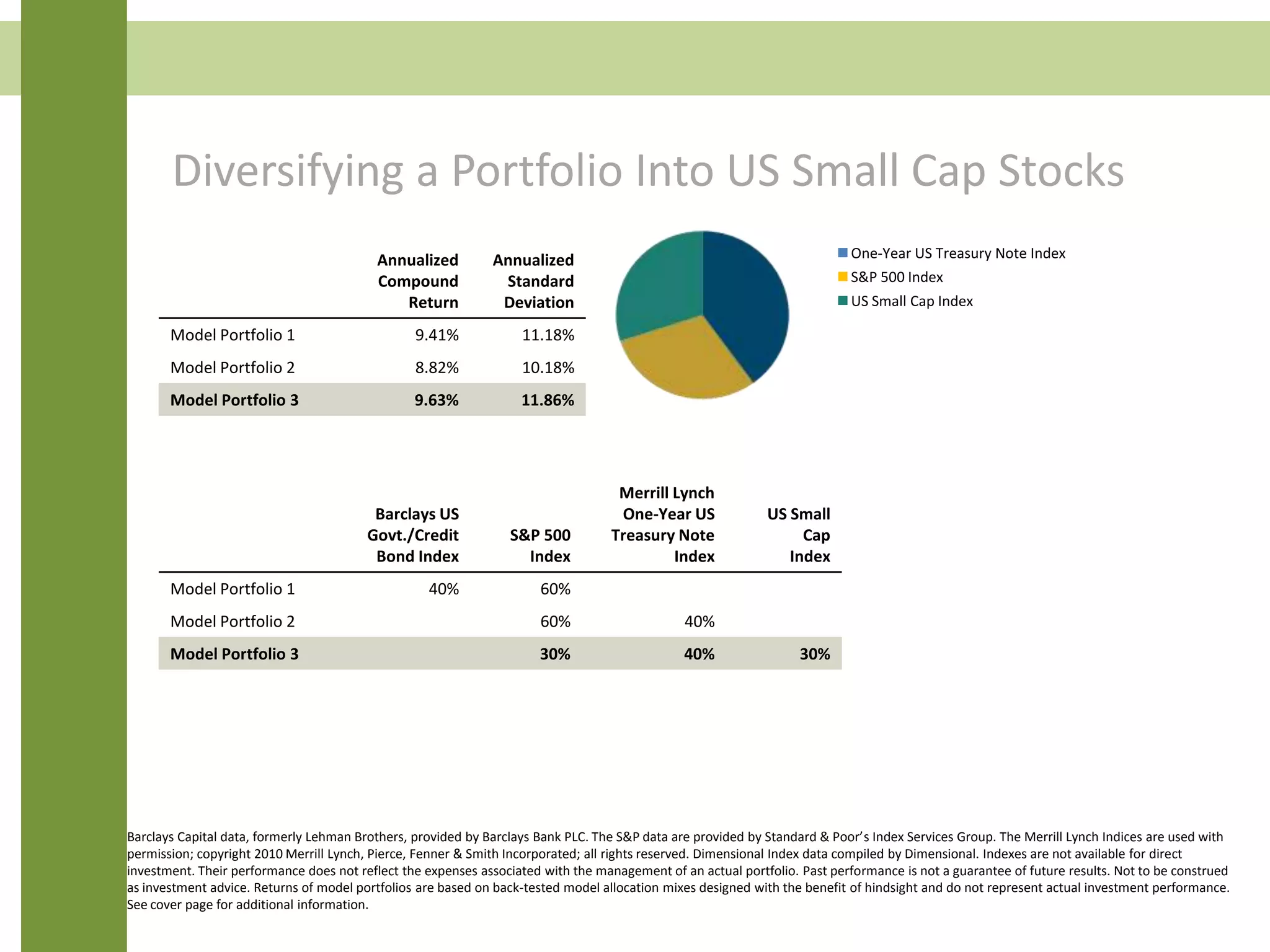

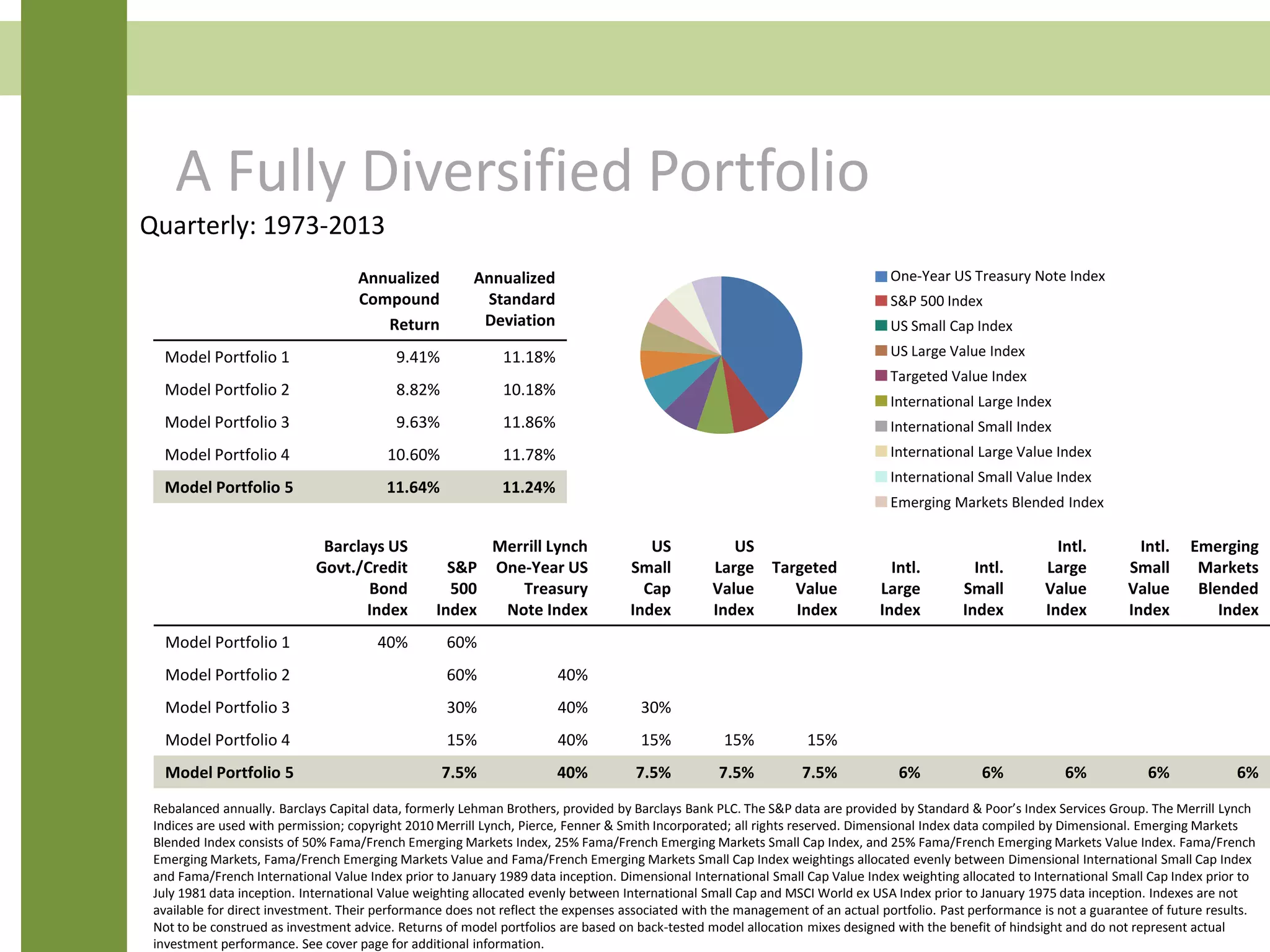

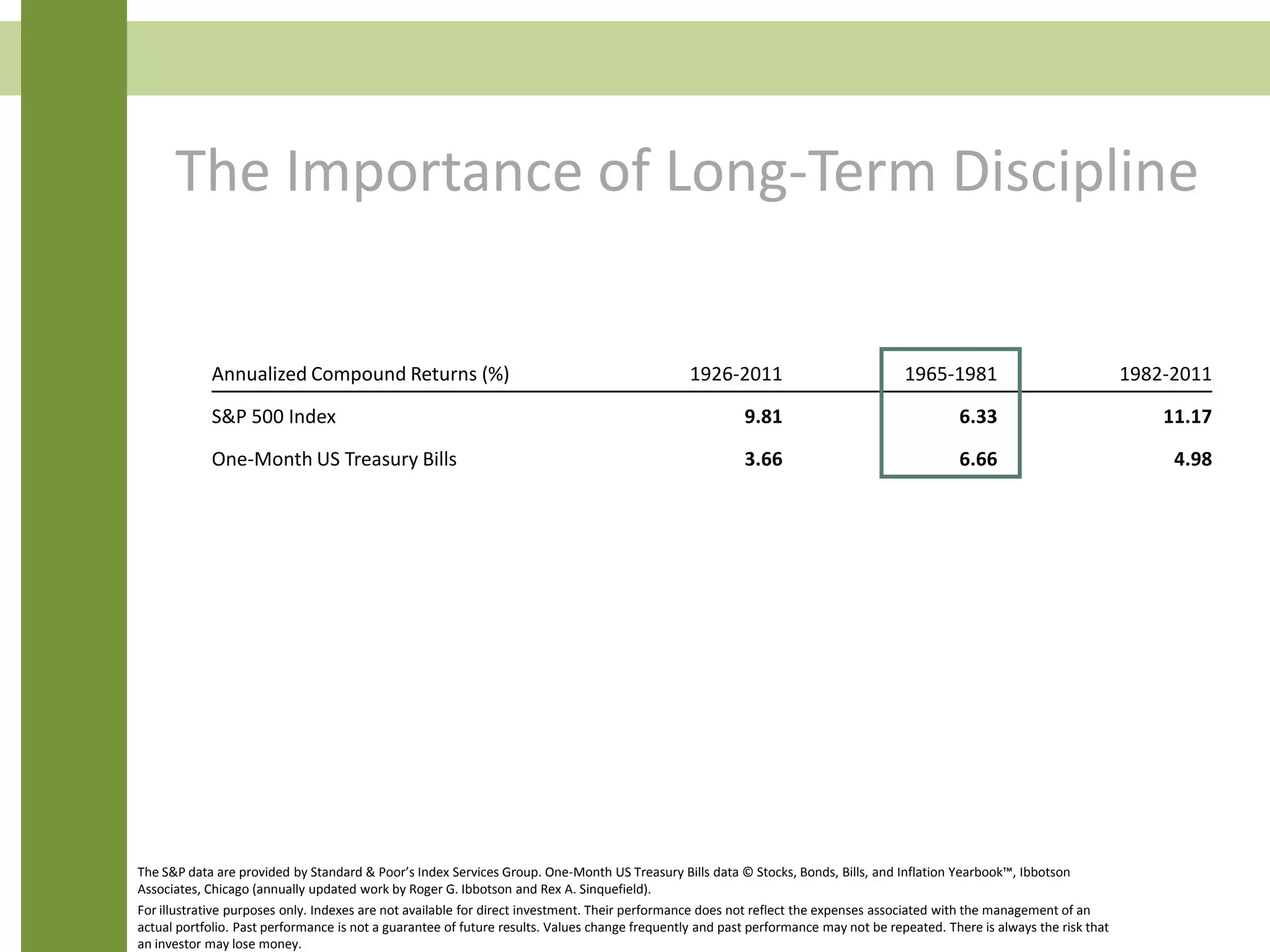

