Download to read offline

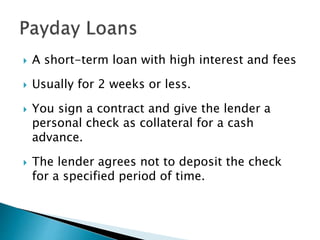

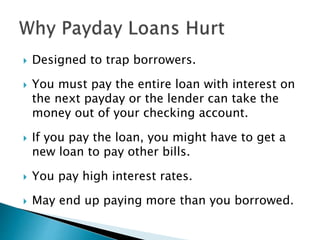

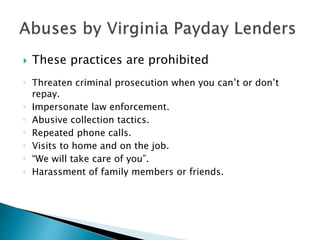

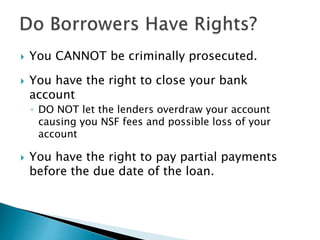

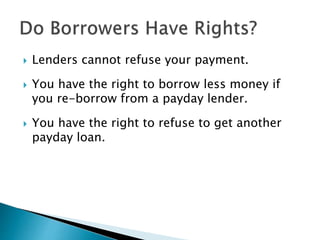

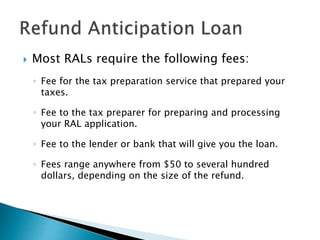

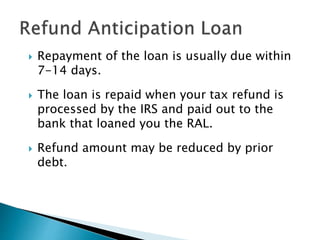

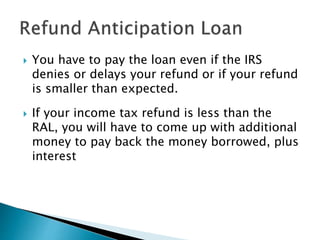

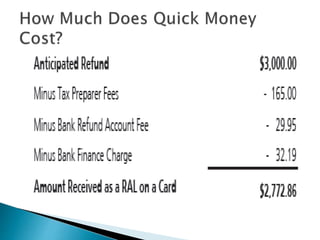

This document discusses predatory lending practices and provides consumer protection information. It summarizes types of predatory loans like payday loans, car title loans, and refund anticipation loans. It describes common predatory loan terms and tactics to trap borrowers, as well as consumers' rights. The document advises seeking alternatives to high-cost loans and provides contact information for consumer assistance agencies.