Download to read offline

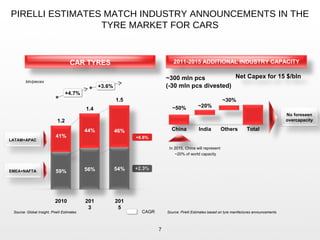

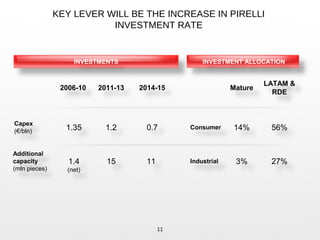

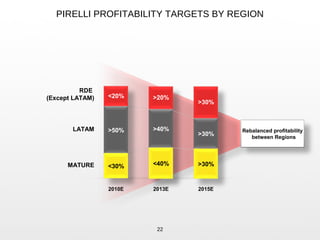

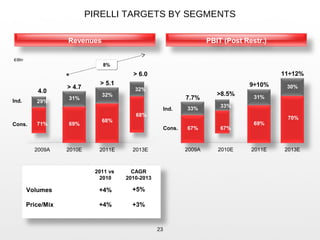

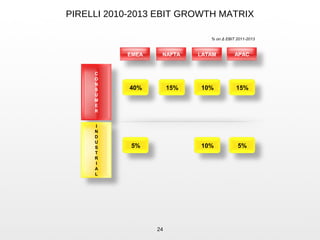

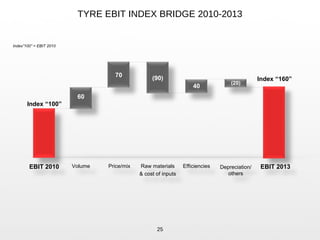

The document summarizes Pirelli's investments and targets from 2010-2013. It outlines Pirelli's strategy to increase investments and capacity across regions to capitalize on market growth, especially in premium segments. Key targets include doubling EBIT margins across most regions by 2013, growing revenues by over 30% with higher volumes and prices, and rebalancing profitability across consumer and industrial segments. Contingency plans and flexibility in sourcing strategies are also discussed to mitigate raw material cost risks.