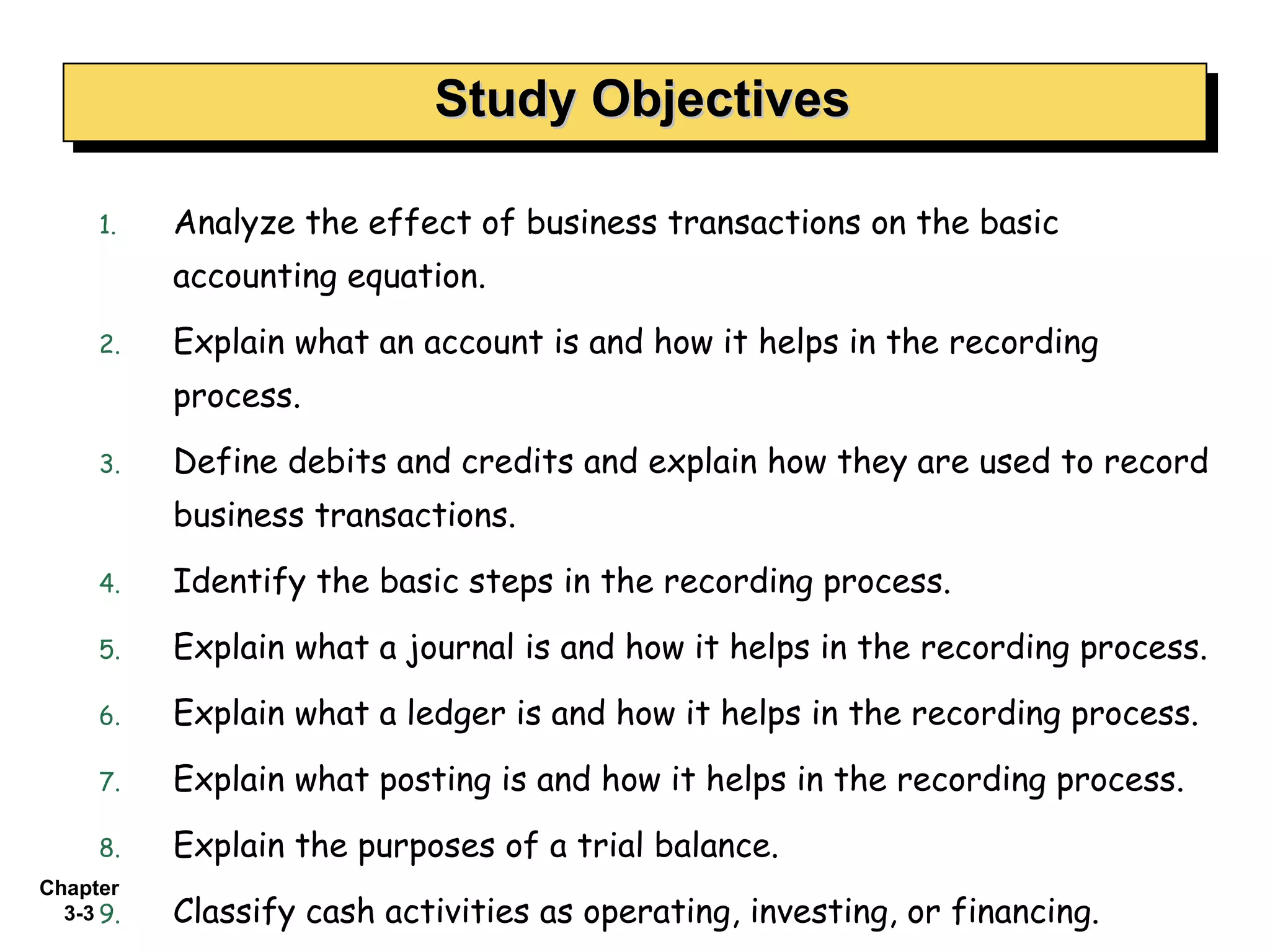

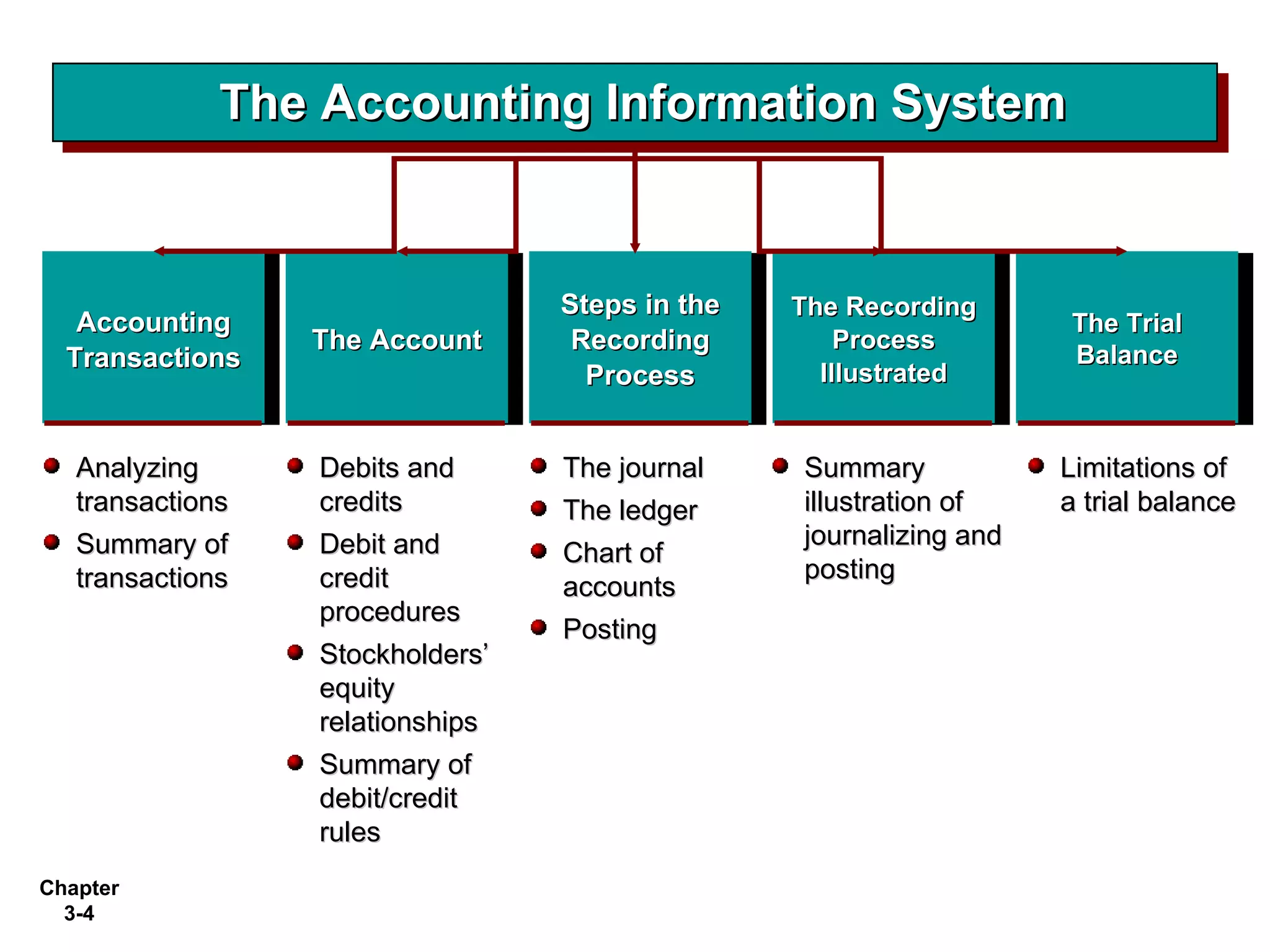

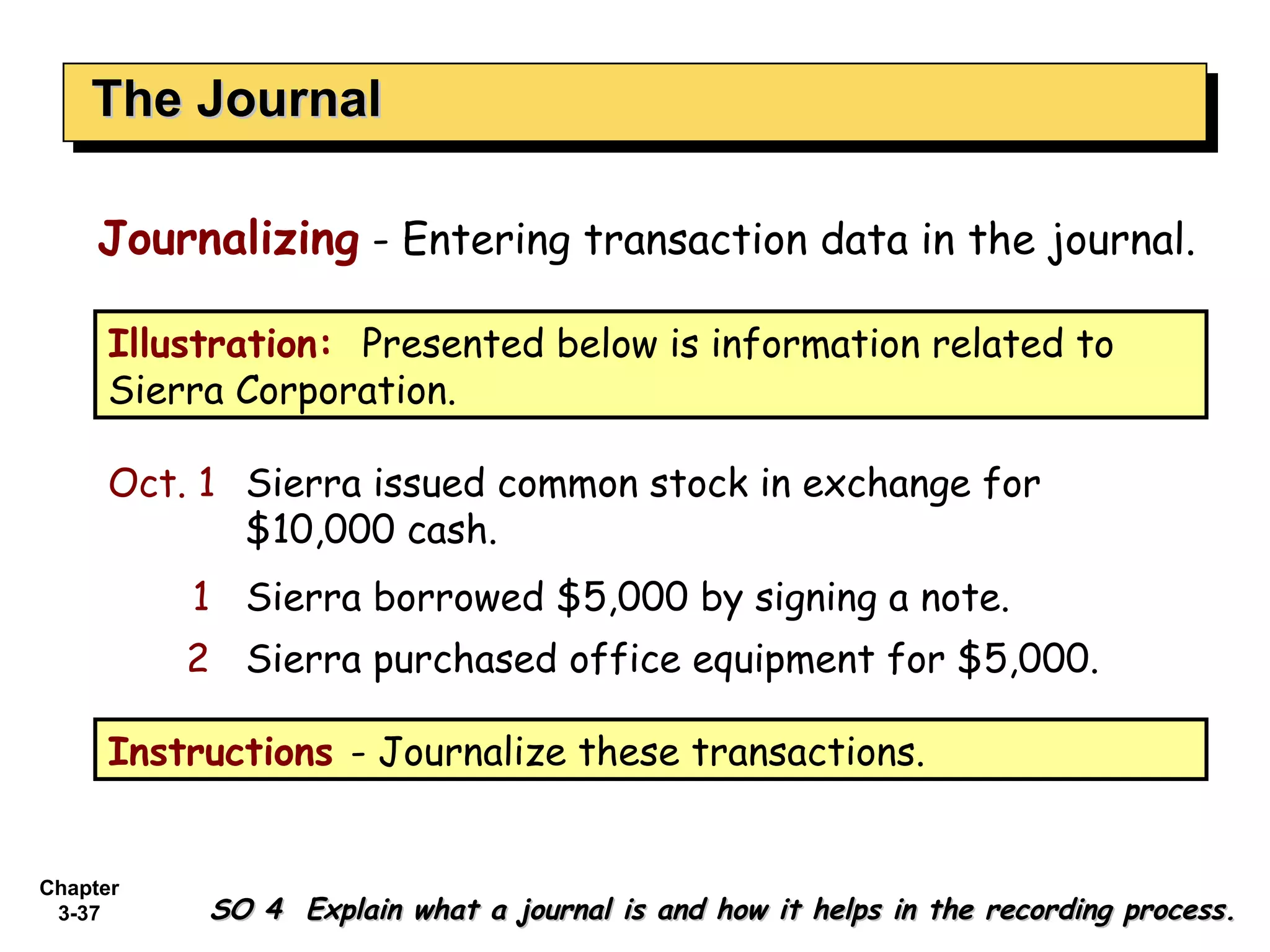

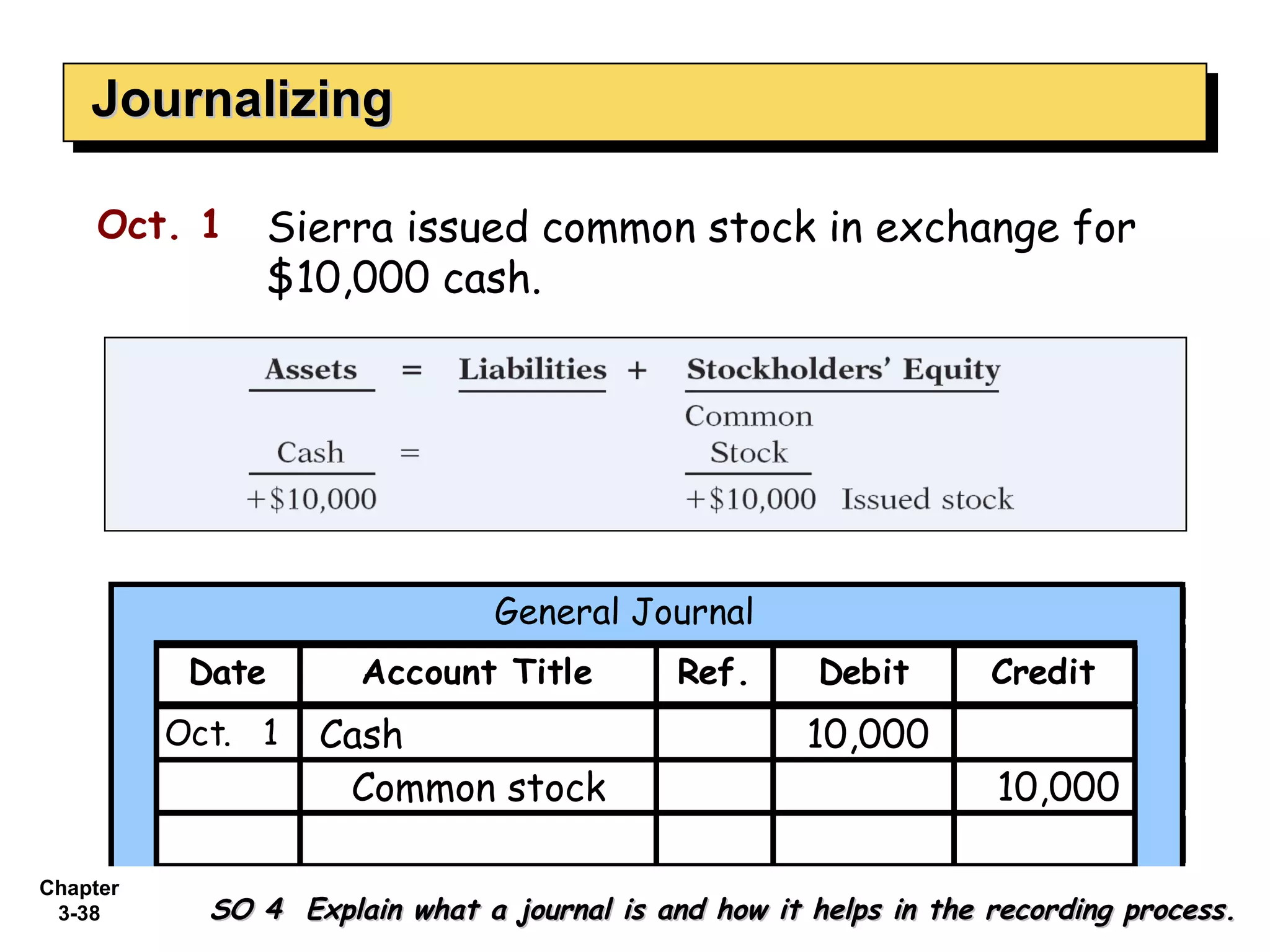

