Essential P&L and Cash Flow indicators

•Download as PPTX, PDF•

2 likes•490 views

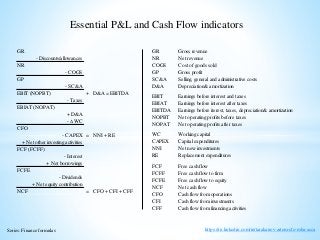

Non-finance people, and sometimes even professionals, confuse various finance ndicators, e.g. NOPAT (Net operating profits after taxes) with EBITDA (Earnings before interest, taxes, depreciation& amortization) or FCF (Free cash flow) with FCFE (Free cash flow to equity). Attached presentation visualizes linkage between major P&L and Cash Flow indicators.

Report

Share

Report

Share

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Vip ℂall Girls Safdarjung Phone No 9999965857 High Profile ℂall Girl Delhi No...

Vip ℂall Girls Safdarjung Phone No 9999965857 High Profile ℂall Girl Delhi No...

Economics - Development 01 _ Handwritten Notes.pdf

Economics - Development 01 _ Handwritten Notes.pdf

Canvas Business Model Infographics by Slidesgo.pptx

Canvas Business Model Infographics by Slidesgo.pptx

Economic Risk Factor Update: May 2024 [SlideShare]

Economic Risk Factor Update: May 2024 [SlideShare]

Top^Clinic Soweto ^%[+27838792658_termination in florida_Safe*Abortion Pills ...

Top^Clinic Soweto ^%[+27838792658_termination in florida_Safe*Abortion Pills ...

GLOBAL RESEARCH TREND AND FUTURISTIC RESEARCH DIRECTION VISUALIZATION OF WORK...

GLOBAL RESEARCH TREND AND FUTURISTIC RESEARCH DIRECTION VISUALIZATION OF WORK...

Indirect tax .pptx Supply under GST, Charges of GST

Indirect tax .pptx Supply under GST, Charges of GST

Top 5 Asset Baked Tokens (ABT) to Invest in the Year 2024.pdf

Top 5 Asset Baked Tokens (ABT) to Invest in the Year 2024.pdf

International economics – 2 classical theories of IT

International economics – 2 classical theories of IT

Featured

More than Just Lines on a Map: Best Practices for U.S Bike Routes

This session highlights best practices and lessons learned for U.S. Bike Route System designation, as well as how and why these routes should be integrated into bicycle planning at the local and regional level.

Presenters:

Presenter: Kevin Luecke Toole Design Group

Co-Presenter: Virginia Sullivan Adventure Cycling AssociationMore than Just Lines on a Map: Best Practices for U.S Bike Routes

More than Just Lines on a Map: Best Practices for U.S Bike RoutesProject for Public Spaces & National Center for Biking and Walking

Featured (20)

Content Methodology: A Best Practices Report (Webinar)

Content Methodology: A Best Practices Report (Webinar)

How to Prepare For a Successful Job Search for 2024

How to Prepare For a Successful Job Search for 2024

Social Media Marketing Trends 2024 // The Global Indie Insights

Social Media Marketing Trends 2024 // The Global Indie Insights

Trends In Paid Search: Navigating The Digital Landscape In 2024

Trends In Paid Search: Navigating The Digital Landscape In 2024

5 Public speaking tips from TED - Visualized summary

5 Public speaking tips from TED - Visualized summary

Google's Just Not That Into You: Understanding Core Updates & Search Intent

Google's Just Not That Into You: Understanding Core Updates & Search Intent

The six step guide to practical project management

The six step guide to practical project management

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Unlocking the Power of ChatGPT and AI in Testing - A Real-World Look, present...

Unlocking the Power of ChatGPT and AI in Testing - A Real-World Look, present...

More than Just Lines on a Map: Best Practices for U.S Bike Routes

More than Just Lines on a Map: Best Practices for U.S Bike Routes

Ride the Storm: Navigating Through Unstable Periods / Katerina Rudko (Belka G...

Ride the Storm: Navigating Through Unstable Periods / Katerina Rudko (Belka G...

Good Stuff Happens in 1:1 Meetings: Why you need them and how to do them well

Good Stuff Happens in 1:1 Meetings: Why you need them and how to do them well

Essential P&L and Cash Flow indicators

- 1. https://ru.linkedin.com/in/tarakanov-artem-cfo-mba-acca Essential P&L and Cash Flow indicators Series: Finance formulas GR - Discounts/allowances NR - COGS GP - SC&A EBIT (NOPBT) + D&A = EBITDA - Taxes EBIAT (NOPAT) + D&A - DWC CFO - CAPEX = NNI + RE + Net other investing activities FCF (FCFF) - Interest + Net borrowings FCFE - Dividends + Net equity contribution NCF = CFO + CFI + CFF GR Gross revenue NR Net revenue COGS Cost of goods sold GP Gross profit SC&A Selling, general and administrative costs D&A Depreciation& amortization EBIT Earnings before interest and taxes EBIAT Earnings before interest after taxes EBITDA Earnings before iterest, taxes, depreciation& amortization NOPBT Net operating profits before taxes NOPAT Net operating profits after taxes WC Working capital CAPEX Capital expenditures NNI Net new investments RE Replacement expenditures FCF Free cash flow FCFF Free cash flow to firm FCFE Free cash flow to equity NCF Net cash flow CFO Cash flow from operations CFI Cash flow from investments CFF Cash flow from financing activities

- 2. Net other investing activities + Receipts in the form of company loans - Payments in the form of company loans + Receipts from Fixed assets sales - Payments to purchase bonds or shares of other companies Net equity contribution + Receipts from issuing stock - Re-acquisition of stock - Dividends https://ru.linkedin.com/in/tarakanov-artem-cfo-mba-accaSeries: Finance formulas Essential P&L and Cash Flow indicators + EBIT CFO - Taxes + D&A - DWC - CAPEX + Receipts in the form of company loans CFI - Payments in the form of company loans + Receipts from Fixed assets sales - Payments to purchase bonds or shares of other companies + Receipts from issuing stock - Re-acquisition of stock CFF* - Dividends + Debt principals raised - Debt principals paid - Interest *IFRS classification + Interest CF to debtholders - Debt principals raised + Debt principals paid - Dividends CF to shareholders - Receipts from issuing stock + Re-acquisition of stock CF to investors = CF to debtholders + CF to shareholders Net borrowings + Debt principals raised - Debt principals paid