Downloaded 25 times

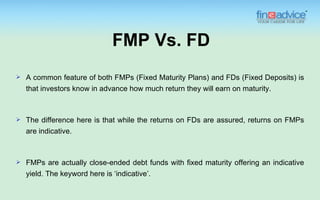

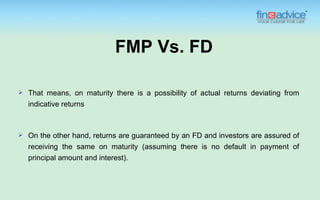

Fixed Maturity Plans (FMPs) and Fixed Deposits (FDs) both provide investors with an expected return at maturity, but while FDs offer guaranteed returns, FMPs have indicative yields that may vary. The difference in yields among FMPs is determined by the risk profile of the debt instruments within their portfolios, and tax implications also differ significantly, with FDs taxed as income and FMPs treated based on the investment option chosen. Ultimately, investors should assess their risk tolerance and investment goals to determine the most suitable option between FMPs and FDs.