The document discusses several topics related to accounting and business goals:

1. The long-term goals of businesses are to maximize benefits for owners, such as profits or company value. This requires producing high-quality products at low costs.

2. An example is given of investing money in education to earn a higher future salary, rather than spending it immediately. This illustrates how capital is created by postponing current consumption.

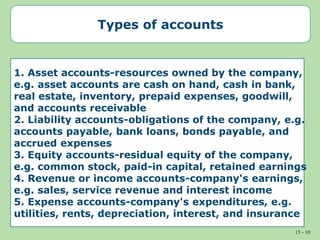

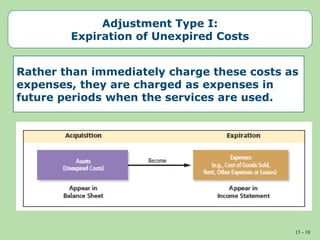

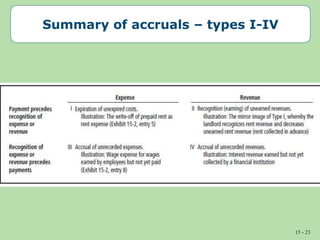

3. Businesses use accounting to quantify inputs, processes, and outputs in monetary terms. There are various types of accounts like assets, liabilities, equity, revenues and expenses. Adjusting entries are made at the end of each accounting period to record implicit transactions like expired costs or accrued