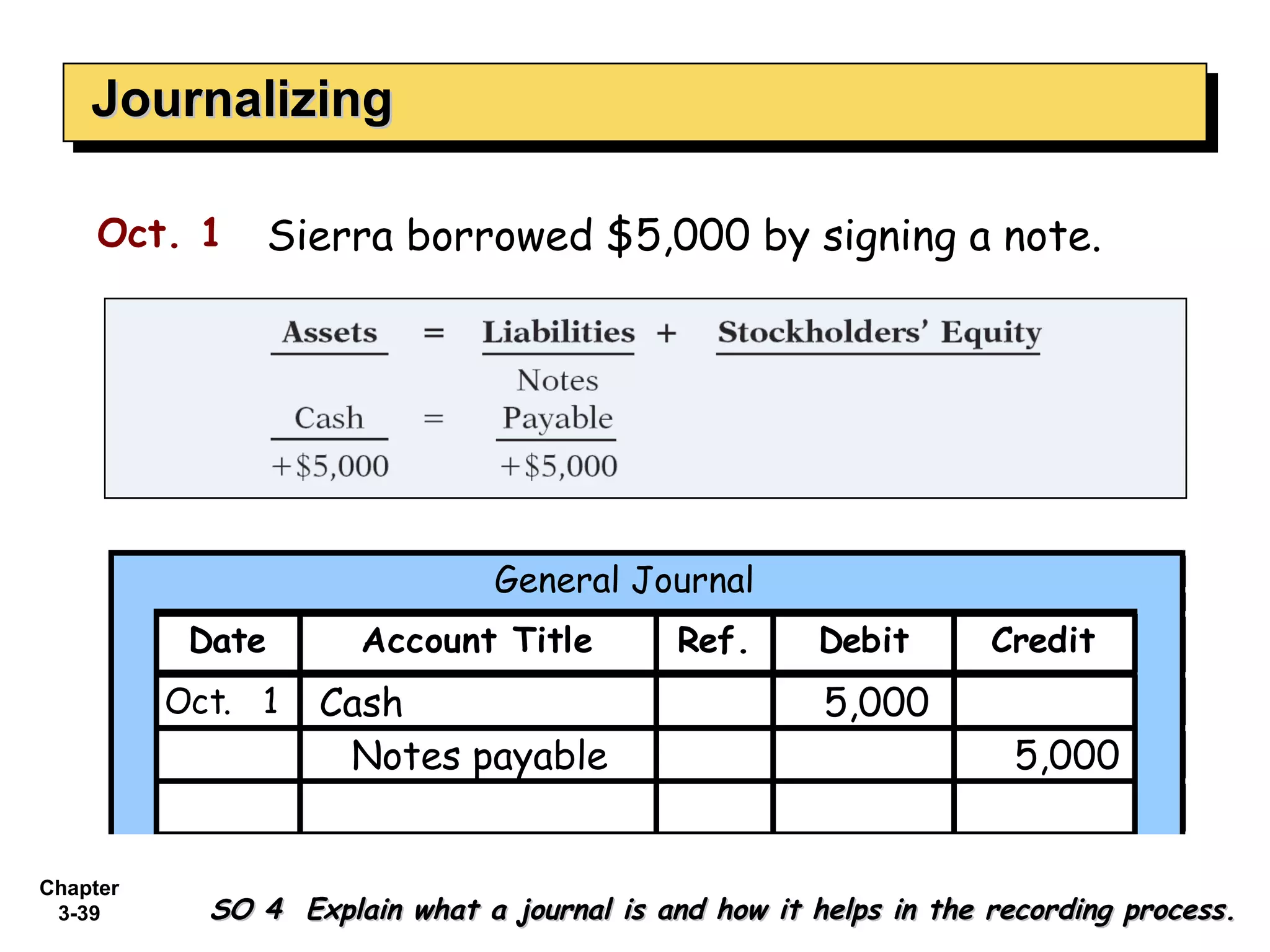

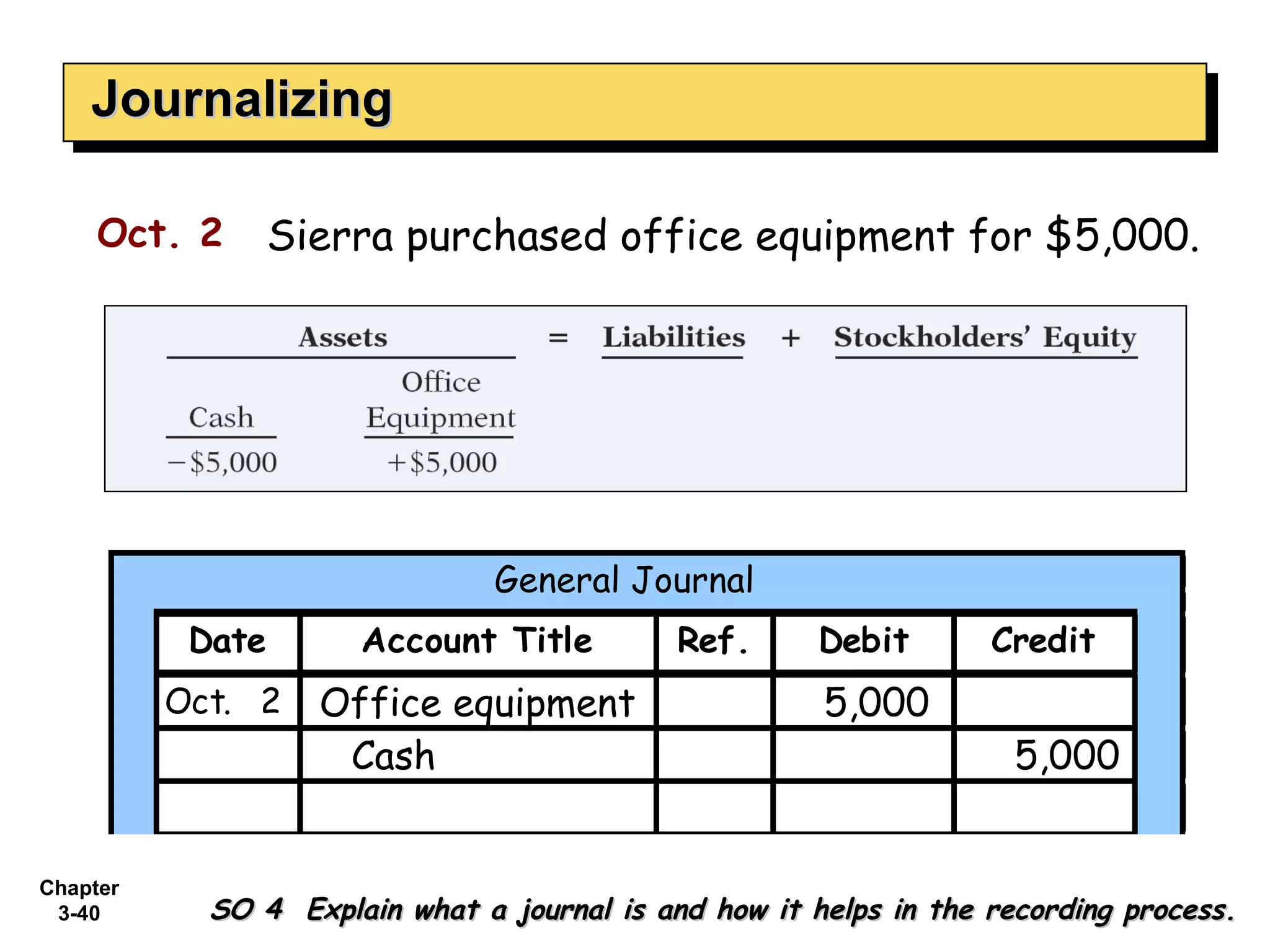

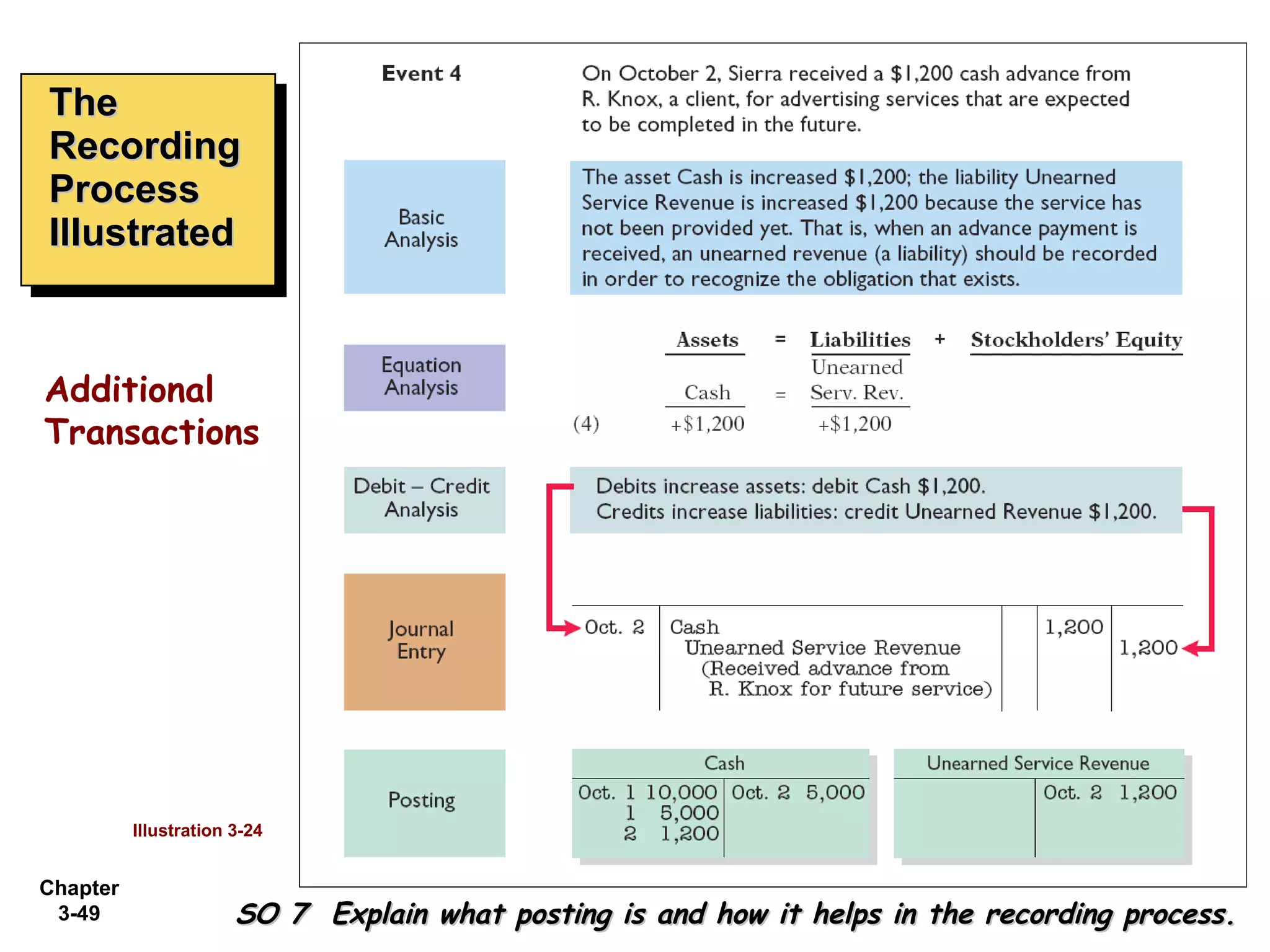

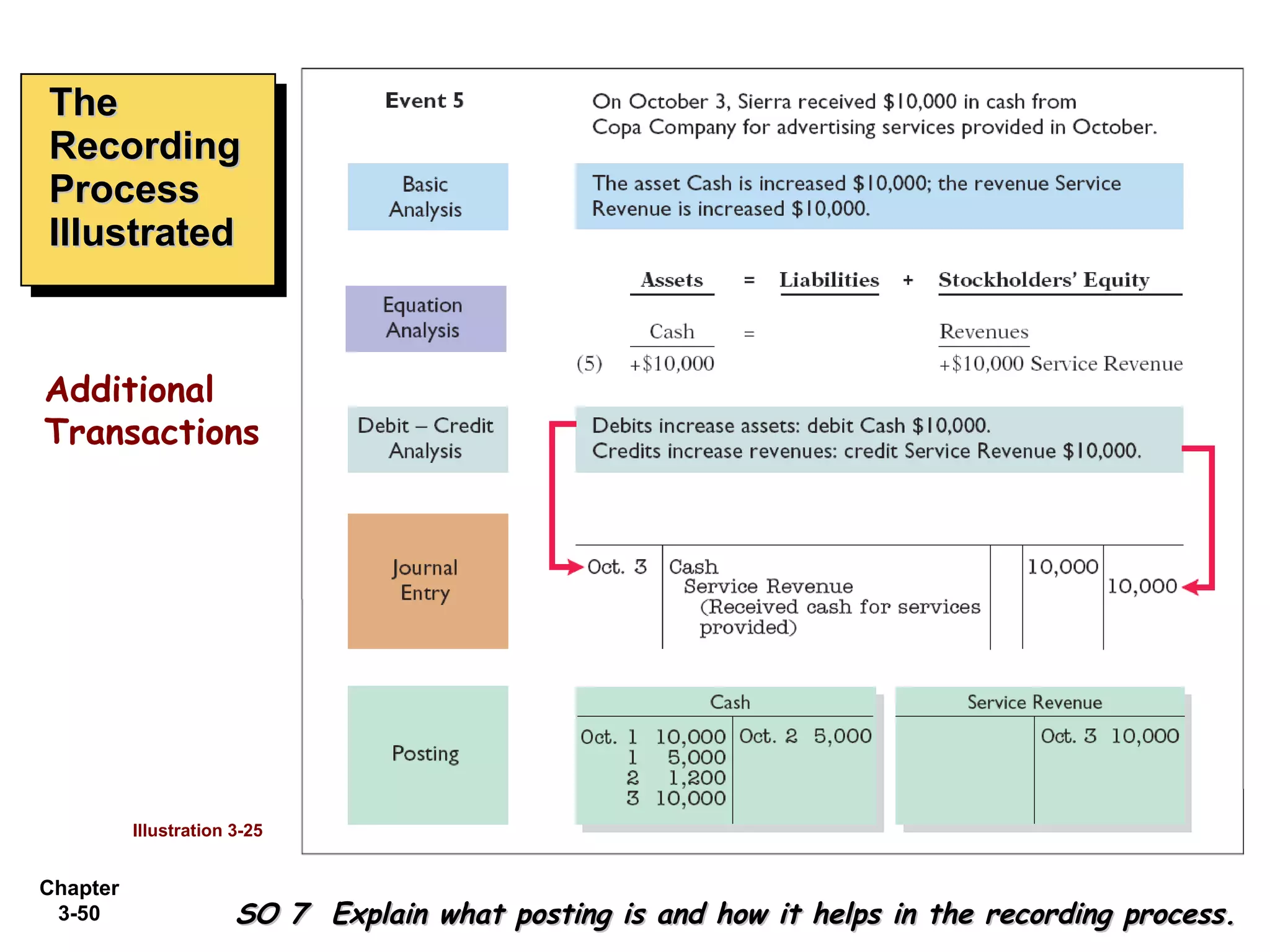

