Downloaded 77 times

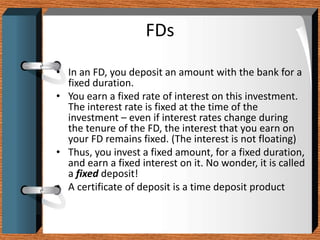

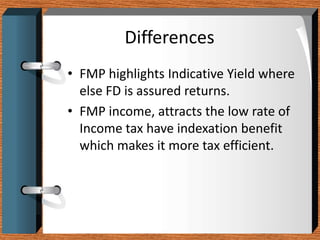

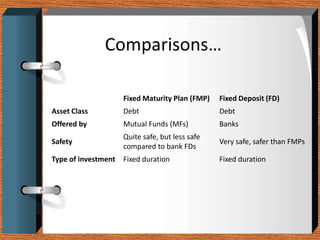

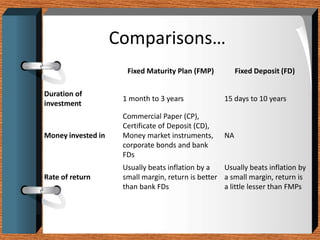

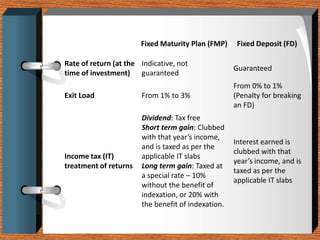

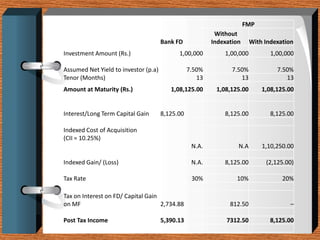

Fixed deposits allow investors to deposit a fixed amount for a fixed duration at a fixed interest rate. With fixed maturity plans, investors' money is invested in close-ended debt schemes with maturity periods ranging from 1 month to 5 years. Both carry credit risk but have predetermined returns. Key differences are that FMPs provide indicative not assured returns and the income is taxed at a lower rate with indexation benefits, making FMPs more tax efficient than fixed deposits.

![Investment ppt[1].pptx [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/investmentppt1-pptxautosaved-120507003432-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Session3 4-5-6 investment planning [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/session3-4-5-6investmentplanningautosaved-150317040013-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)