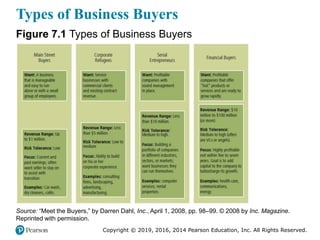

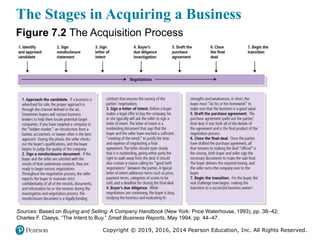

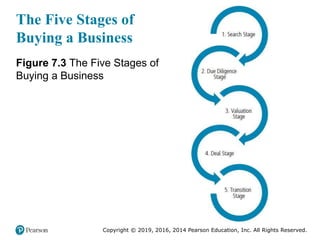

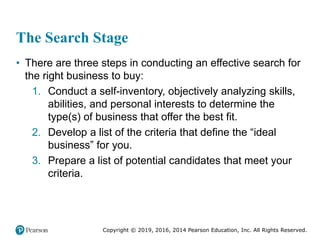

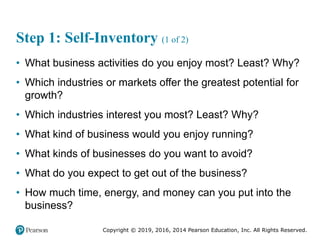

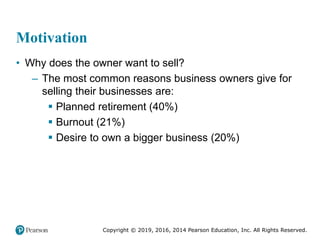

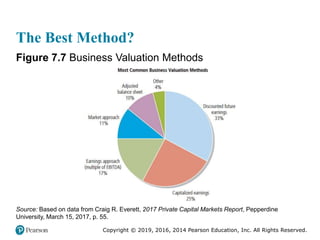

The document discusses the process of buying an existing business, outlining the key stages and considerations. It begins with conducting self-analysis and developing criteria to identify suitable businesses. The stages of acquisition include search, due diligence, valuation, deal, and transition. Due diligence involves assessing the seller's motivation, business assets, legal issues, and financials. Valuation methods include balance sheet, earnings, and market approaches. The deal involves negotiating terms that achieve both the buyer and seller's goals, such as price, payment structure, and non-compete agreements.