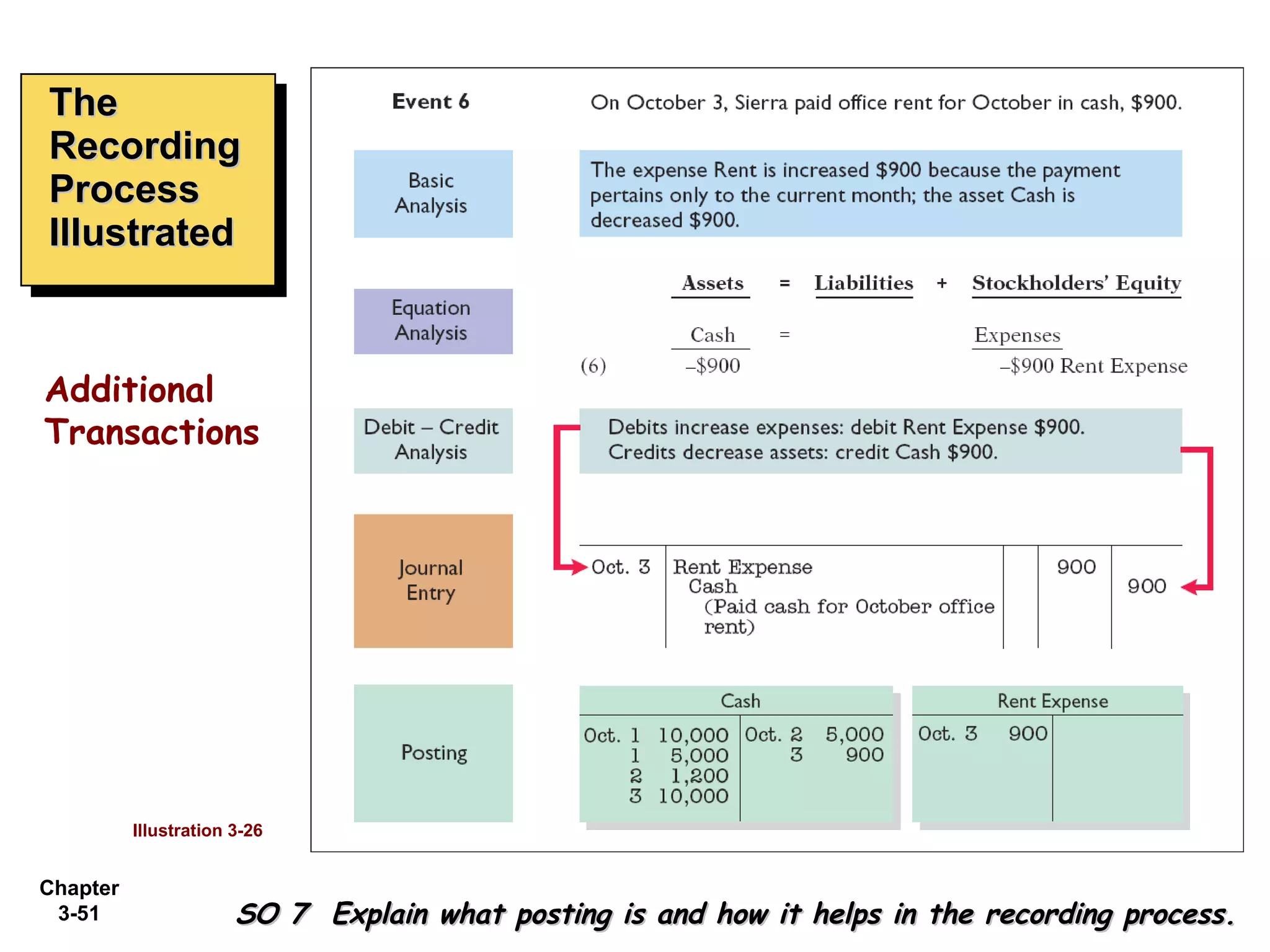

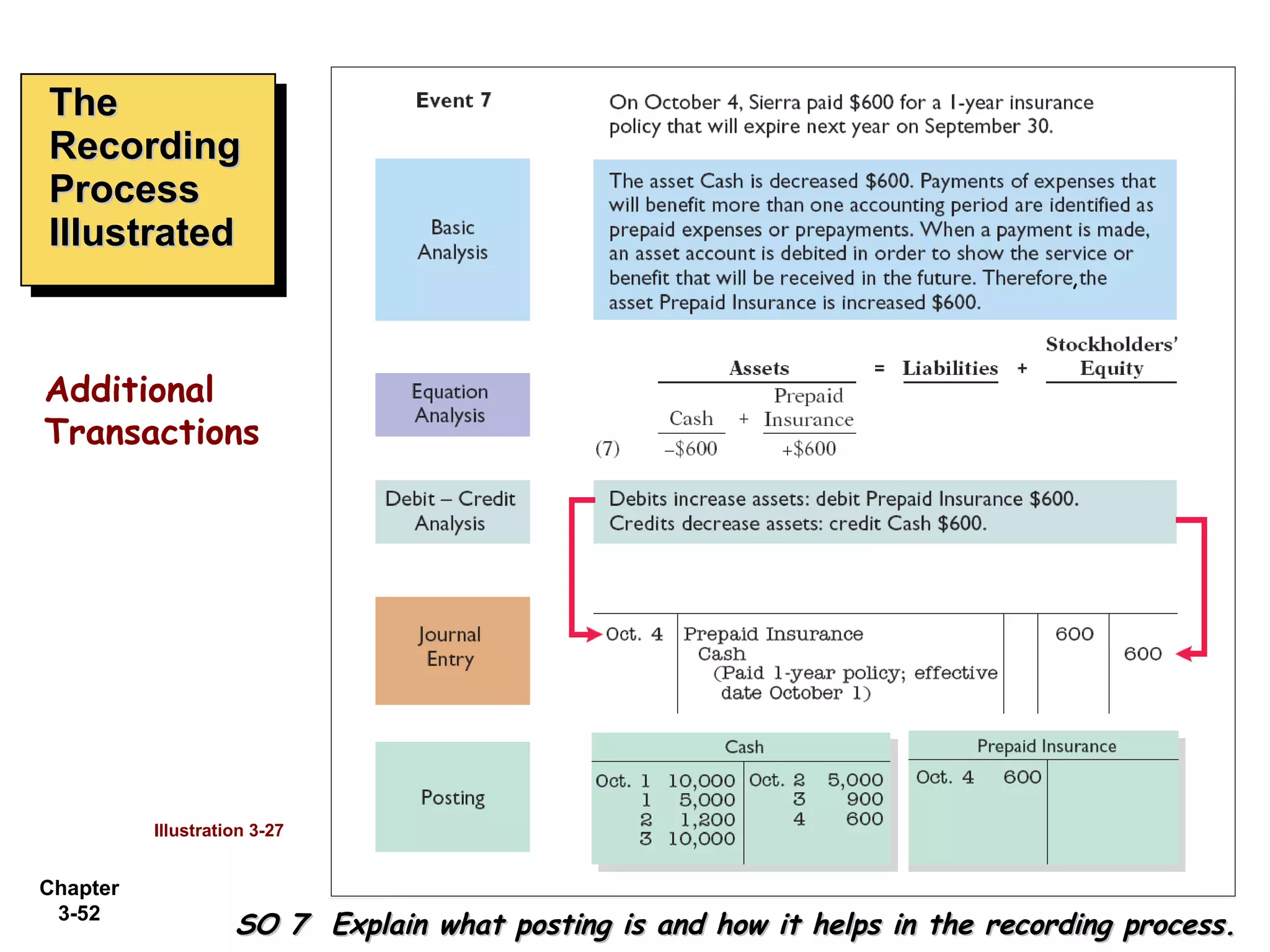

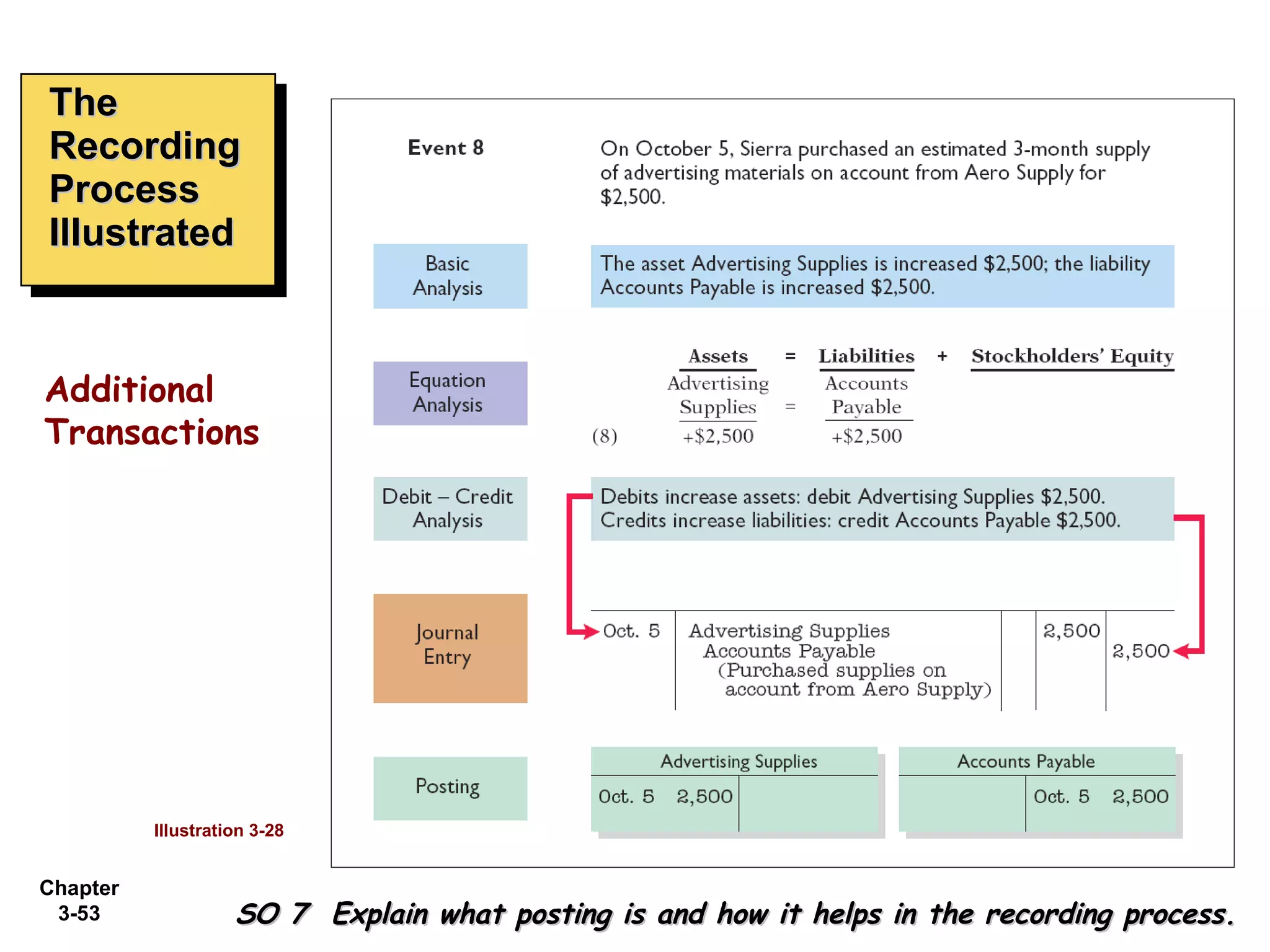

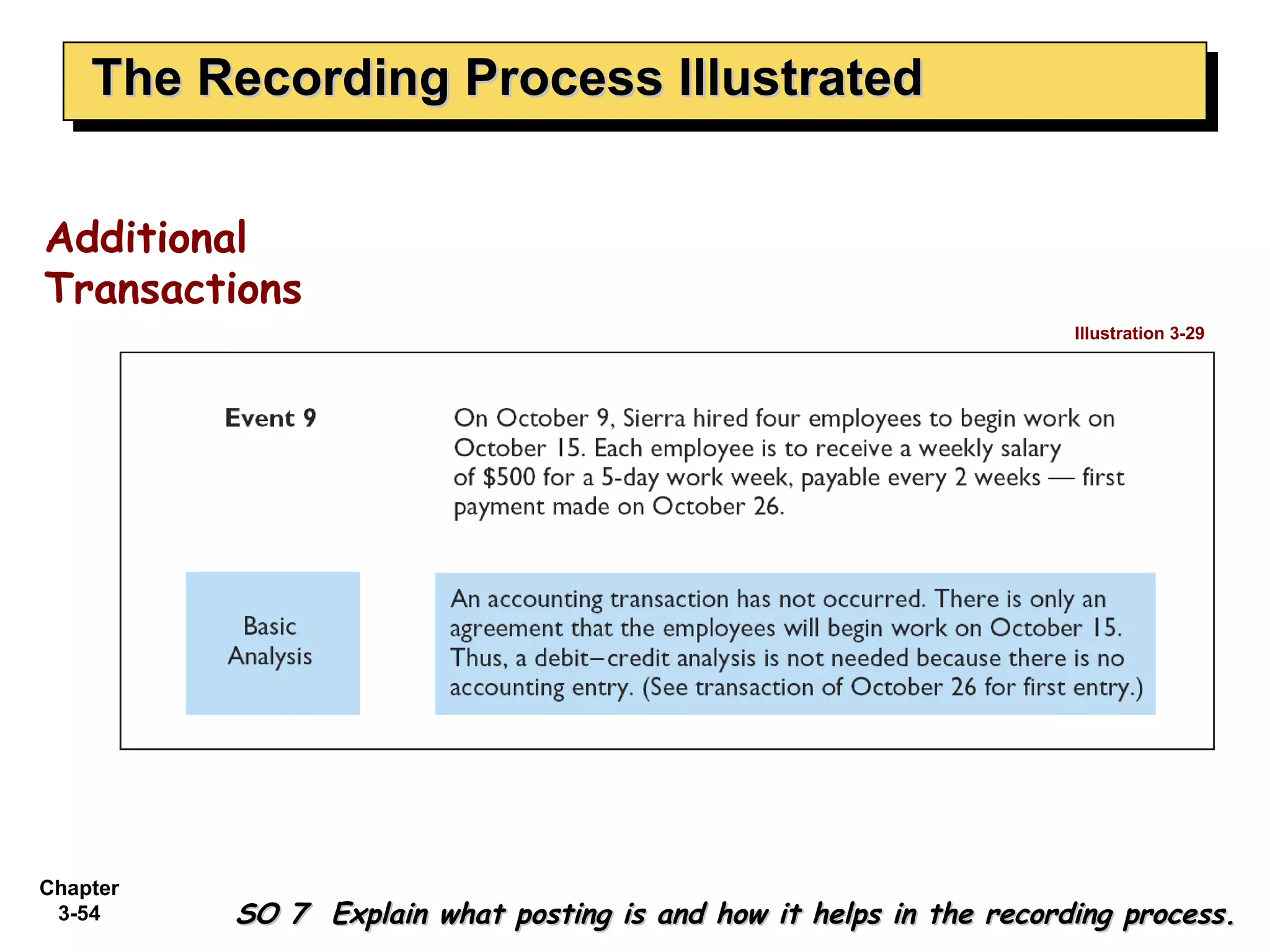

