Comparative Analysis - Section 25 Company, Society, Trust and Private Limited Company

The document compares and contrasts trusts, societies, section 25 companies, and private limited companies across various areas such as permitted scope of activities, ownership, setting up process, compliance requirements, management control, and tax implications. Some key highlights: - Trusts can be created for any lawful purpose while societies can only be created for specific charitable/educational purposes. Section 25 companies and private limited companies can be set up for profit/non-profit activities. - Trusts and societies have trustees/members as owners, while companies have shareholders as owners. - Setting up a trust is simpler than other forms which require registrations with regulatory authorities. - Compliance requirements are less for trusts which do not

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Comparative Analysis - Section 25 Company, Society, Trust and Private Limited Company

Similar to Comparative Analysis - Section 25 Company, Society, Trust and Private Limited Company (20)

More from Prabhjeet Gill

Recently uploaded

Recently uploaded (13)

Comparative Analysis - Section 25 Company, Society, Trust and Private Limited Company

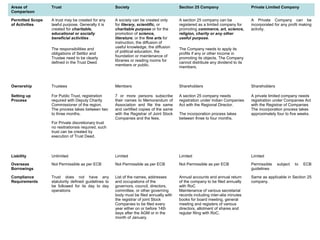

- 1. Areas of Comparison Trust Society Section 25 Company Private Limited Company Permitted Scope of Activities A trust may be created for any lawful purpose. Generally it is created for charitable, educational or socially beneficial activities . A society can be created only for literary, scientific, or charitable purpose or for the promotion of science, literature, or the fine arts for instruction, the diffusion of useful knowledge, the diffusion of political education, the foundation or maintenance of libraries or reading rooms for members or public. A section 25 company can be registered as a limited company for promoting commerce, art, science, religion, charity or any other useful purpose. A Private Company can be incorporated for any profit making activity. The responsibilities and obligations of Settlor and Trustee need to be clearly defined in the Trust Deed. The Company needs to apply its profits if any or other income in promoting its objects. The Company cannot distribute any dividend to its members. Ownership Trustees Members Shareholders Shareholders Setting up Process For Public Trust, registration required with Deputy Charity Commissioner of the region. The process takes between two to three months. 7 or more persons subscribe their names to Memorandum of Association and file the same and certified copies of the same with the Registrar of Joint Stock Companies and the fees. A section 25 company needs registration under Indian Companies Act with the Regional Director. A private limited company needs registration under Companies Act with the Registrar of Companies The incorporation process takes approximately four to five weeks. The incorporation process takes between three to four months. For Private discretionary trust no resitrationsis required, such trust can be created by execution of Trust Deed. Liability Unlimited Limited Limited Limited Overseas Borrowings Not Permissible as per ECB Not Permissible as per ECB Not Permissible as per ECB Permissible guidelines Compliance Requirements Trust does not have any statutorily defined guidelines to be followed for its day to day operations List of the names, addresses and occupations of the governors, council, directors, committee, or other governing body must be filed annually with the registrar of joint Stock Companies to be filed every year either on or before 14th days after the AGM or in the month of January. Annual accounts and annual return of the company to be filed annually with RoC Maintenance of various secretarial records including inter-alia minutes books for board meeting, general meeting and registers of various directors, allotment of shares and regular filing with RoC. Same as applicable in Section 25 company. subject to ECB

- 2. Areas of Comparison Trust Society Section 25 Company Private Limited Company Alteration of Objects Difficulty in modifying objects and impossible in the event of original settlers being unavailable or unwilling. Objects can be modified with the approval of 3/5ths of the members Objects can be modified anytime subject to approval of Central Govt Can be modified in accordance with procedure prescribed. Management Control Trustees as appointed under the Trust deed. Governing Council as elected by the society members. Directors as appointed by the shareholders. Directors as appointed by the shareholders. Operational Control Trustees in line with the Trust Deed Governing councils / directors / committee Directors in line with the MOA and AOA Directors in line with the MOA and AOA Members Participation Trustees have the final say As per the MOA of the society. All the rights of the shareholders as per the Companies Act and MOA, ordinary resolution, special resolution etc. All the rights of the shareholders as per the Companies Act and MOA, ordinary resolution, special resolution etc. Termination The trust can be dissolved by Settlor Can be dissolved by 3/5th of the members. Winding up is a cumbersome and time consuming process which can take anywhere between 10-12 months Same as applicable in Section 25 company. Funding (Foreign Contribution Regulation Act) If grants are received directly by the Trust from overseas, approval of Ministry of Home Affairs under Foreign Contribution Regulation Act is required which is a time consuming process and can take up to four to six months. In case of a foreign trustee, credibility of the foreign trustee needs to be established before the regulator. If grants are received directly by the Society from overseas, approval of Ministry of Home Affairs under Foreign Contribution Regulation Act is required which is a time consuming process and can take up to four to six months. If grants are received directly by the Company from overseas, approval of Ministry of Home Affairs under Foreign Contribution Regulation Act is required which is a time consuming process and can take up to four to six months. Subject to Foreign Exchange laws Repatriation of funds Profits to be utilized for the furtherance of the trust objectives and for beneficiaries and any form of repatriation would require RBI approval. Funds to be utilized for the furtherance of society's objectives only and in case of dissolution to be transferred to other society – Repatriation not possible. Prohibition on distribution of dividend – so repatriation not possible Funds are freely repatriable in form of dividends or on liquidation subject to provisions of Companies Act and payment of applicable taxes.

- 3. Areas of Comparison Trust Society Section 25 Company Private Limited Company Exchange Control/ FDI policy Where an Indian trust has either a foreign trustee or a foreign beneficiary, provisions of exchange control regulations will apply N/A Ownership of stock in the company would be governed by the FDI policy of the Government of India Same as applicable in Section 25 company. In case of foreign trustee In case the trust has foreign trustee certain assets which are statutorily required to be registered, such as immovable properties, would be registered in name of trustee. This shall entail prior approval of Reserve Bank of India (RBI), which will not be possible as a non resident in not permitted to own immovable property in India. In case of foreign beneficiary In case of a foreign beneficiary prior RBI approval would need to be obtained on account of the ability to make remittances in future and distribution on dissolution of the trust. In our experience, obtaining such an approval is again extremely difficult In summary, if a trust structure is to be set up, there should be no foreign beneficiary. In case there are foreign trustees, then the trust cannot own immovable property. As per the FDI policy, the following activities fall under automatic route, i.e. no Government approval is required -educational research -publishing of books (not magazines & periodicals) -tendering scholarships -education (AICTE and University Grants Commission (UGC) guidelines, prohibit a company form of entity for setting up a college, university or educational institute.

- 4. Areas of Comparison Trust Society Section 25 Company Private Limited Company Transfer of Ownership Not permissible Permissible with appointment of new members and resigning of old members and approved by 3/5ths members resolution By transfer of shares By transfer of shares Tax Implications in hands of entity running the institution Tax exemption can be sought u/s 10(23C) of IT Act after obtaining requisite approvals Same as Trust Same as Trust Profits earned from running the institution would be taxable as in hands of the company @ 33.99% [Exemption available to university or educational institution existing solely for educational purposes and not for purposes of profit] Tax exemption not available as activities would be construed as ‘for purposes of profit’ Entity to obtain approval for eligibility u/s 80G of IT Act. Tax Implications in hands of entity providing funds 50% of the amount of donations eligible for deduction u/s 80G of the IT Act Same as Trust 50% of the amount of donations eligible for deduction u/s 80G of the IT Act unless contributions in the nature of ‘share capital’