Download as PDF, PPTX

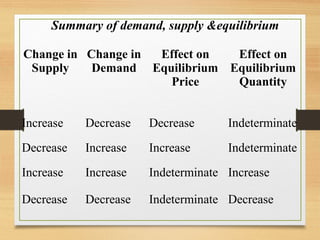

![Demand Schedule

Point Price [Rs per unit]

Quantity demanded of X

[kg. per month]

a

b

c

d

e

f

0.50

1.00

2.00

2.50

1.50

7.0

3.

52.5

3.00

5.0

1.0

1.5

1 2 3

0.50

1.00

2.00

Quantity of X

PriceofX

3.00

2.50

654 7

Demand Curve

a

b

c

e

d

f

1.50

Demand schedule](https://image.slidesharecdn.com/demandandsupply-180823131110/85/Demand-and-supply-5-320.jpg)

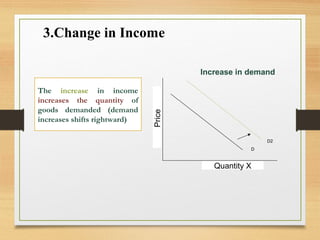

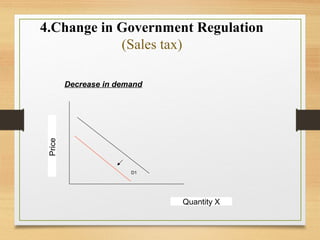

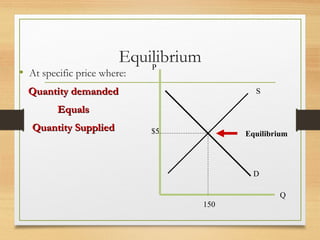

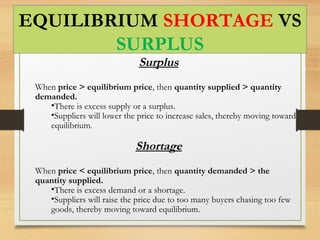

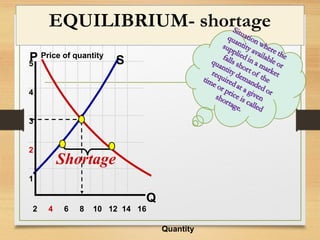

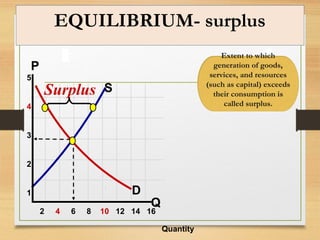

This document summarizes key concepts of demand and supply, including: - Demand is the quantity of a good consumers will purchase at a given price, governed by the law of demand. Supply is the quantity produced at a given price, governed by the law of supply. - Equilibrium occurs when quantity demanded equals quantity supplied at the equilibrium price. - Factors like income, tastes, prices of substitutes/complements can shift the demand curve. Factors like technology, input prices, and number of producers can shift the supply curve. - When price is above equilibrium, a surplus occurs. When price is below equilibrium, a shortage occurs bringing prices back to equilibrium.