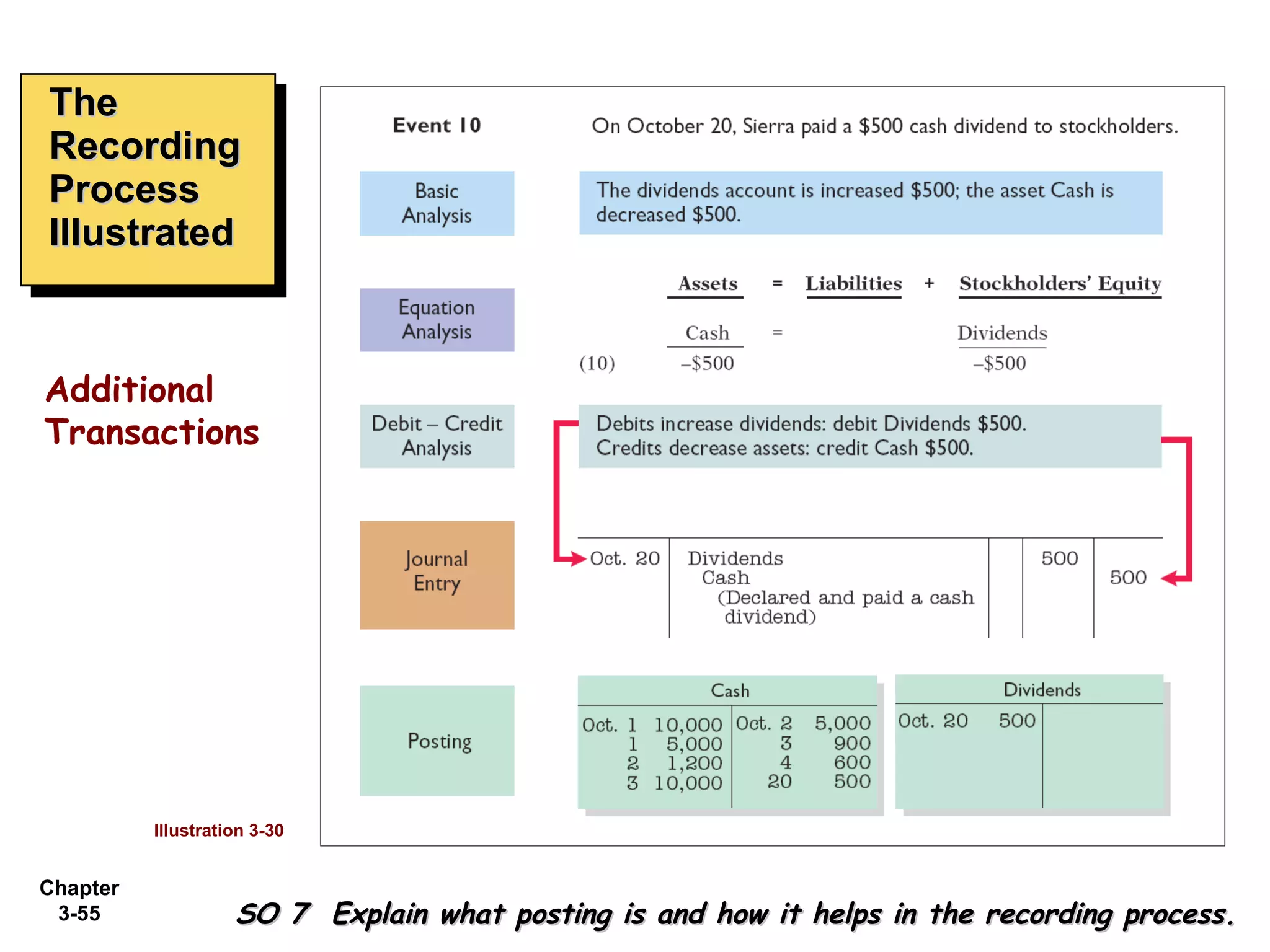

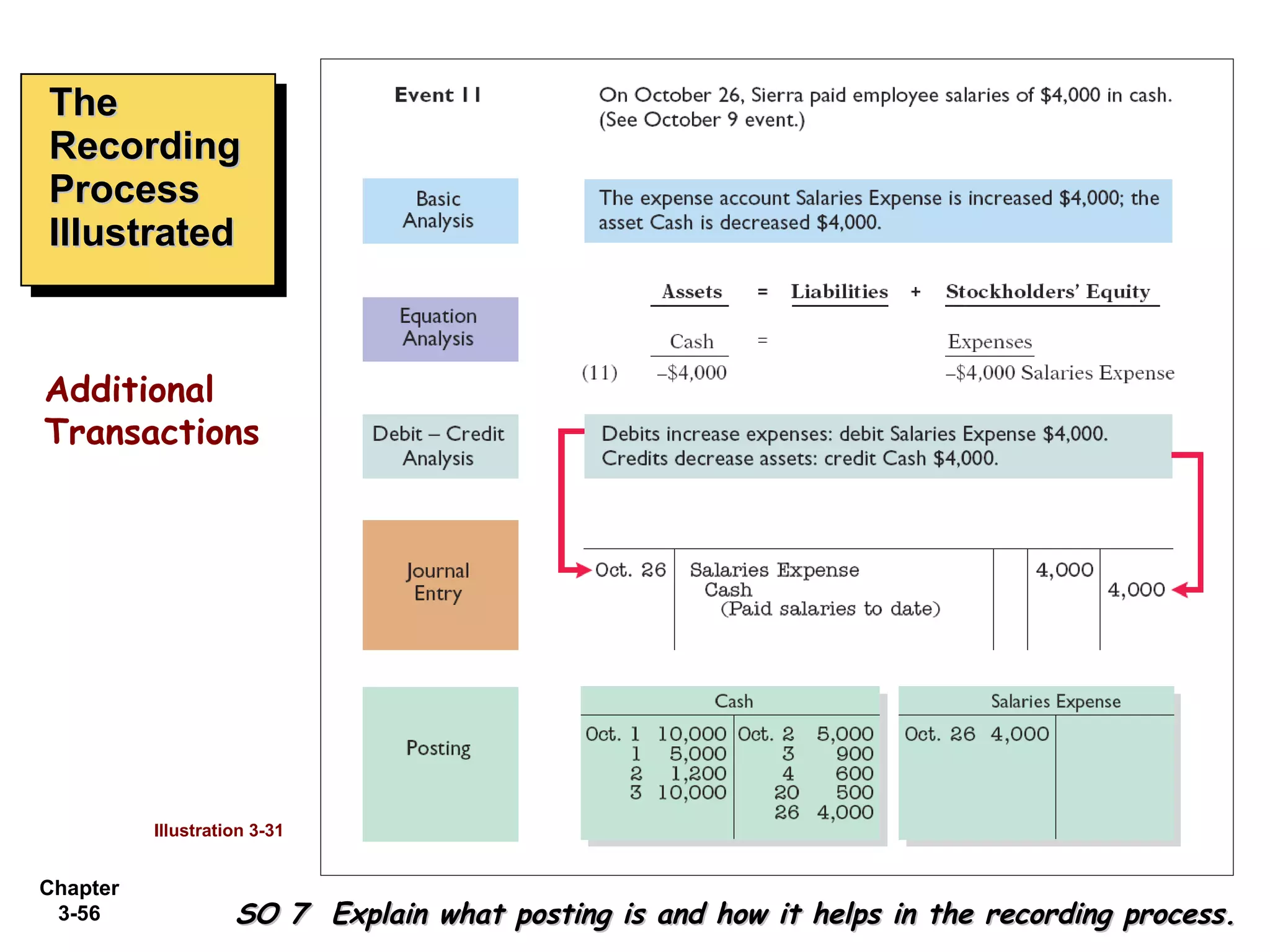

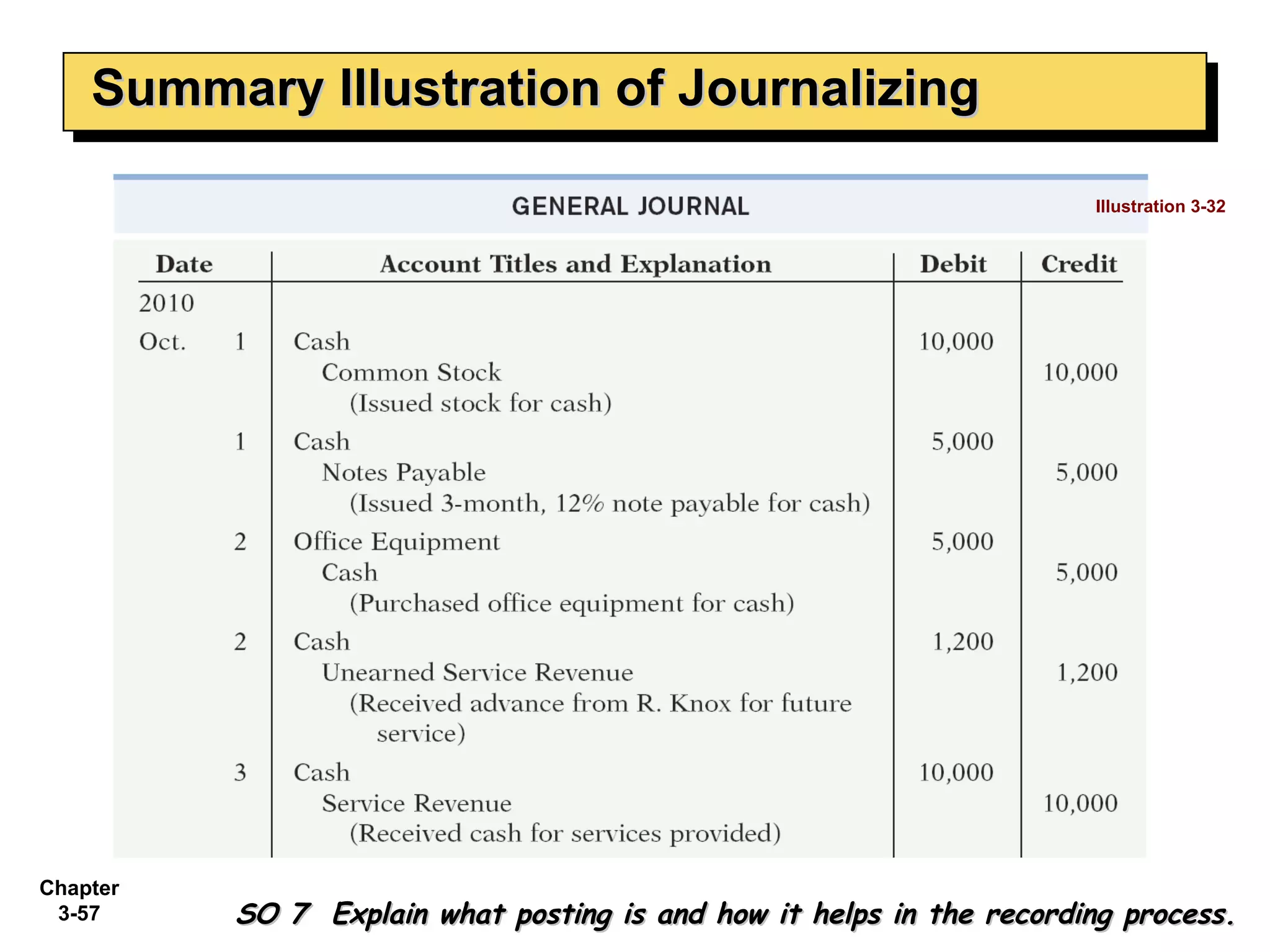

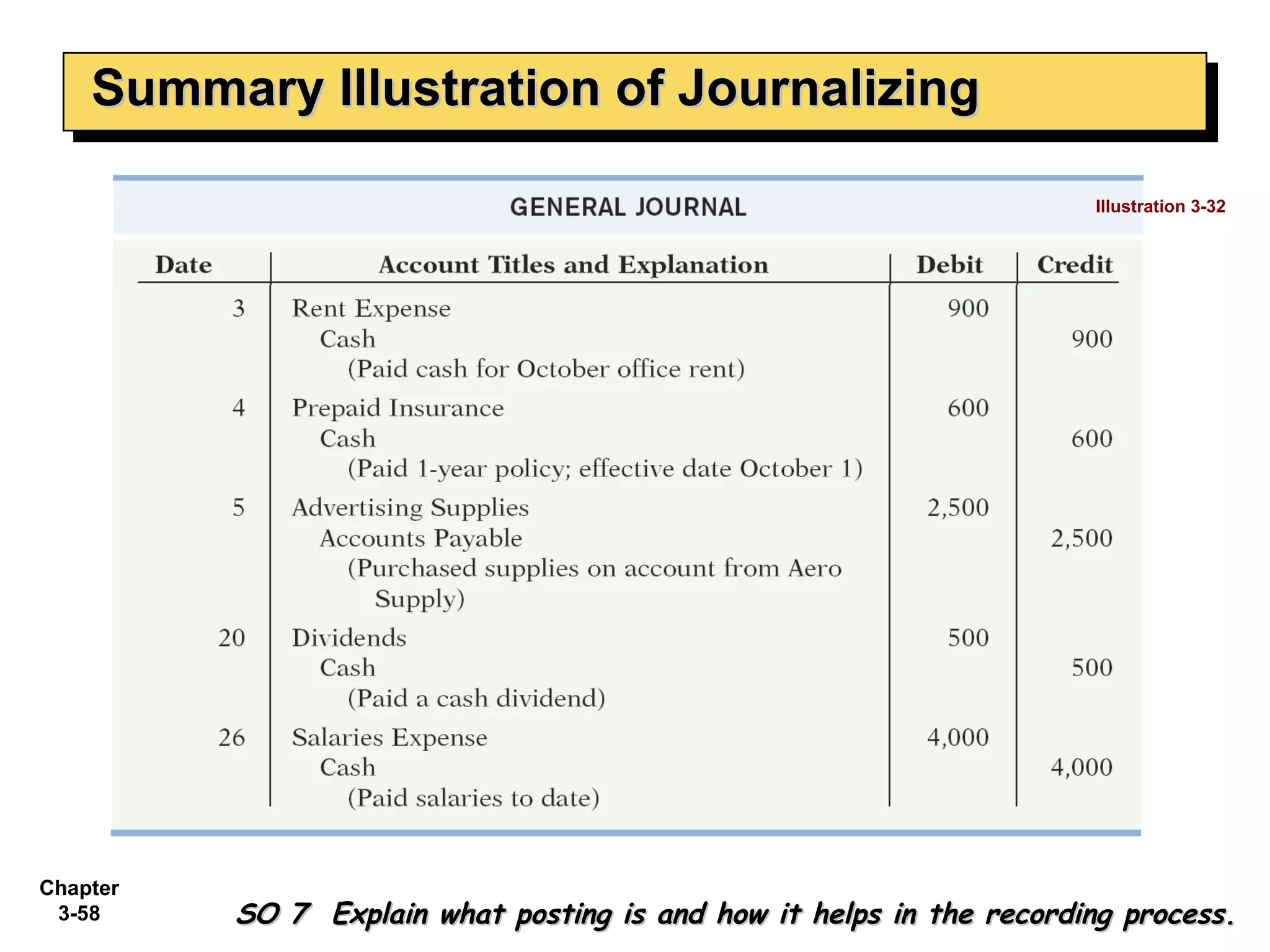

