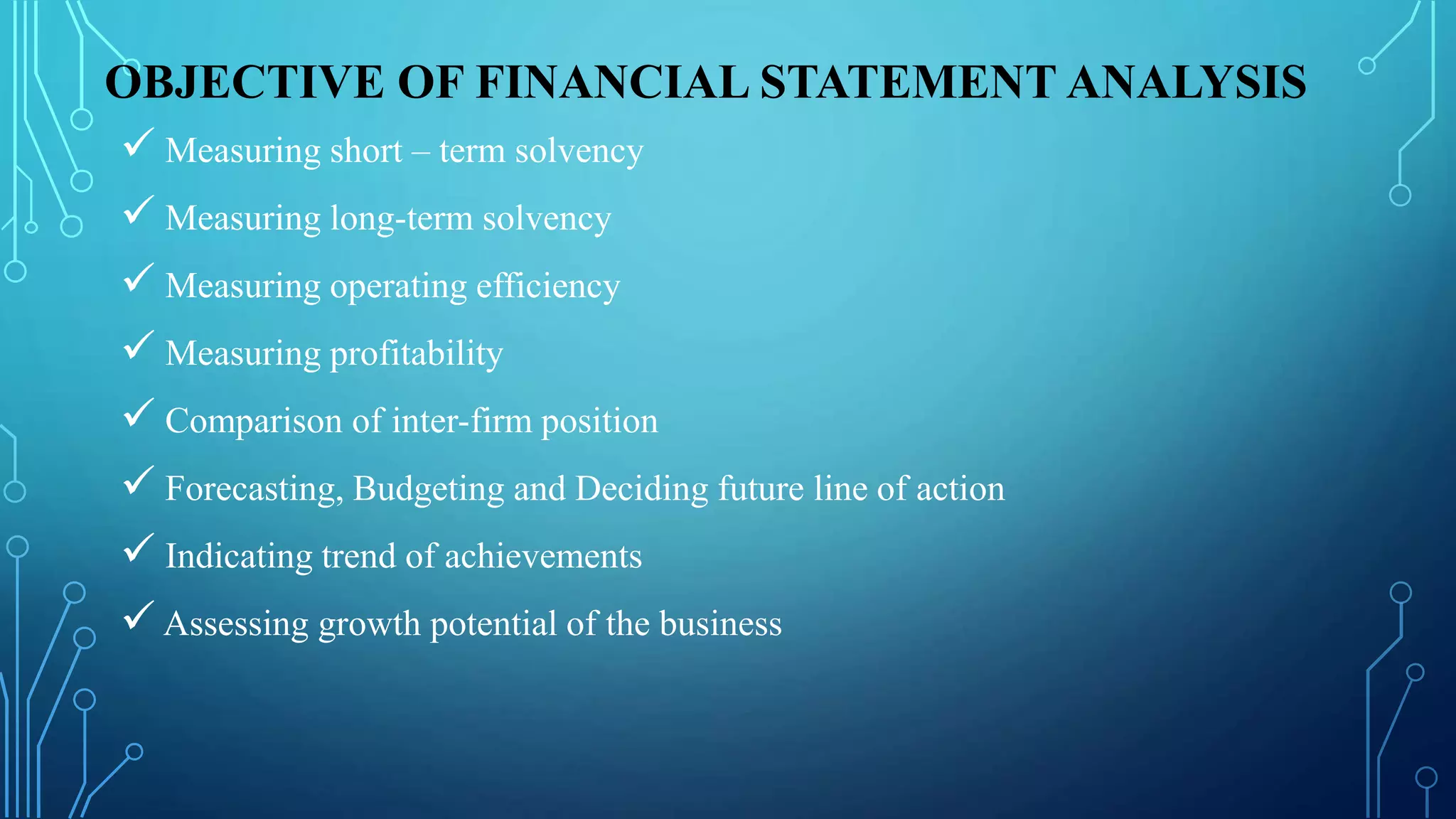

The document discusses financial statement analysis, defined as the evaluation of relationships among financial factors in a business. It outlines objectives such as measuring solvency and profitability, as well as the importance of the analysis for various stakeholders like management and investors. The document also addresses types, limitations, and tools associated with financial statement analysis.