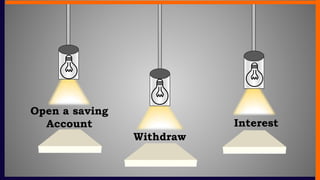

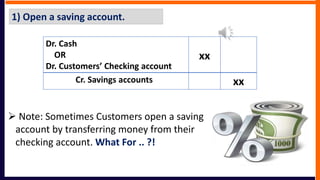

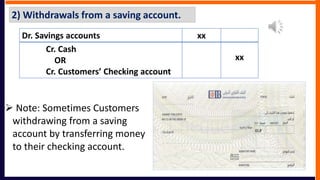

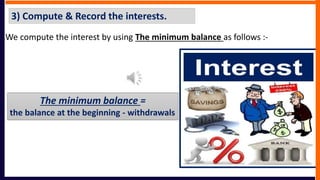

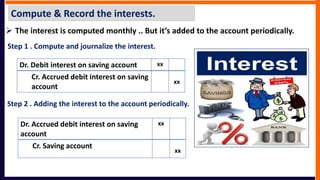

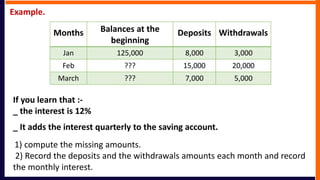

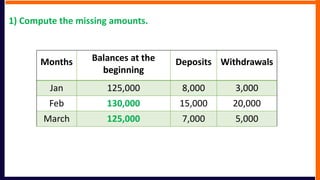

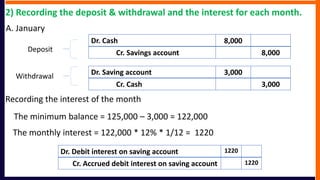

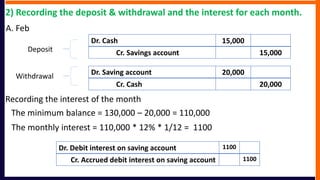

This document discusses the accounting treatment for savings accounts. It begins by defining savings accounts as accounts meant for non-trading customers to save money with limited transactions. The key steps in accounting for savings accounts are: 1) Open a savings account by depositing funds from cash or a checking account, 2) Withdraw funds from the savings account to cash or a checking account, and 3) Compute and record monthly interest earned on the minimum balance in the account. Interest is calculated using the minimum monthly balance and is recorded initially as an accrued interest account before being added to the savings account periodically. An example is provided to demonstrate computing minimum balances and recording deposits, withdrawals, and monthly interest for three months.

![accounting final projec G 35 t[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountingfinalprojecg35t1-231002133737-cf59e07d-thumbnail.jpg?width=640&height=640&fit=bounds)