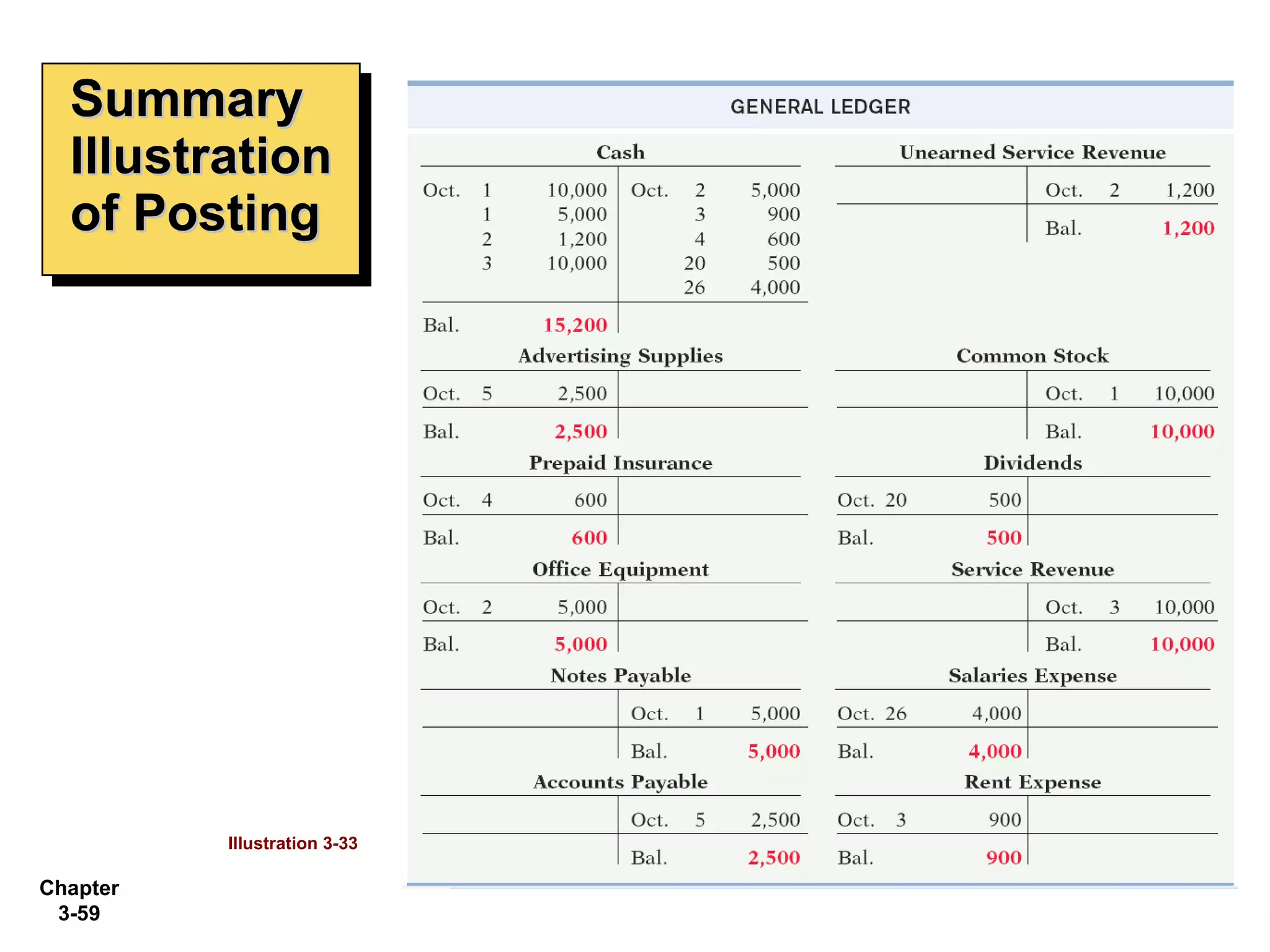

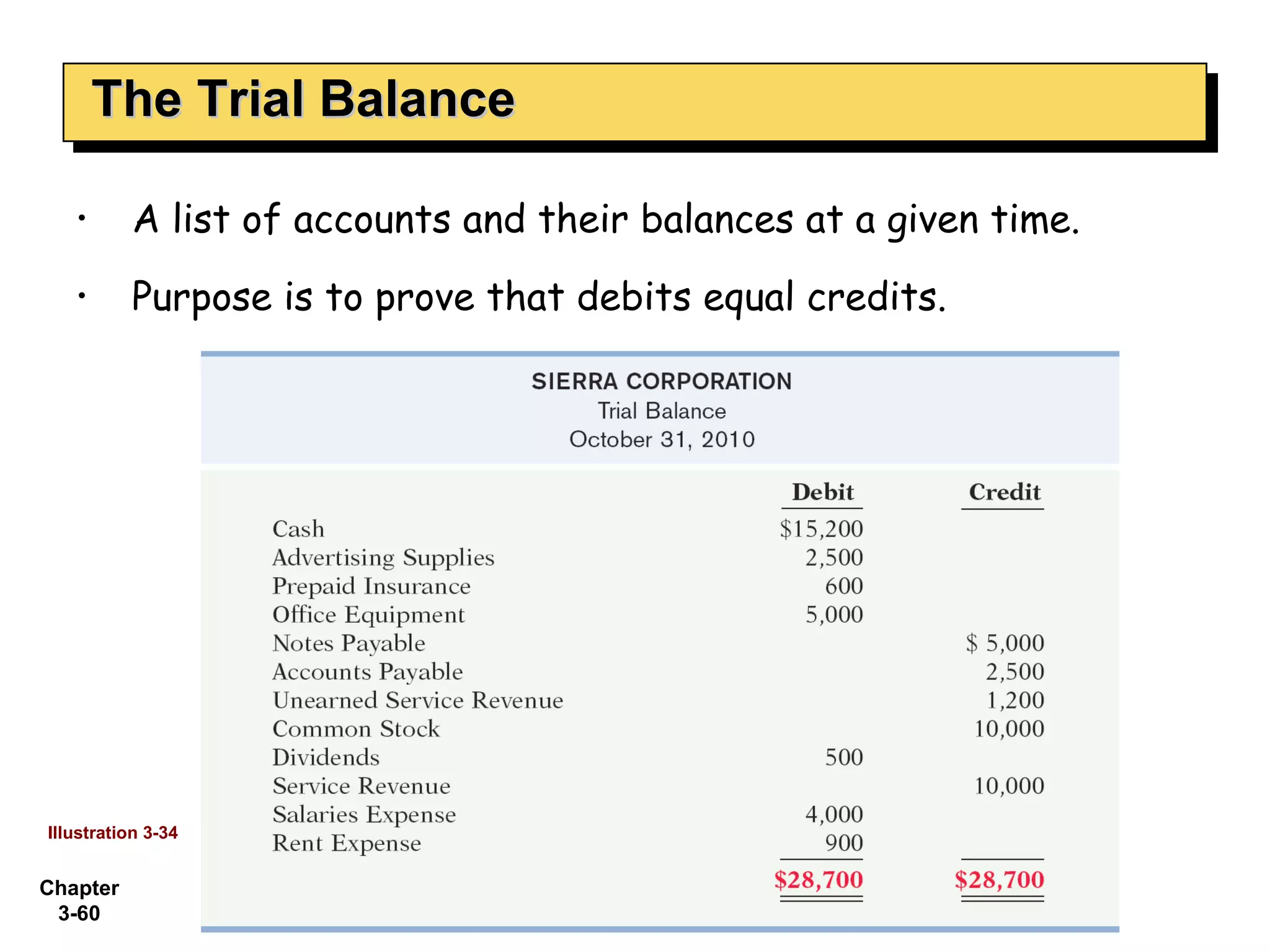

The document discusses key concepts in the accounting information system including:

