Downloaded 10 times

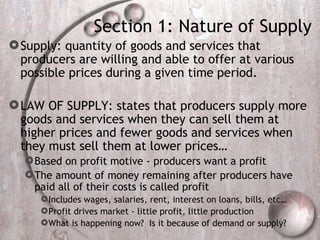

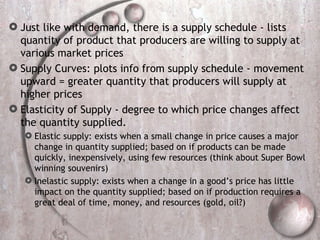

The document summarizes key concepts related to supply in microeconomics. It defines supply as the quantity of goods producers are willing to offer at various prices. The law of supply states that producers will supply more goods at higher prices and fewer goods at lower prices, based on seeking profit. Supply is determined by factors like the prices of resources, government interventions, technology, competition from other producers, and producer expectations about the future. Firms analyze costs of production like fixed, variable, total, and marginal costs to determine optimal production levels.