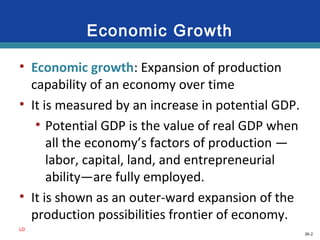

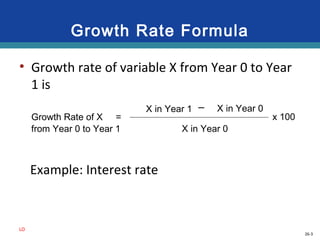

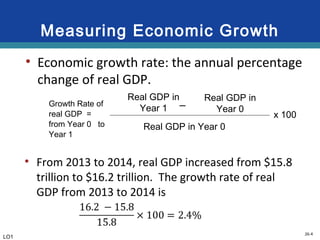

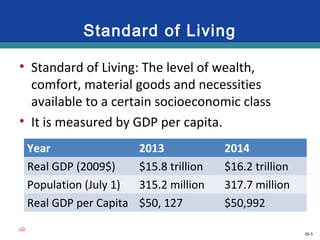

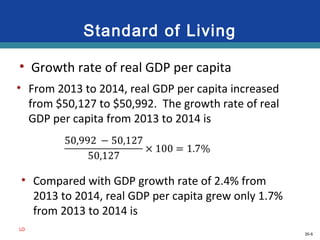

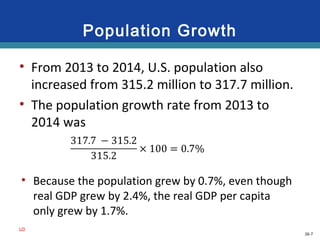

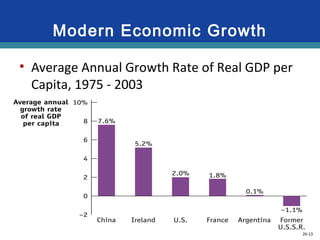

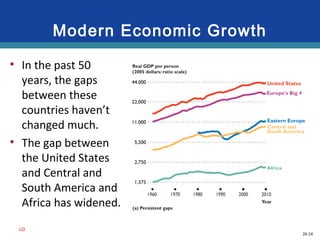

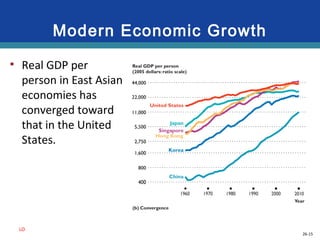

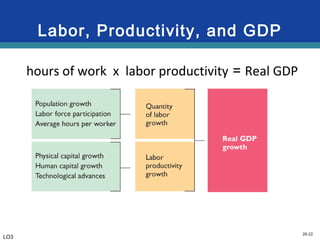

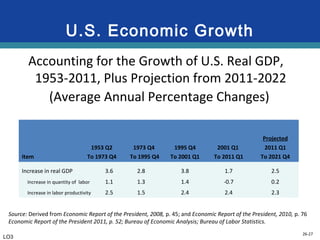

This document discusses economic growth and factors that influence it. It defines economic growth as an increase in potential GDP over time, measured by expanding production capabilities. Growth rates are calculated by comparing GDP values between years. Economic growth increases standards of living by raising GDP per capita. While population growth reduces growth in GDP per person, productivity gains can outweigh this effect and allow sustained increases in living standards over long periods. Factors driving productivity and growth include investment in physical and human capital, technology advances, and strong economic institutions.