More Related Content

What's hot

What's hot (20)

Similar to Financial Technologies

Similar to Financial Technologies (20)

Recently uploaded

Recently uploaded (20)

Financial Technologies

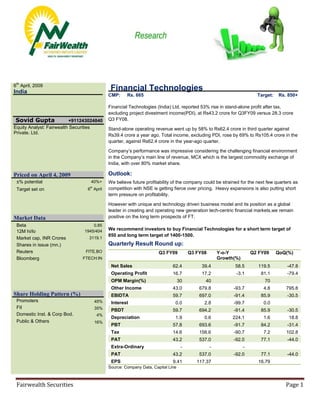

- 1. th 6 April, 2009 India Financial Technologies CMP: Rs. 665 Target: Rs. 850+ Financial Technologies (India) Ltd, reported 53% rise in stand-alone profit after tax, excluding project divestment income(PDI), at Rs43.2 crore for Q3FY09 versus 28.3 crore Sovid Gupta +911243024840 Q3 FY08. Equity Analyst: Fairwealth Securities Stand-alone operating revenue went up by 58% to Rs62.4 crore in third quarter against Private. Ltd. Rs39.4 crore a year ago. Total income, excluding PDI, rose by 69% to Rs105.4 crore in the quarter, against Rs62.4 crore in the year-ago quarter. Company’s performance was impressive considering the challenging financial environment in the Company’s main line of revenue, MCX which is the largest commodity exchange of India, with over 80% market share. Priced on April 4, 2009 Outlook: ±% potential 40%+ We believe future profitability of the company could be strained for the next few quarters as Target set on th 6 April competition with NSE is getting fierce over pricing. Heavy expansions is also putting short term pressure on profitability. However with unique and technology driven business model and its position as a global leader in creating and operating new generation tech-centric financial markets,we remain Market Data positive on the long term prospects of FT. Beta 0.85 12M hi/lo 1945/404 We recommend investors to buy Financial Technologies for a short term target of 850 and long term target of 1400-1500. Market cap, INR Crores 3119.1 Shares in issue (mn.) Quarterly Result Round up: Reuters FITE.BO Q3 FY09 Q3 FY08 Y-o-Y Q2 FY09 QoQ(%) Bloomberg FTECH:IN Growth(%) Net Sales 62.4 39.4 58.5 119.5 -47.8 Operating Profit 16.7 17.2 -3.1 81.1 -79.4 OPM Margin(%) 30 40 70 Other Income 43.0 679.8 -93.7 4.8 795.8 Share Holding Pattern (%) EBIDTA 59.7 697.0 -91.4 85.9 -30.5 Promoters 45% Interest 0.0 2.8 -99.7 0.0 FII 35% PBDT 59.7 694.2 -91.4 85.9 -30.5 Domestic Inst. & Corp Bod. 4% Depreciation 1.9 0.6 224.1 1.6 18.8 Public & Others 16% PBT 57.8 693.6 -91.7 84.2 -31.4 Tax 14.6 156.6 -90.7 7.2 102.8 PAT 43.2 537.0 -92.0 77.1 -44.0 Extra-Ordinary - - - PAT 43.2 537.0 -92.0 77.1 -44.0 EPS 9.41 117.37 16.79 Source: Company Data, Capital Line Fairwealth Securities Page 1

- 2. Buy-Financial Technologies Q3 Analysis Highlights: 58.5% Y-o-Y growth in Net sales. FTIL to set up multi-asset bourse in Bahrain-Jan-09 Non PDI income has grown to 105 crores BFX (Bahrain Financial Exchange) has been given approval to list and trade cash and versus 63 crores in the year ago quarter. derivatives instruments on multiple asset classes such as equities, currencies, commodities, debt products, Islamic Finance instruments and clearing by its brokers. Operating PAT on standalone basis stood at 43.2 crores versus 28 crores in Q3 FY08. Company’s Operating Profit margins have witnessed sharp drop as Expenses FTIL to acquire acquires 60% equity in Bourse Africa-Dec’08 have risen at faster pace. Botswana-based Bourse Africa Limited has been licensed by government of Botswana, to Expenditure set-up Spot and Derivative Multi-Asset exchange for trading in commodities, currencies, bonds and diamonds Q3FY0 Q3F % Change 9 Y08 Y-o-Y MCX-India’s leading commodity exchange launched currency derivatives -October Mat. Cost 5.5 1.9 193.3 2008. % of Sales 8.8 4.8 Emp. 21.5 11.7 83.4 Company Description: Expenses The Financial Technologies group is among the global leaders in offering technology IP % of Sales 34.4 29.8 (Intellectual Property) and domain expertise to create and trade on next-generation financial S&A Exp. 6.8 1.1 539.4 markets. % of Sales 10.9 2.7 The Financial Technologies group operates one of the world’s largest network of 10 exchanges connecting fast-growing economies of Africa, Middle East, India and South East Other Exp. 12.0 7.4 61.2 Asia. The group also has six ecosystem ventures to address upstream and downstream % of Sales 19.2 18.9 opportunities around exchanges, including clearing, depository, information vending, and Source: Capital Line payment gateway among others. Rising Expenses are putting pressures Company is the only corporate house to have set up 5 international exchange namely : on the bottom line and EBITDA margins. Dubai: Dubai Gold and Commodity Exchange(DGCX) Increased Employee and Sales Expenses is also seen as preperation for Singapore(Sinfapore Mercentile Exchange(SMX) Future Growth. Bahrain: Bahrain Commodity Exchnage Mauritius: GBOT (Global Board f Trade) Botswana: South Africa Bourse Company has 3 focussed line of business. Exchange business Ecosystem Businesss Technology Business While Exchange business is the company’s focussed line of business, Ecosystem and Technology are the supporting businesses which form upstream and downstream opportunities and support. Fairwealth Securities Page 2