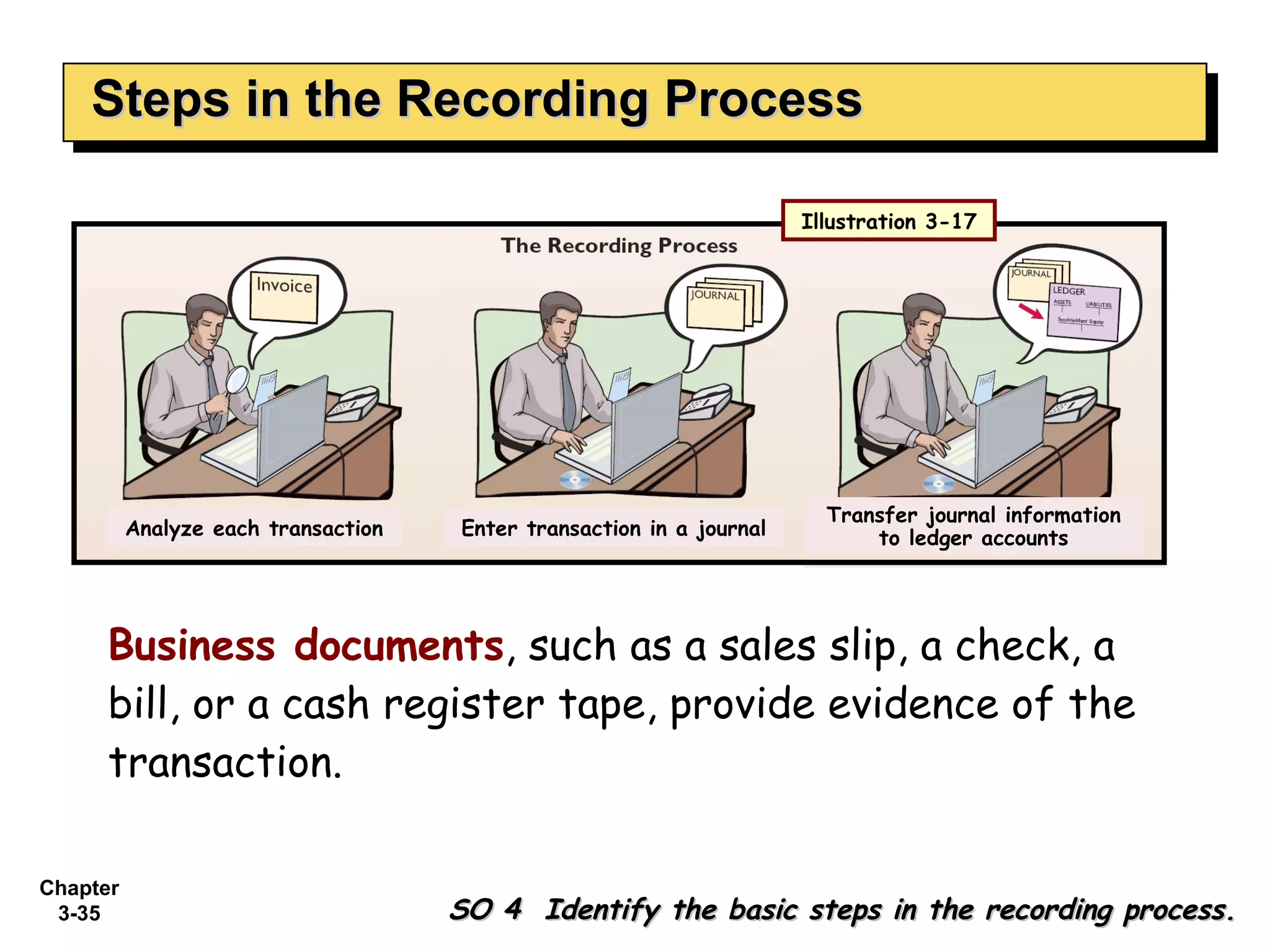

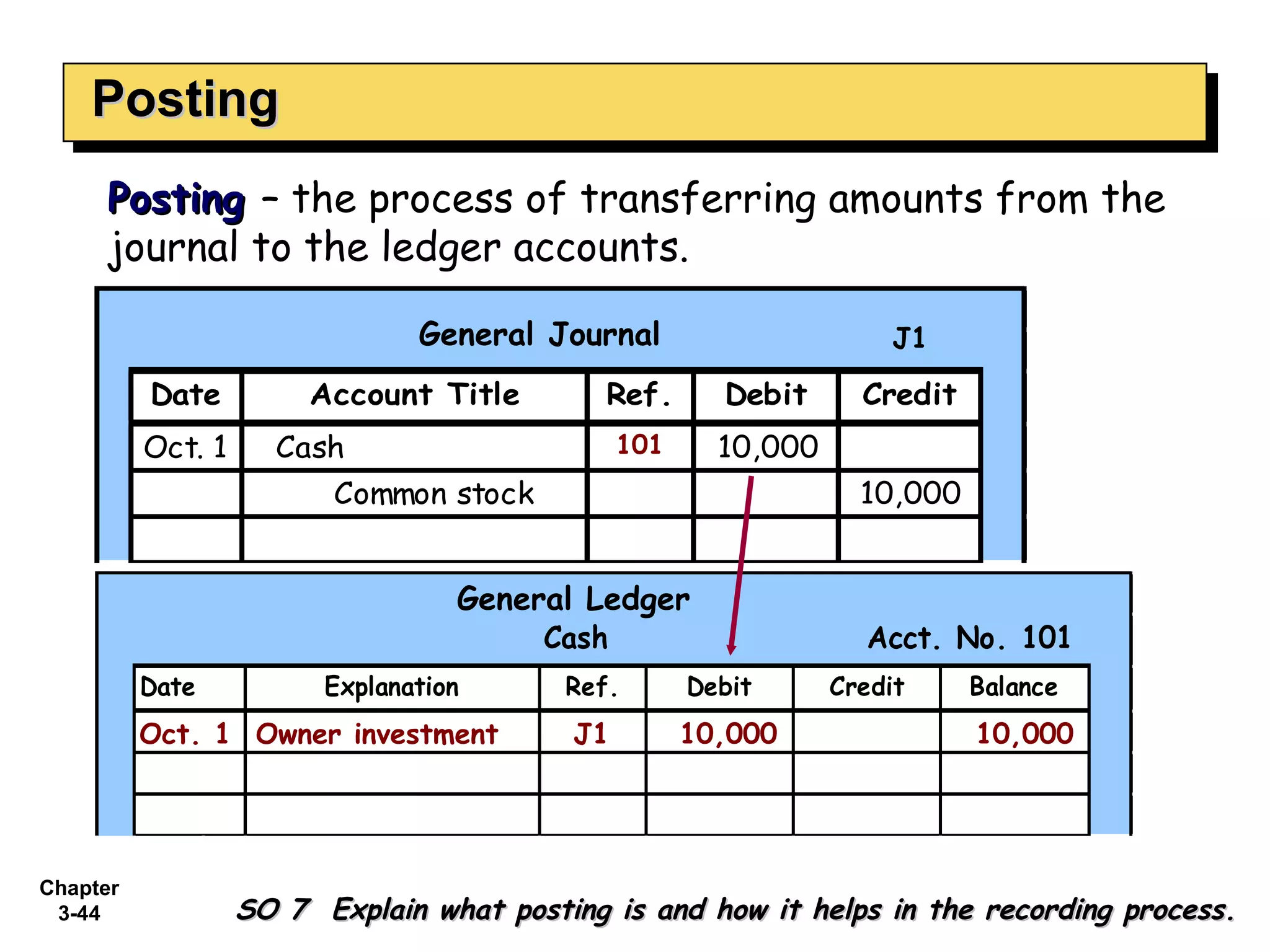

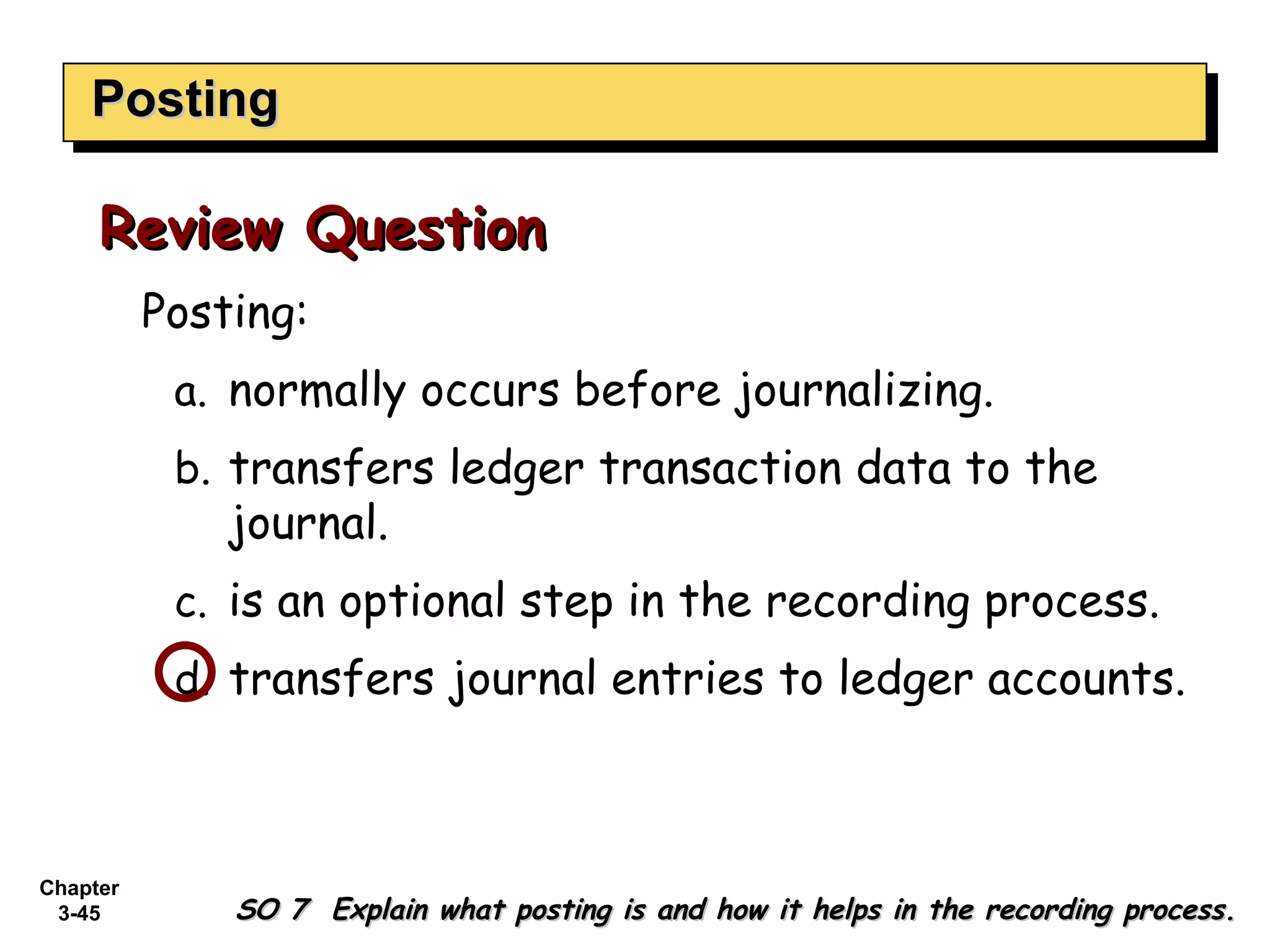

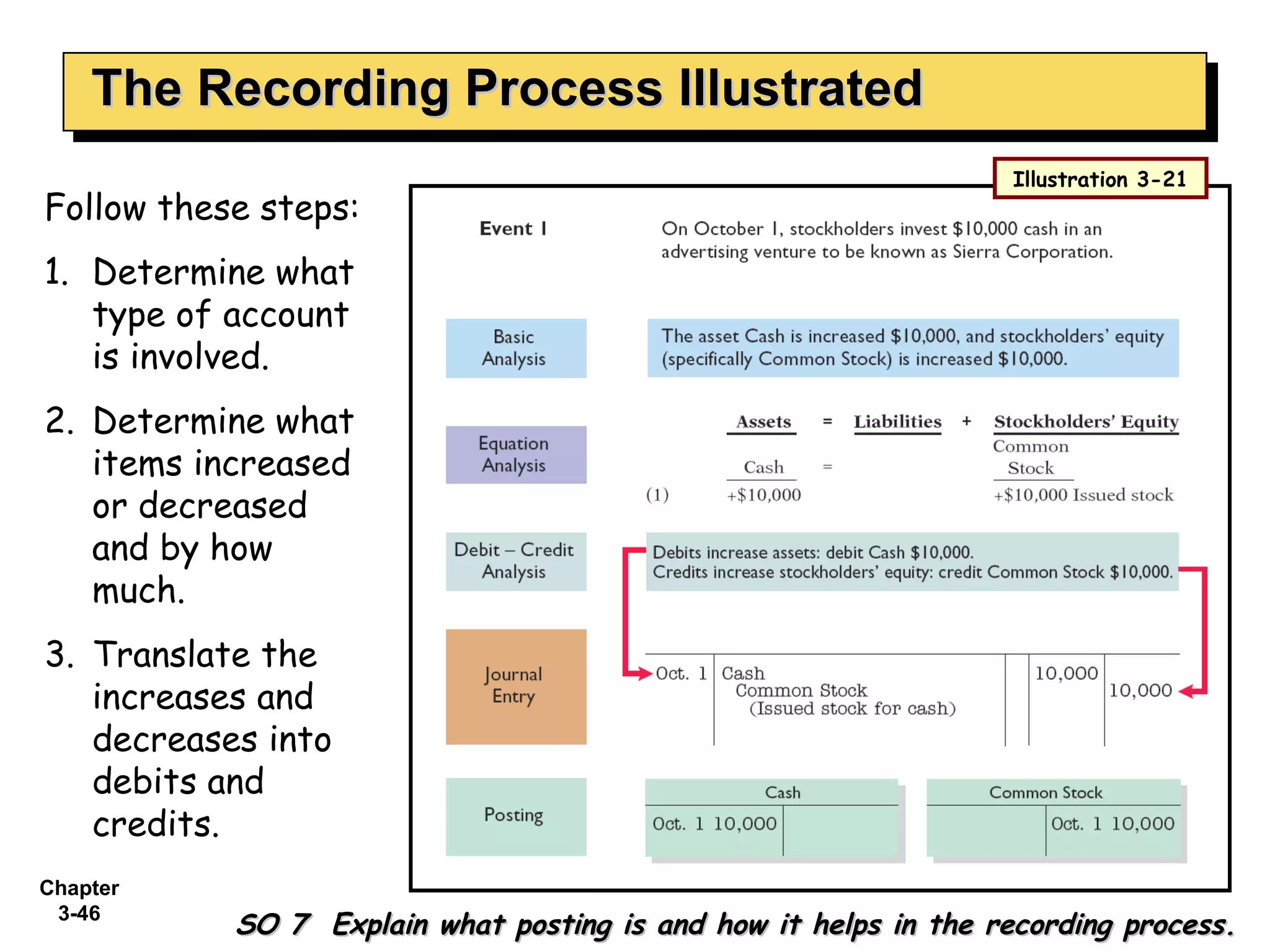

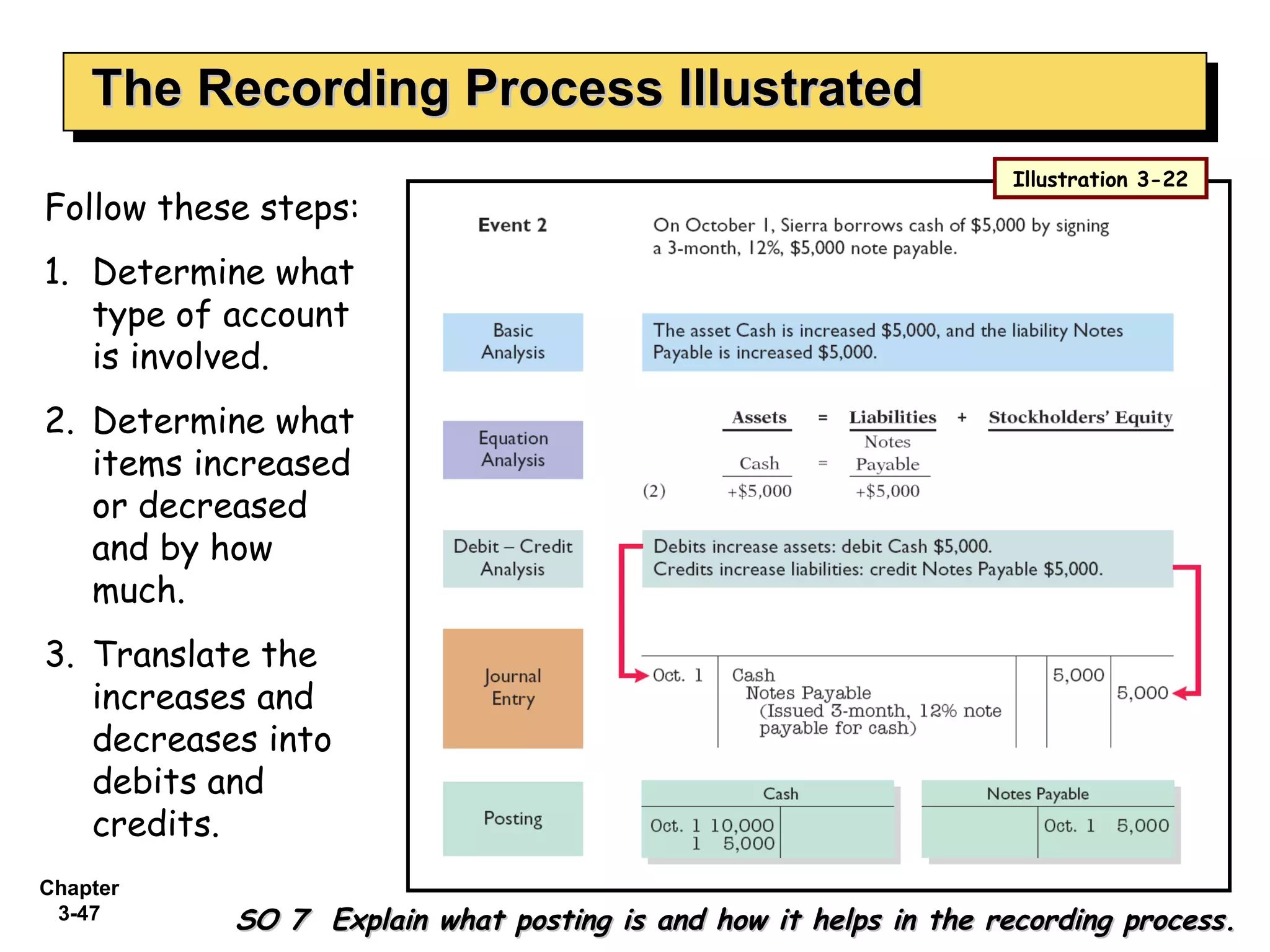

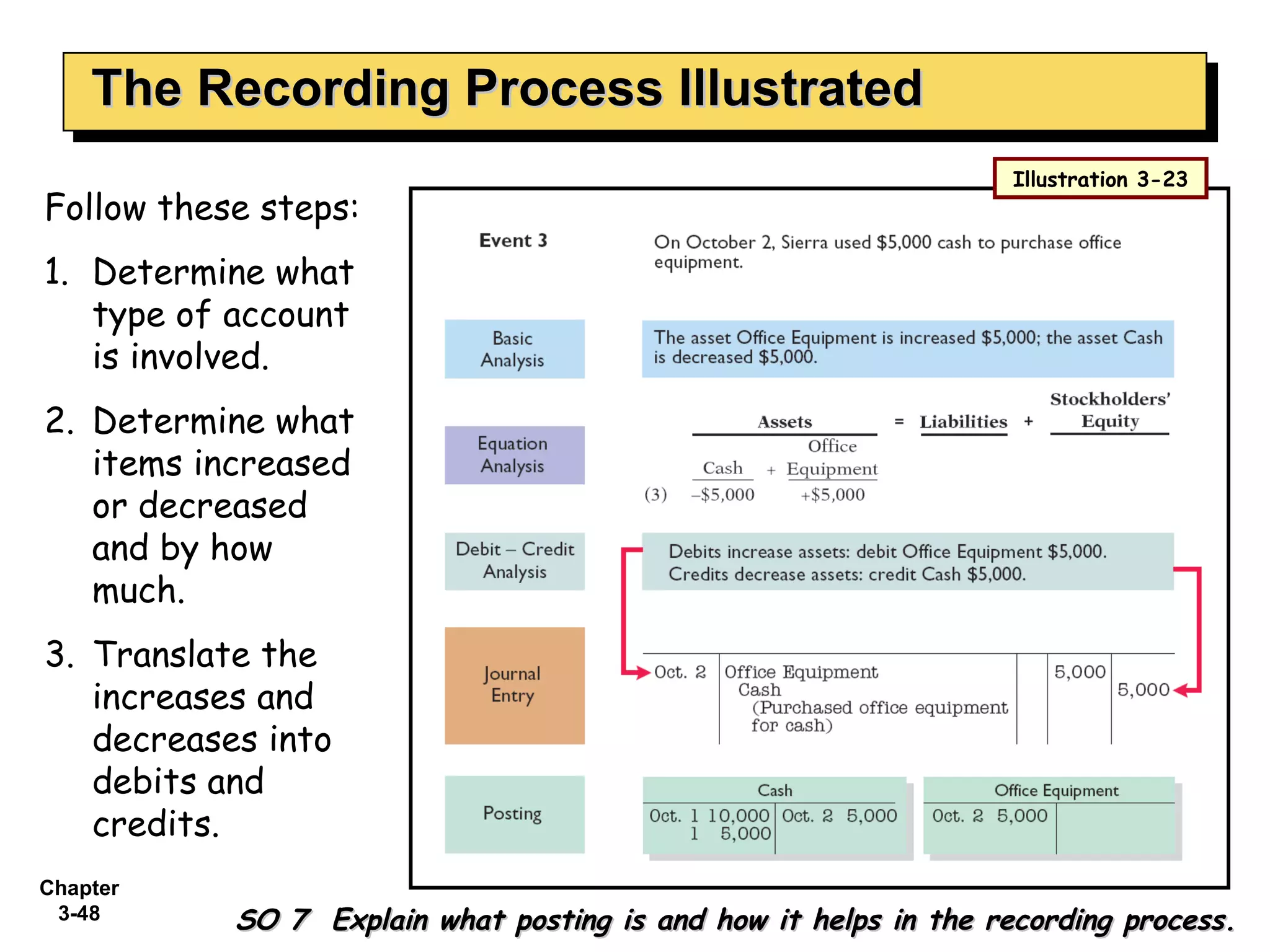