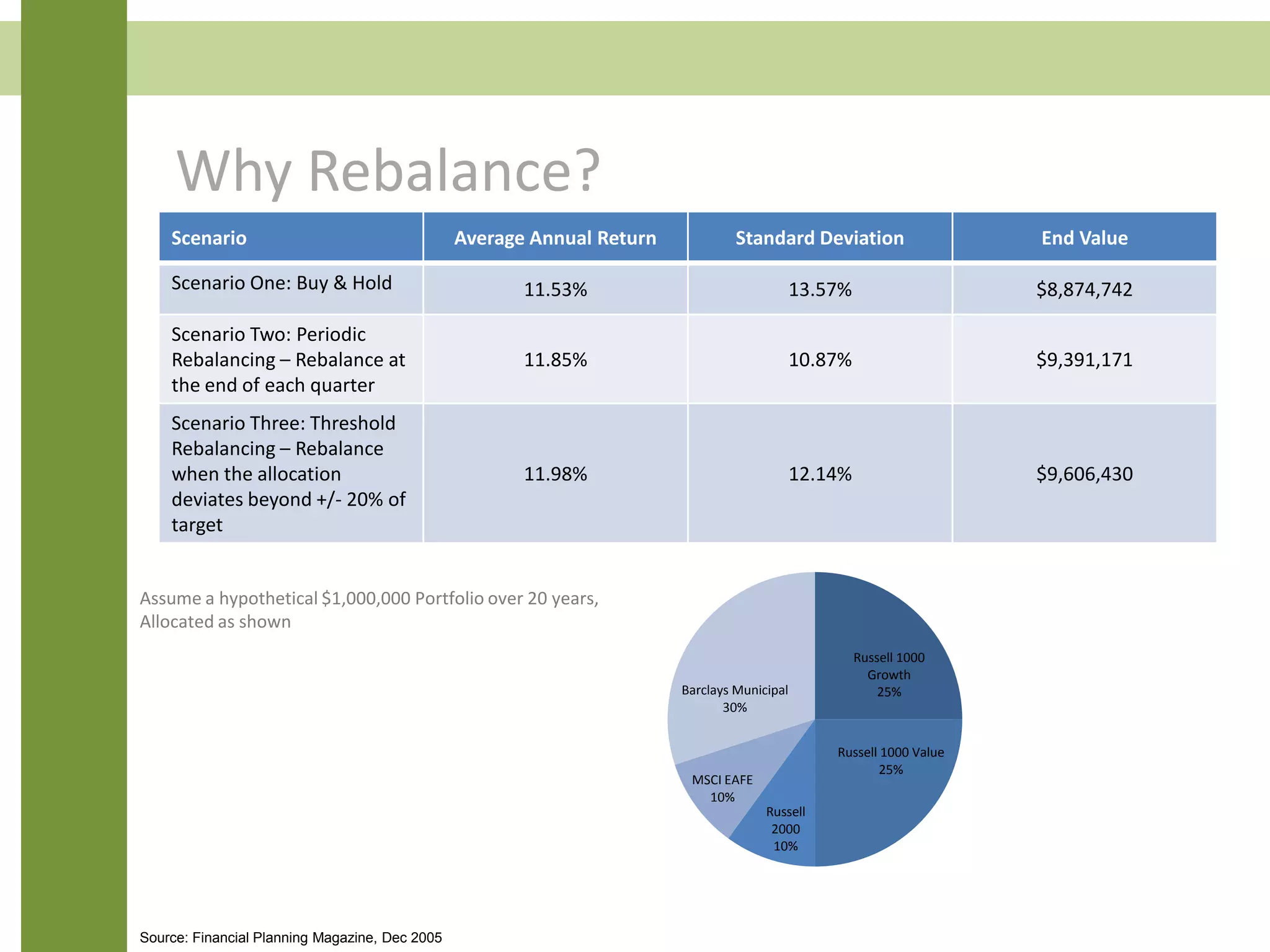

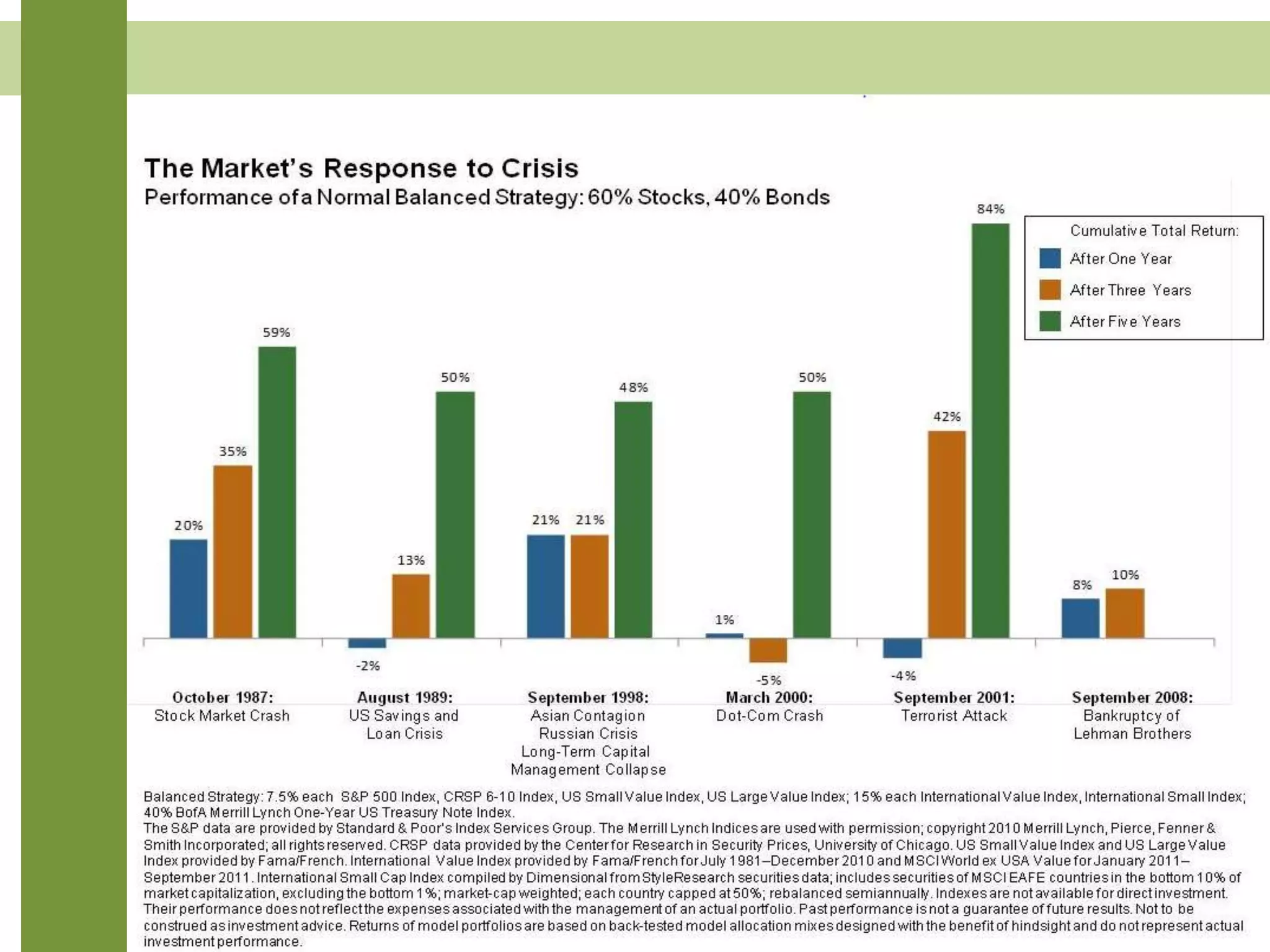

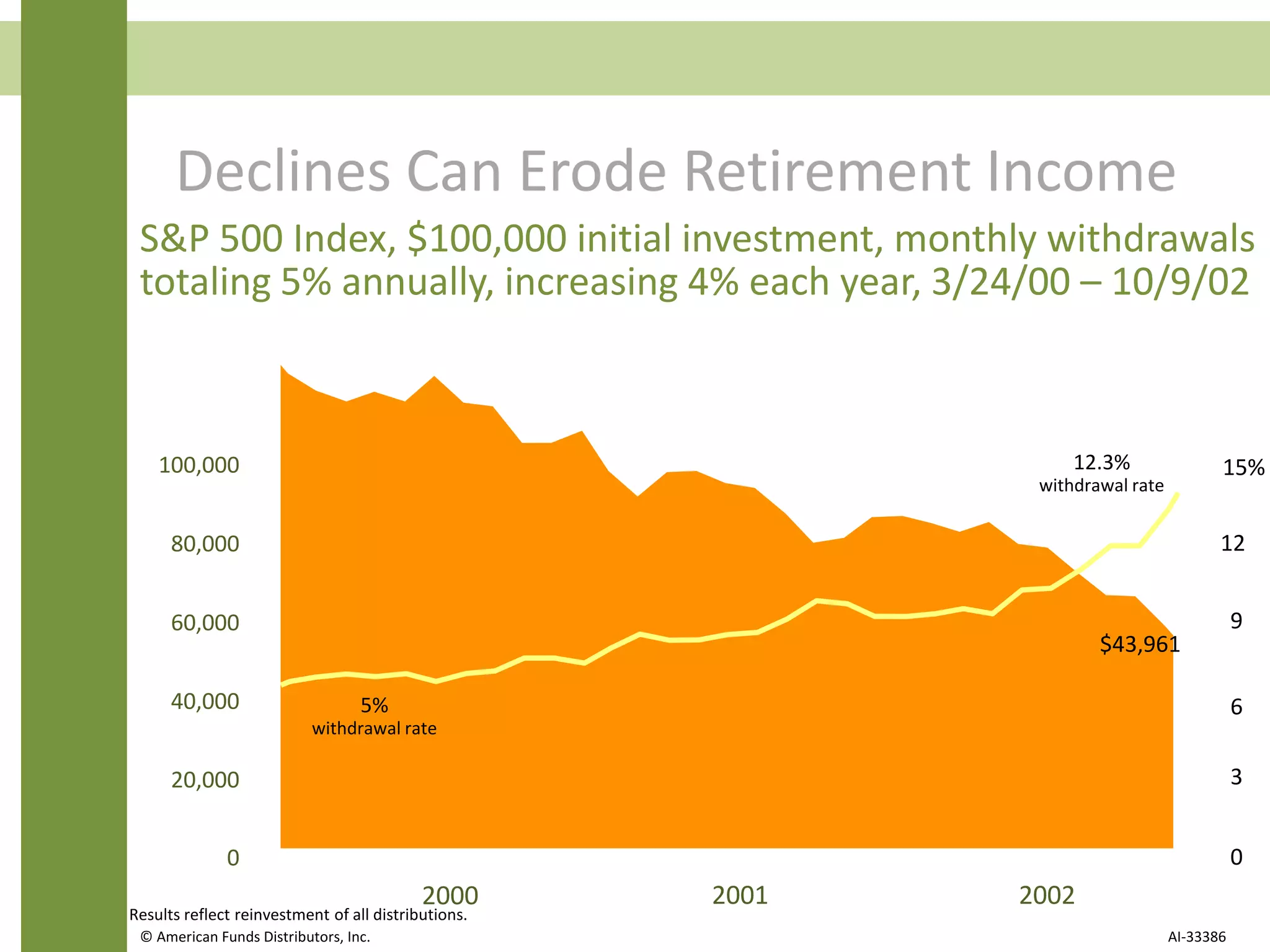

The document discusses wealth management principles and strategies for affluent investors, emphasizing the importance of understanding risk and expected return when investing for long-term goals, particularly during retirement. It highlights that while stocks generally outperform fixed-income securities over time, risk tolerance and time horizons change with age, necessitating tailored investment strategies. Various portfolios are illustrated to demonstrate how different asset allocations align with specific investment objectives and risk tolerances.