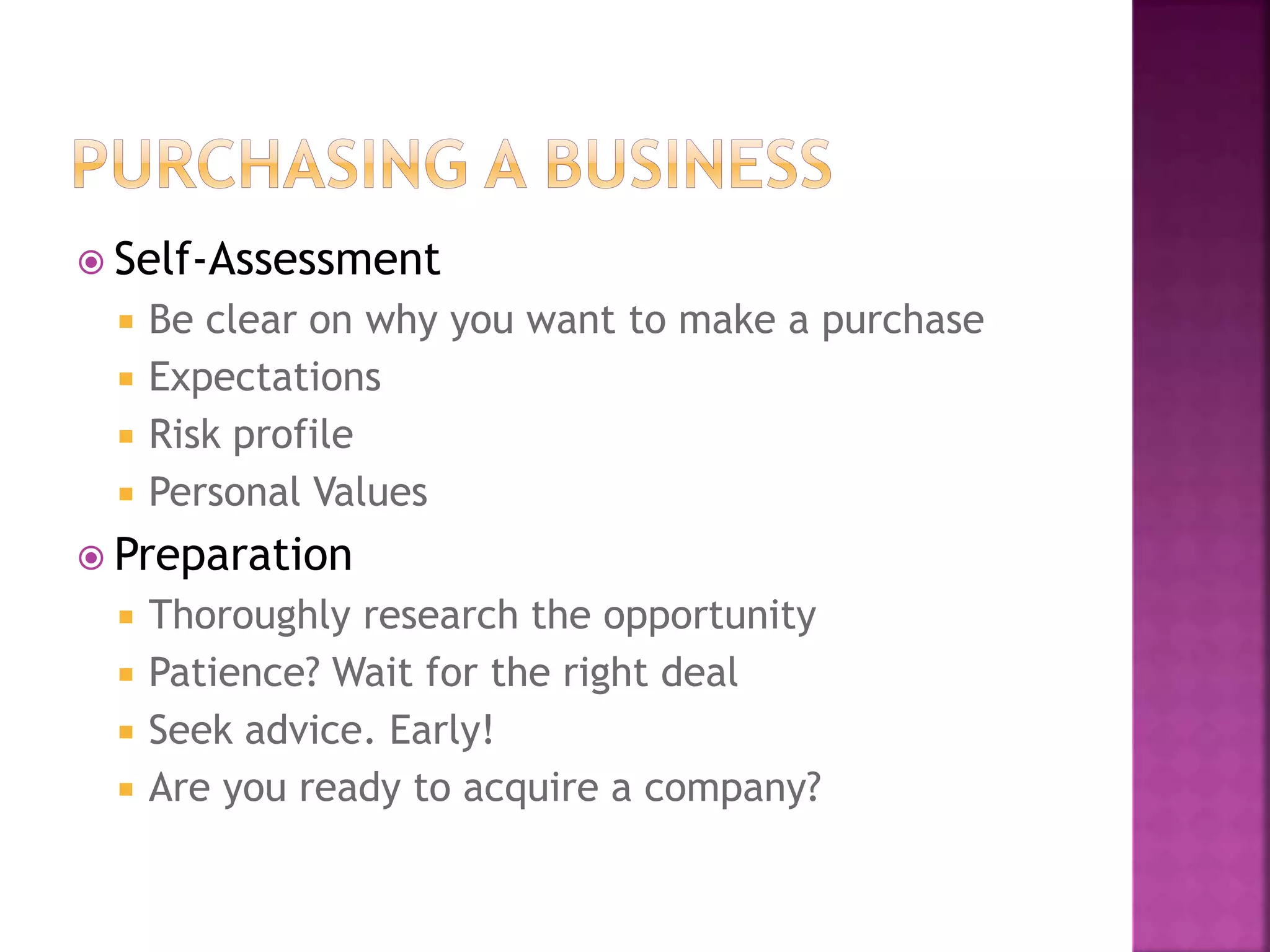

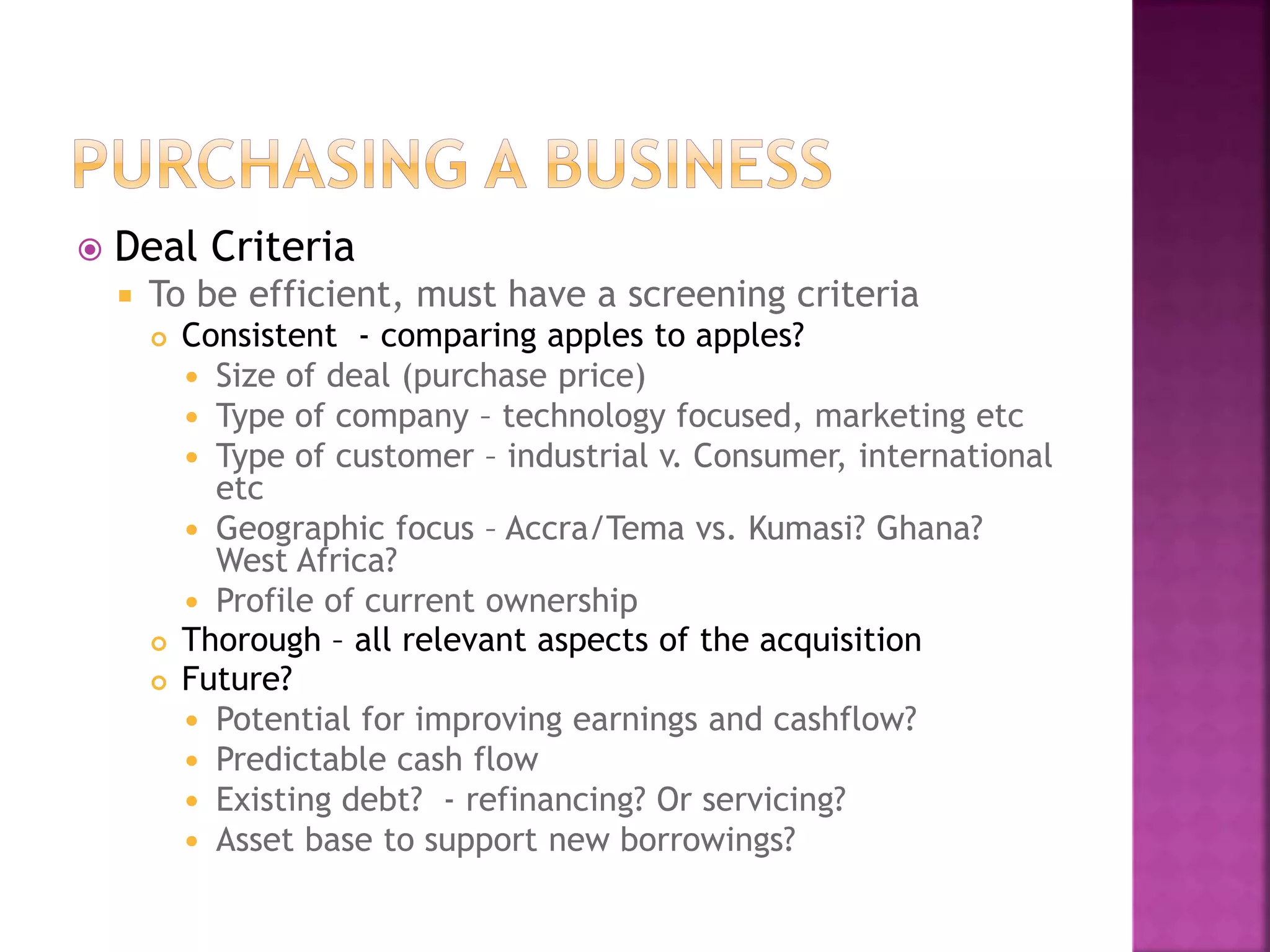

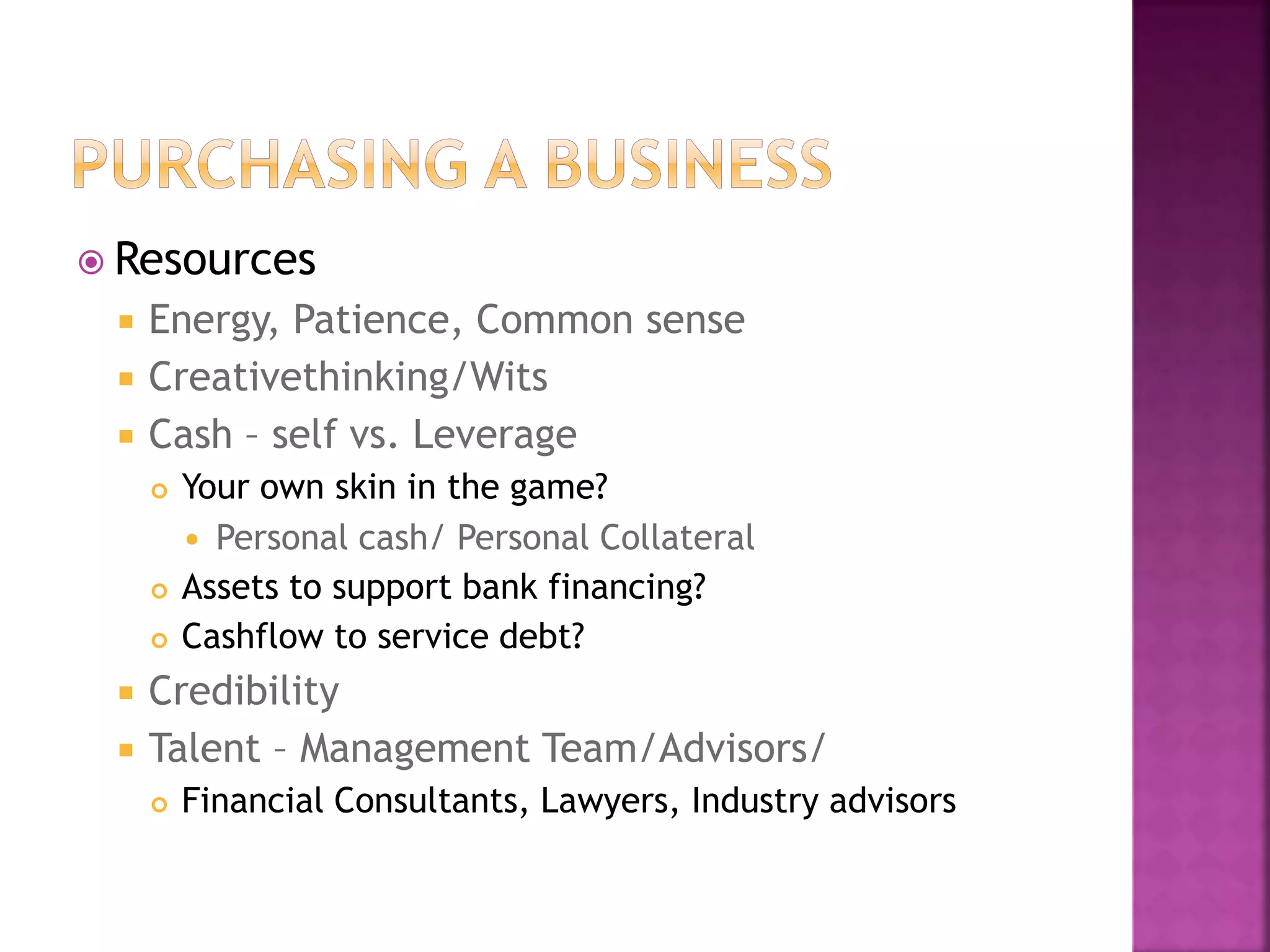

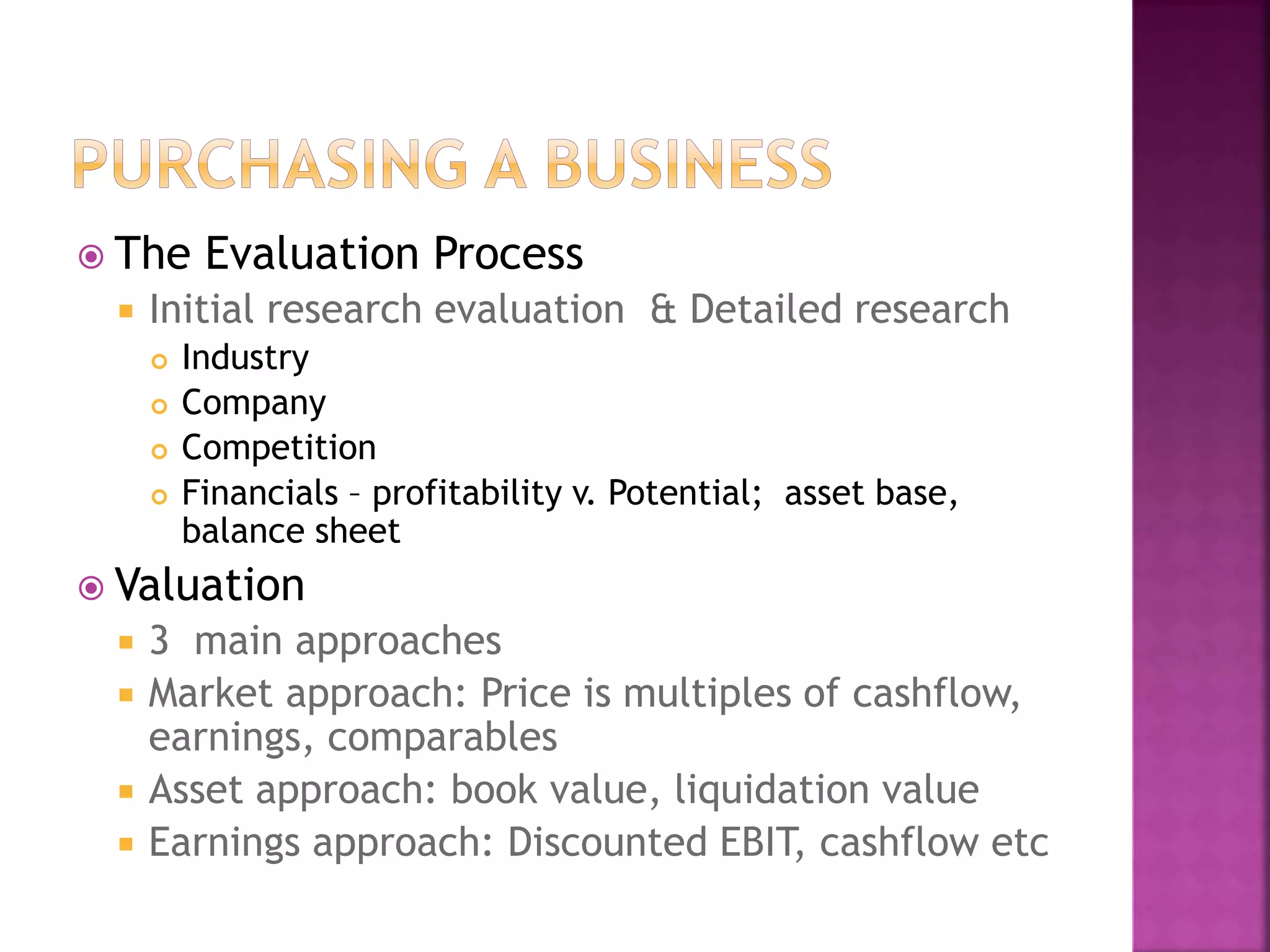

