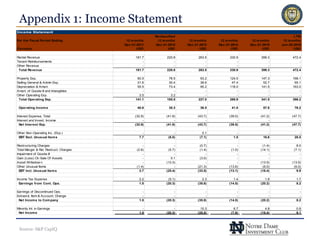

This document provides an analysis and recommendation for CyrusOne, Inc. (CONE). It summarizes CONE's business operations as a data center REIT, industry drivers of cloud computing demand, and CONE's strategic positioning. Financial projections through 2020 show increasing revenue, NOI, and unlevered free cash flow. Comparable company analyses find CONE trading at a discount to NAV. The analysts recommend the Notre Dame Investment Club purchase CONE due to its strategic positioning, interconnection revenue growth opportunities, acquisition and development patterns, and discount to estimated NAV.