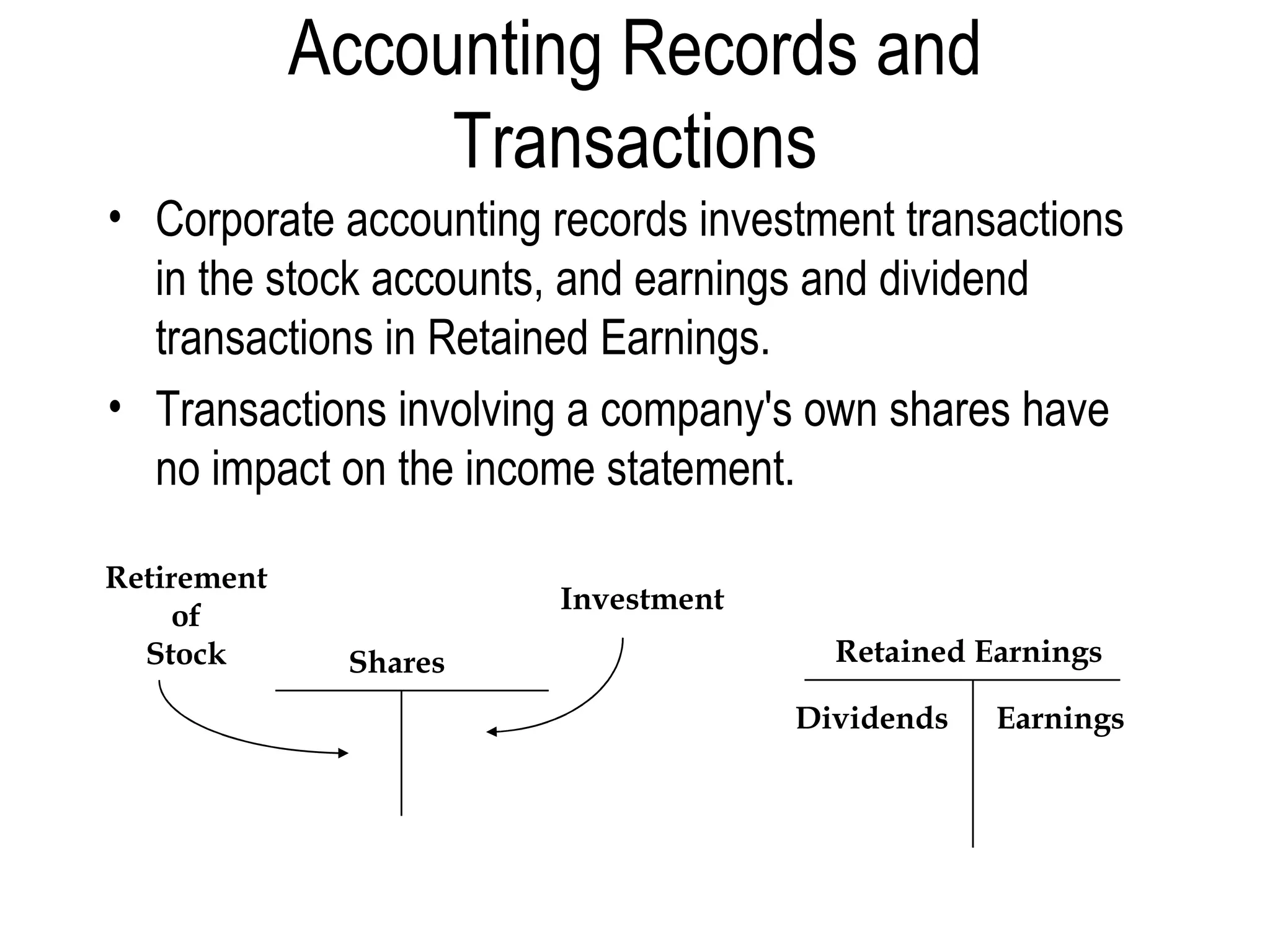

Corporations have several key characteristics including separate legal entity status, limited liability for shareholders, transferable ownership through share trading, and continuous life regardless of ownership changes. A corporation is formed through registration and establishes a board of directors elected by shareholders to oversee policy and delegate daily operations. Financial statements include an income statement, statement of retained earnings, and balance sheet that account for transactions involving shares, earnings, dividends and retained earnings.