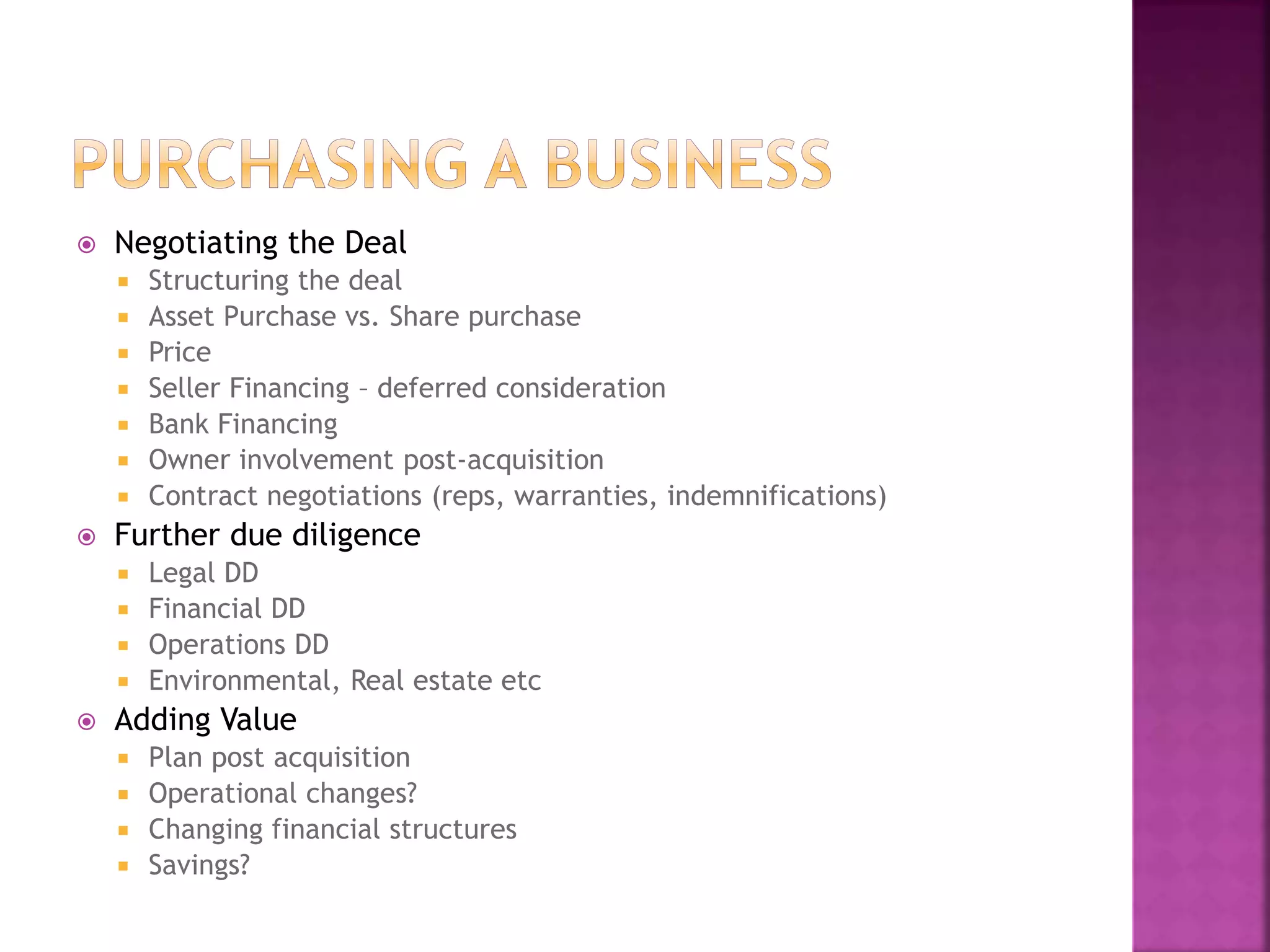

This class covered idea generation and the build or buy decision process for acquiring a business. It discussed starting a business from scratch, acquiring an existing business, or operating a franchise. The class covered self-assessment, thorough research of opportunities, deal criteria, sources, resources, evaluation process, negotiation, and the pros and cons of acquisition. Key aspects included clear goals, patience, screening criteria, industry and company research, valuation approaches, negotiating price and structure, and due diligence of legal, financial, and operational areas. Success requires acquisition skills, focus, entrepreneurial drive to add value, and access to capital and technical skills.