Download to read offline

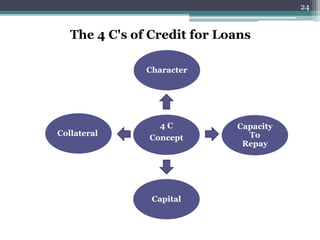

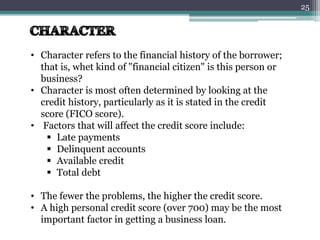

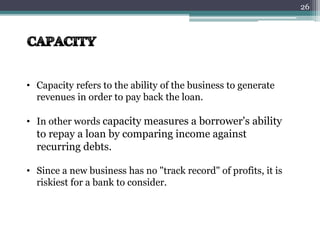

The document discusses various types of loans including secured loans, unsecured loans, open-ended loans, closed-ended loans, and more specific loans like personal loans, home loans, vehicle loans, student loans, business loans, and payday loans. It explains the key characteristics of each type of loan such as whether they require collateral, have fixed repayment terms, or can be repeatedly borrowed against. The 4 C's of lending are also summarized as the main criteria lenders evaluate which are the borrower's character, capacity to repay, capital or collateral, and the conditions of the loan.