- 3. Buy-Financial Technologies Group Companies: MULTI COMMODITIES EXCHANGE OF INDIA: Largest Commodity exchange in India with: 89% market share in Q3 as against 82% in the corresponding quarter. Average daily turnover of 13,900 crore for April-Dec 2008. Latest tradeable product to be launched was Electricity in Jan 2009 Financial Technologies is the main promoters of Financial Technologies with 37% share holding. Other main promoters of MCX are SBI, Fidlity and Citigroup (Source: Draft Red Herring Prospectus). At the time deal valued MCX-SX at around USD 1 billion. MCX-SX Started currency futures trading in October 2008. Within 2 months of Operation acquires over 50% market share. DGCX(Dubai Gold and Commodity Exchange) DGCX commenced trading in November 2005 as the regions first commodity derivatives exchange and has become today, Middle East's largest and most diverse commodities and derivatives exchange. DGCX is an initiative of the Dubai Multi Commodities Centre (DMCC), Financial Technologies (India) Limited and the Multi Commodity Exchange of India Limited (MCX) Total of 2.6 million + contracts traded with a value of USD 107 billion+ since inception. FT group holds 39% shareholding while MCX holds 5% shareholding in the company. IEX: India’s No.1 power exchange with a market share of 96%, 55 members and a turnover of 1337 crores. NSEL National Spot exchange Limited, established in October’08 with an aim to reach a daily turnover of 15000 crores by 2011. Currently traded commodities are Bullion and Agri Commodities NHBC: National Bulk handling Corporation is highly ambitious project of FTIL with a purpose to establish Warehouses (418 ware houses with 1.64 mn.MT of storage Capacity and 9.2 mn. Sq. Ft. of storage area.) Company also provide Collateral Management Services to over 3500 storage facilities and handles over 6mn MT of Commodities and perform Quality Assurance and Pest Management. Fairwealth Securities Page 3

- 4. Buy-Financial Technologies Atom Atom is the product from the technology arm providing Mobile payments servces 5 fold growth in payment processing from 30 crores in March’08 Quarter to over 160 crores in Dec’08 Quarter. Tickerplant Ticker plant is in the business of information retailing by providing data, news, analytics for Capital Markets. It provides feeds, entire data, Fundamental and Technical Charting for Forex, Equities and Commodities markets from vatious Exchanges. Competition: NSE is leading exchange in India, since its inception in 1994. It is the largest Equities and FNO exchange in the country with BSE a distant second. Exchange also has its presence in Commodities, Foreign Exchange and Power Trading. MCX which is late entrant has with its strong technical and support infrastructure has lately started giving tough competition to NSE. NSE, which enjoyed a virtual monopoly in the stock market, had a taste of real competition when FT launched MCX-SX, a stock exchange, and started currency derivatives trading in October last year. It’s been a see-saw fight ever since, with daily trading volume data for February showing MCX-SX’s market share at 50.23 per cent to NSE’s 49.77 per cent. MCX –SX hasn’t started operations in Cash and Futures segment of Equities as it is awaiting regulatory approvals. NSE has started a price war by offering its software NOW free of cost for three years. 80% of the brokers are already using FT’s ODIN. What many analysts believe is predatory pricing, NSE has clarified that it does this is inline with its policy. FT received biggest hit when NSE decided to put FT’s ODIN on watch list on software defeciency ssues and rejected FT’s application to issue new licenses. FT took NSE to court for taking such step and now both parties are presenting their case in the court. There is another majore issue in the currency futures market, NSE has kept zero transaction fee a practise which has been criticised by MCX-SX as well as industry experts. NSE can afford to keep zero transaction fees as it earns most of its revenue in the cash and futures segment of Equities. Industry experts have called fr a level playing field asking regulators to allow more brokerage houses in the Equities and Derivatives segment. Fairwealth Securities Page 4

