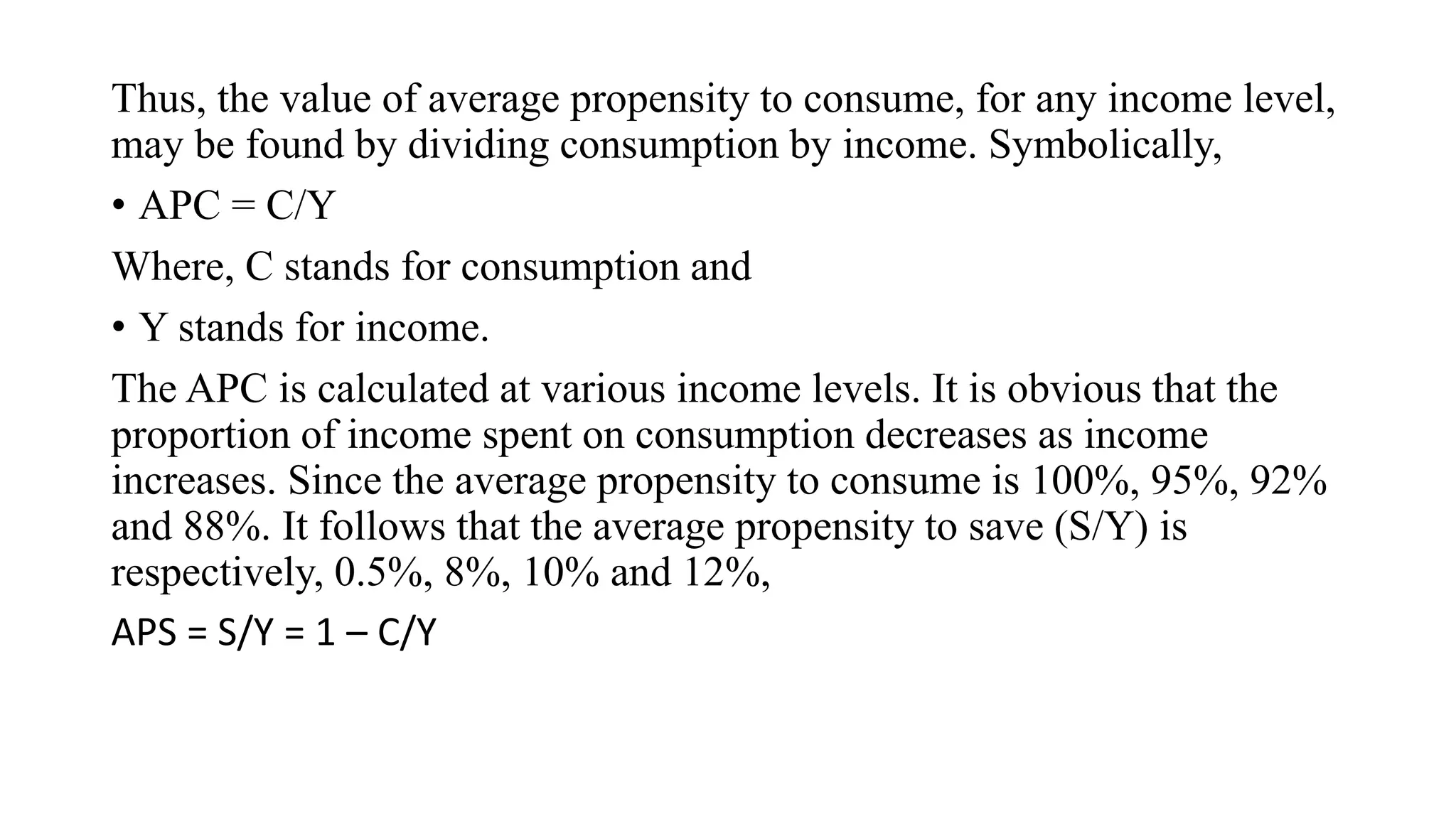

The document discusses the consumption function introduced by economist John Maynard Keynes, which illustrates the relationship between real disposable income and consumer spending. It explains key concepts such as average propensity to consume (APC) and marginal propensity to consume (MPC), detailing how they are calculated and their significance in understanding overall consumption behavior in an economy. The text further examines factors influencing consumption and the variations of these propensities across different economic contexts.