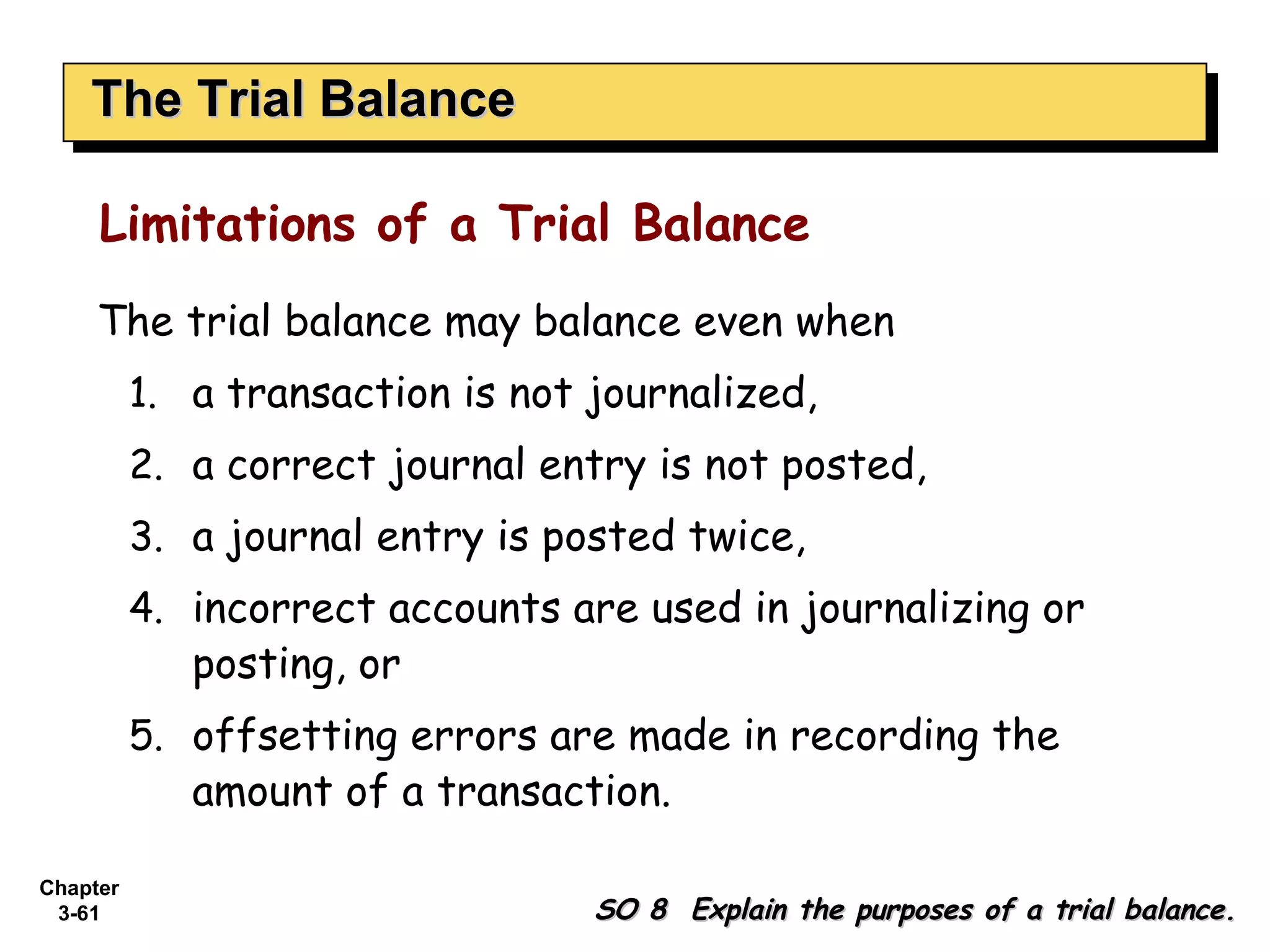

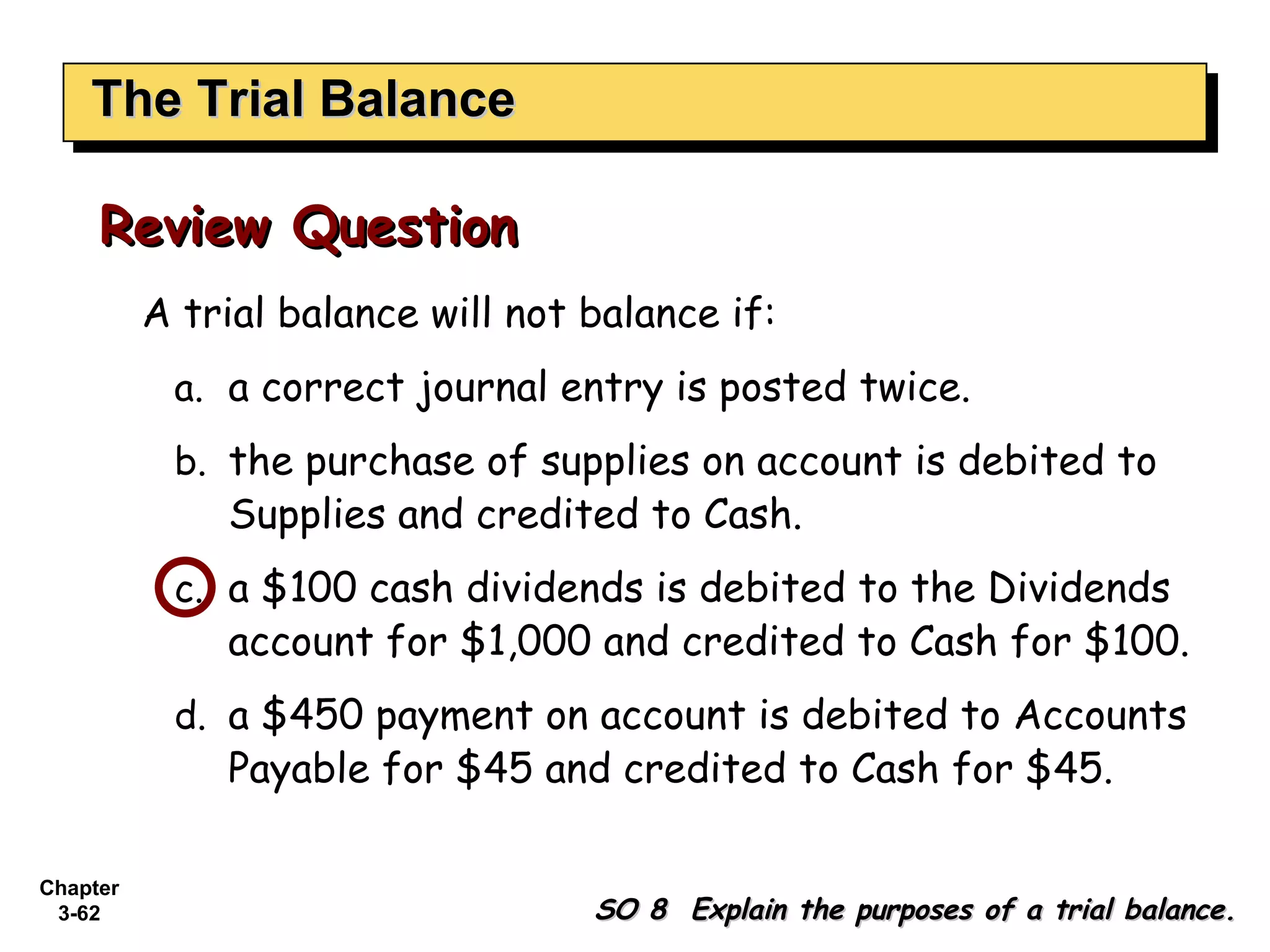

1) The basic steps in the recording process such as analyzing transactions, journalizing, posting to ledger accounts, and preparing a trial balance.

