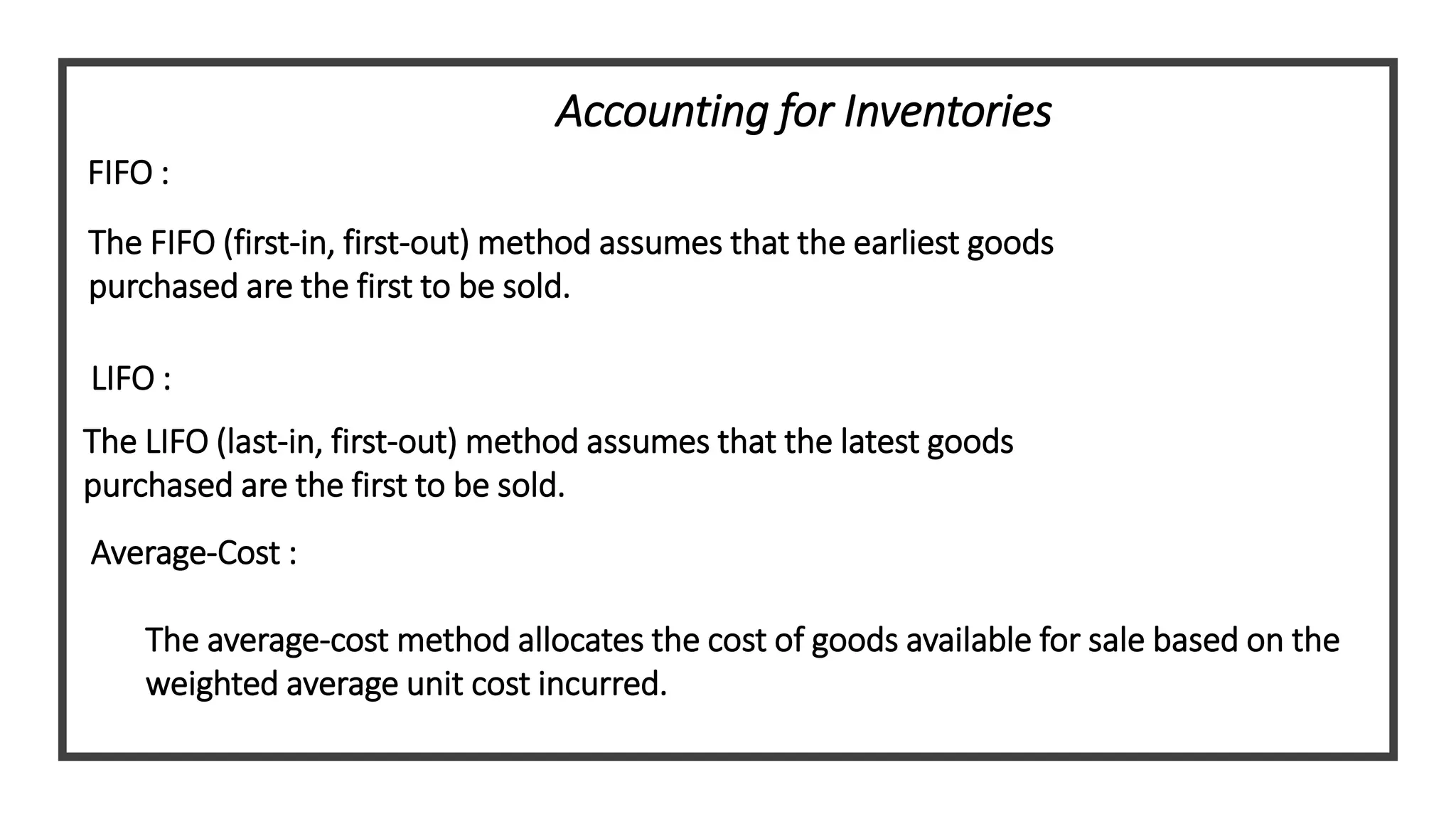

This document discusses an accounting project for Nike company. It provides details on Nike's background, products, use of the perpetual inventory system and weighted average cost method. It also discusses plant assets and calculating ratios like inventory turnover and asset turnover for Nike. Plant assets are depreciated on a straight-line basis over 2-40 years for different asset types at Nike.

![accounting final projec G 35 t[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/accountingfinalprojecg35t1-231002133737-cf59e07d-thumbnail.jpg?width=640&height=640&fit=bounds)