- 5. Buy-Financial Technologies THE BATTLEFIELD Who operates what NSE FT/MCX Technology Now, NSEIT, OM NSESYS ODIN Stock exchange Equity, F&O and currency Currency Commodity futures NCDEX MCX Power trading PXI IEX Overseas exchange 5 exchanges Source: Business Standard While there is much more to the battle between two large exchange in India, Industry has clearly suggested its need for more transparent and competitive exchanges, moreover considering demand and need to develop Indian Financial markets Indian markets can clearly accommodate more exchanges. Valuations: We initaiate a buy call on Financial Technologies after analysing and accounting for major upsides and downsides for the stock. Company is poised to give astounding results in years to come and we expect them to deliver 40% CAGR in its topline over next 4 years. Profitability can get get strained in FY 10E if the they enter into a price war with NSE. Company’s amazing track record and its technical and operational capabilities and unlimited opportunities in Financial Markets industry in the developong and under developed countries. We remain positive in the long term and advise investors to invest for longer periods to of time. At its current price of 635 stock is fairly valued for high growth company. Company’s total Income has increased to 484 crores for 9M FY’09 while Net Profits have risen to Rs. 290 crores giving EPS of 63.21 for 9M FY’09. At annualised EPS of around 84 for stock is trading at 7.5 x times its expected FY’09 earnings. Company has app. 1200 crores of cash and liquid securities on its balance sheet. Copany has been registering growth of over 100%over last 5 year. We expert stock to touch 850 – 900 in 4-6 months and to go even higher to touch its lifetime highs for investors who can hold the stock for a period of two years. Fairwealth Securities Page 5

- 6. Buy-Financial Technologies Buy Key Risks: 1. With current price war between NSE- MCX-SX and NSE- -MCX, FT might be forced to lower the fees for its product which can have a huge negative impact on its profitability. 2. Financial Technologies can face major downside if it receives unfavorable response over its ongoing litigation with NSE, which stops it to issue further licences to brokers for , its ODIN product. 3. Any major policy changes which stops FT’s exhanges to expand in Indian markets. 4. Policy changes in spot and futures of major Commodities can also have negative impact pot on Financial Technologies. 5. General slowdown in Bullion, Forex and Commodity markets can also lead to lower than expected growth. Besides first point we do not see any major risk and other risk mentioned are unlikely to materialize. However price war between MCX and NSE is likely which could lead to lower profitability in the coming quarters. Financial Technology stock has witnessed more than 70% drop in share value from Feb’08 to Feb’09 while Nifty fell by only 40%. Last 1 month of continuous buying has led to a huge spurt in Financial Technology share prise which has risen by more than 50%. We believe that a lot of steam is left in the stock and with latest announcements of Bourse Africa and Bahrain Stock exchange FT stock price will see further triggers in the share price. ther Source: Capital Line Fairwealth Securities Page 6

- 7. Buy-Financial Technologies Investment Rational Dominance in commodities(85% market share), Power(90% market share ) and Forex markets with MCX and MCX –SX, FT has huge growth potential as India’s Financial markets are only in nascent stage With over 10 exchanges and supplementary businesses like Ecosystem and IT services FT has established expertise in developin and operating exchanges. With major presence in India and Dubai, FT is exapanding its presence fast other emerging economies like Bahrain and Africa(Bourse Africa). We see tremendous growth in financial markets of these economies and FT is well poised to take advantage of the boom. MCX-SX, which already has more than 50% market share in Currency Futures market has applied to launch cash and futures for Equity markets. When it gets permission for the same. Given FT’s track record MCX-SX is likely to give huge competition to NSE and BSE in their biggest revenue contributor. As a final word, FT’s current cash flow and growth figures do not justify its huge valuation, but key to FT’s valuation is Its strong technical capabilities and proven operational track record Strong growth being wiitnessed and huge growth potential of Indian Financial markets Need for other Financial markets to develop and establish Exchange traded products and supporting infrastructure to develop spot market in tandem. TECHNICAL OUTLOOK FINANTECH FINANTECH has given a break out above 540 levels and had a good rally above that to post a high of 702.A look at the RSI shows that the stock is trading in a highly overbought zone .So one can buy the stocks on dips at around 550-600 levels for an upside Target of 850 in 2-3 months. Fairwealth Securities Page 7

- 8. Buy-Financial Technologies Annexure: 1. Income Statement: Income Statement Fund Flow Statement: 200803 200703 200603 2008(12) 2007(12) 2006 (12) SOURCES OF FUNDS : Share Capital 9.18 8.82 8.8 INCOME Reserves Total 1492.05 304.49 299.88 Net Sales 266.9 264.5 182.0 Total Shareholders Funds 1501.23 313.31 308.68 Other Income 1177.5 62.2 19.3 Minority Interest 11.79 108.92 110.9 Total Income 1444.5 326.7 201.2 Secured Loans 24.83 0 0 EXPENDITURE : Unsecured Loans 399.45 434.42 0 Raw Materials 3.0 7.9 0.0 Total Debt 424.28 434.42 0 Employee Cost 94.5 58.8 22.2 Total Liabilities 1937.3 856.65 419.58 Selling and Admin. APPLICATION OF FUNDS : Expenses 29.3 62.9 38.6 Net Block 50.38 98.85 34.2 Other Expenses 115.8 27.3 16.0 Capital Work in Progress 170.88 88.35 2.02 Total Expenditure 242.6 161.7 79.0 Investments 1184.16 438.66 630.99 Operating Profit 1201.9 165.0 122.2 Current Assets, Loans & Advances Interest 12.3 0.9 0.1 Inventories 59.15 1.76 0 Gross Profit 1189.6 164.1 122.1 Sundry Debtors 39.03 26.93 16.13 Depreciation 9.8 8.9 5.6 Cash and Bank 554.34 656.3 105.24 Profit Before Tax 1179.8 155.3 116.5 Loans and Advances 68.32 35.89 25.89 Tax 294.0 50.2 31.6 Total Current Assets 720.84 720.88 147.26 Net Profit 885.8 103.6 83.9 Less : Current Liabilities EO Items & Min. and Provisions Interest 16.3 37.2 31.5 Adj Net profit Current Liabilities 123.13 456.9 361.16 869.5 66.3 52.4 Provisions 69.77 30.55 31.4 EPS after Min. Int 185.57 13.04 14.86 Total Current Liabilities 192.9 487.45 392.56 Book Value 327.07 71.05 70.15 Source: Company Report, Capital Line Net Current Assets 527.94 233.43 -245.3 Net Deferred Tax 3.94 -2.64 -2.33 Total Assets 1937.3 856.65 419.58 Contingent Liabilities 8.57 4.38 2.7 Source: Company Report, Capital Line 2. Cash Flow Statement: 200803 200703 200603 . Cash Flow Summary Cash and Cash Equivalents at Beginning of the year 534.63 73.42 16.36 Net Cash from Operating Activities -296.21 125.89 312.22 Net Cash Used in Investing Activities -230.53 -23.2 -470.21 Net Cash Used in Financing Activities 346.5 358.52 215.05 Net Inc/(Dec) in Cash and Cash Equivalent -180.24 461.21 57.06 Cash and Cash Equivalents at End of the year 354.39 534.63 73.42 Source: Company Report, Capital Line Fairwealth Securities Page 8

- 9. Buy-Financial Technologies Coverage: Our Stock coverage and Returns. Stock Target Price as on Call date Price on % return absolute % return 2nd Relative April (Outperfe romance) Set Date Price Stock Sensex Stock Stock Sensex Educomp 22-Jan-09 2750 1715 8814 2398 39.8% 19.5% 20.3% Havells 30-Jan-09 280 115 8325 153.1 33.1% 26.5% 6.6% Jaiprakash 12-Feb-09 110 73 9466 97.55 33.6% 11.3% 22.3% Associates Lupin 3-Feb-09 780 630 8607 640 1.6% 22.4% -20.8% Tata Steel 6-Mar-09 250 152 8325 235.65 55.0% 26.5% 28.5% M&M 12-Mar-09 430 345 8344 459.7 33.2% 26.2% 7.0% Unitech 25-Mar-09 51 34 9667 36.75 8.1% 9.0% -0.9% Punj Lloyd 30-Mar-09 120/145 85 9549 106.7 25.5% 10.3% 15.2% Note: Based on 6th April Sensex closing of 10535 Note: All calls are initial/ first time calls Note: All reports can be accesed Fundamental and Technical reports are independently given and investors are advised to take their decision based on their investment profile and holding periods Disclaimer This publication has been prepared solely for information purpose and does not constitute a solicitation to any person to buy or sell a security. While the information contained therein has been obtained from sources believed to be reliable; investors are advised to satisfy themselves before making any investments. Fairwealth Securities Pvt Ltd does not bear any responsibility for the authentication of the information contained in the reports and consequently, is not liable for any decisions taken based on the same. Further, Fairwealth Research Reports only provide information updates and analysis. All opinion for buying and selling are available to investors when they are registered clients of Fairwealth Investment Advisory Services. As a matter of practice, Fairwealth refrains from publishing any individual names with its reports. As per SEBI requirements it is stated that, Fairwealth Sec Pvt Ltd., and/or individuals thereof may have positions in securities referred herein and may make purchases or sale while this report is in circulation. Fairwealth Securities Page 9