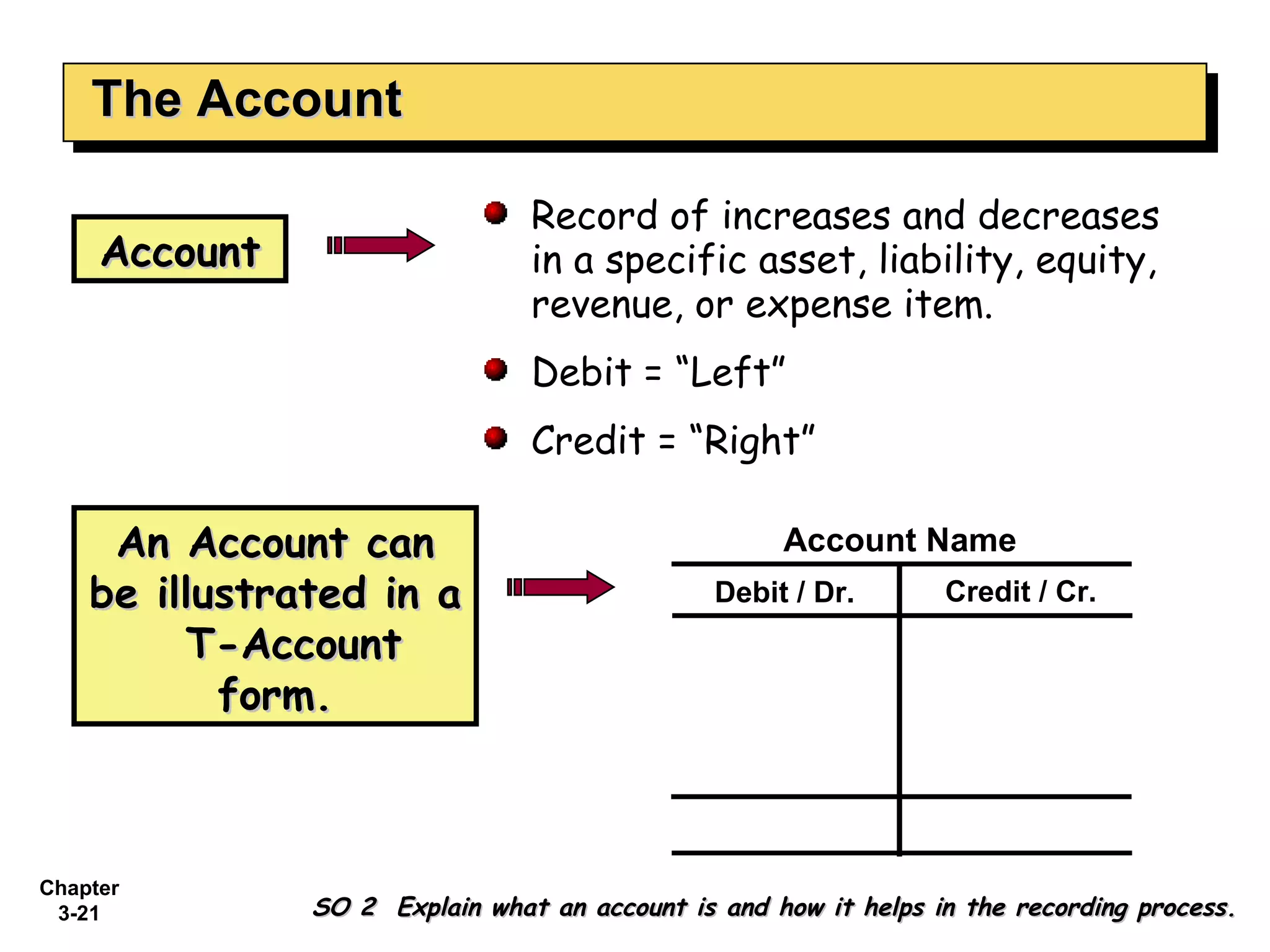

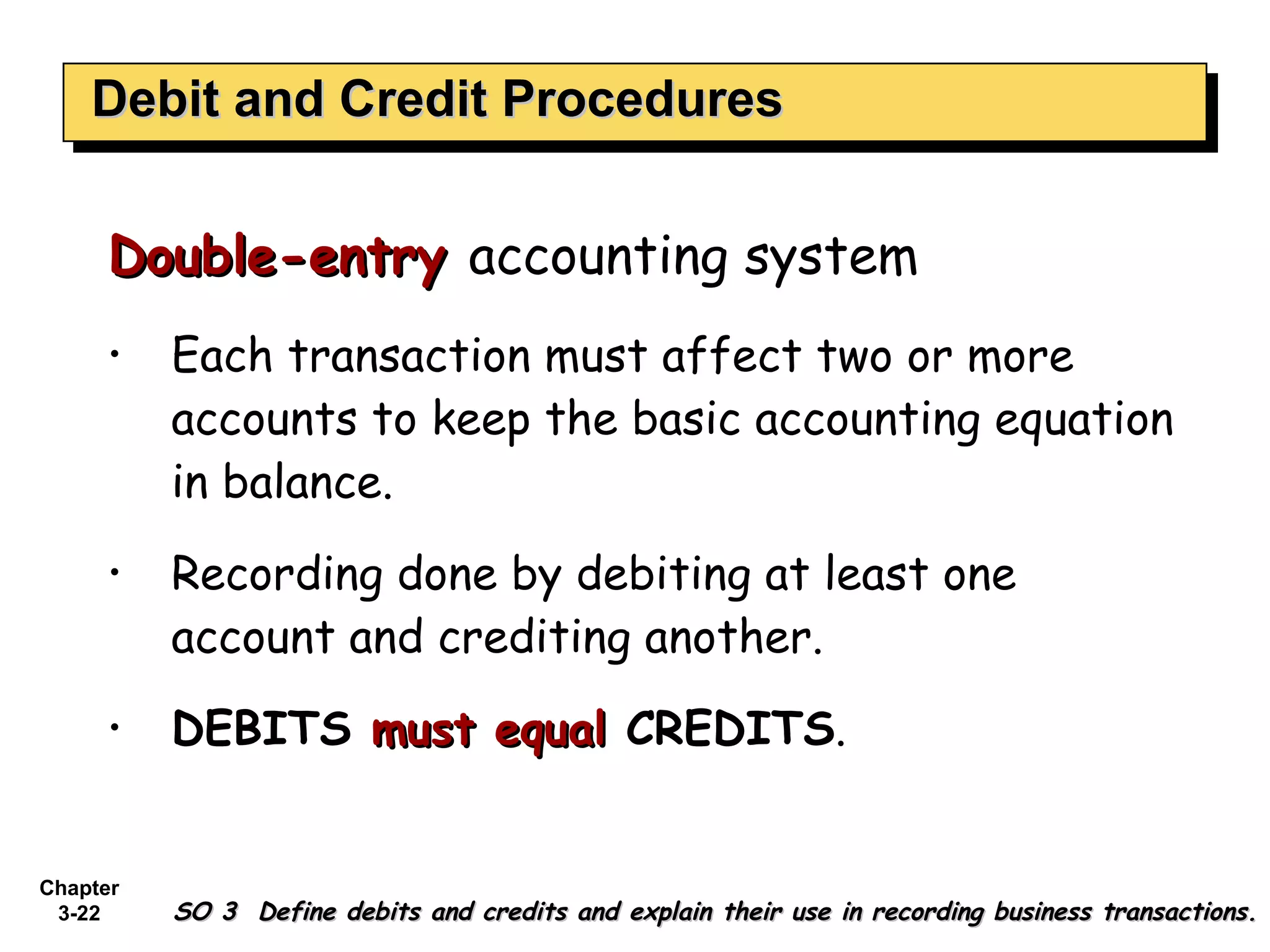

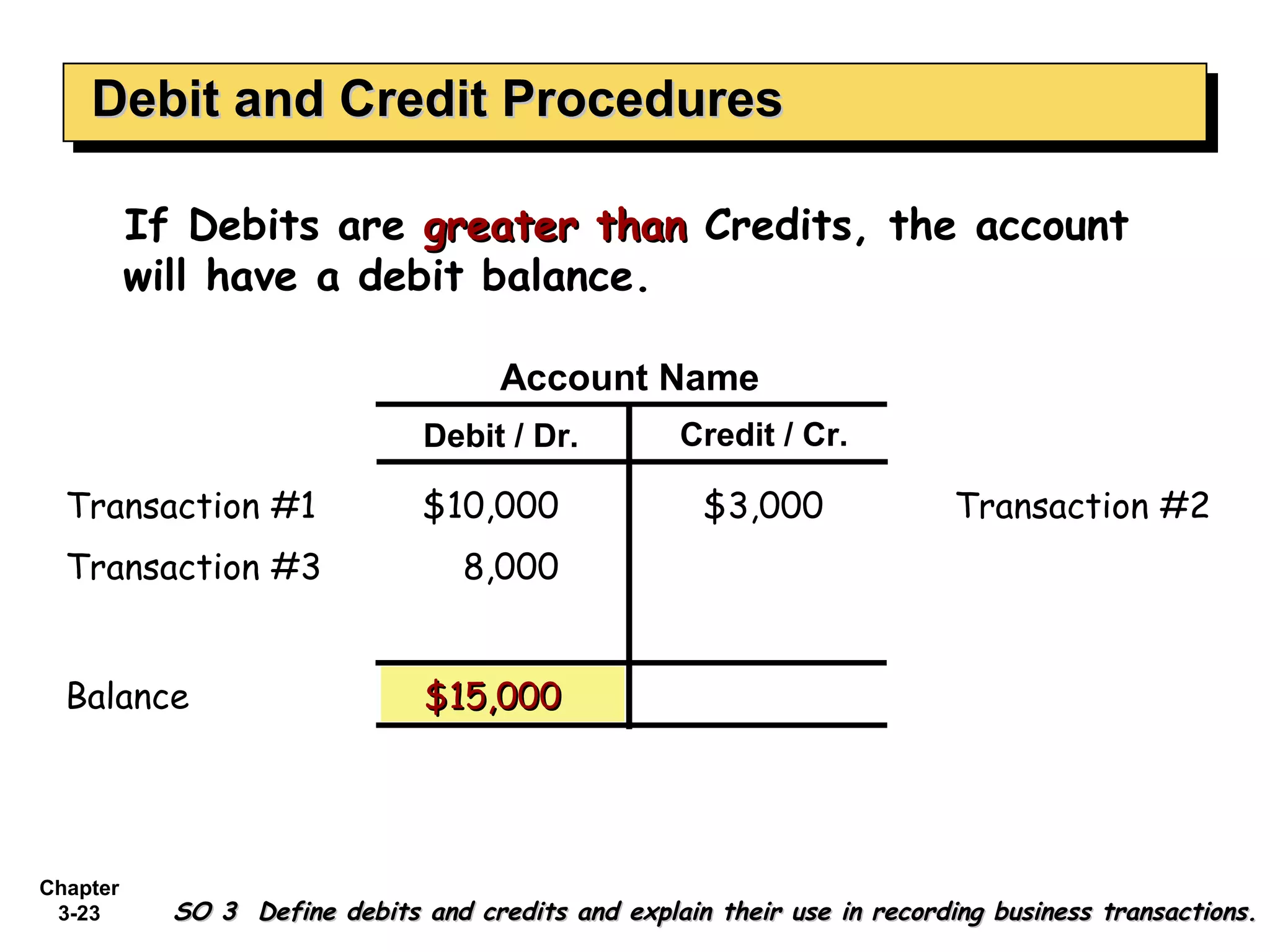

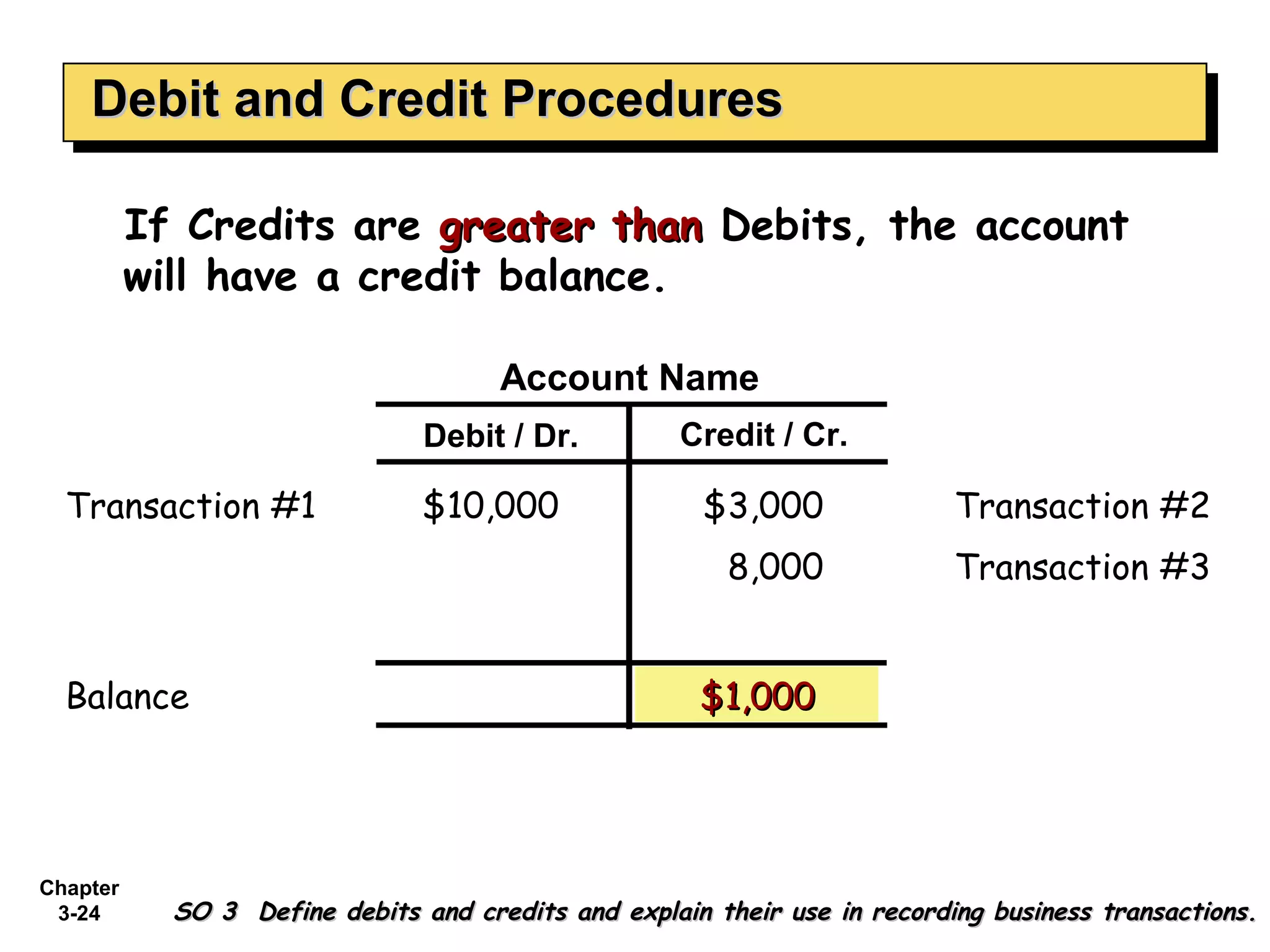

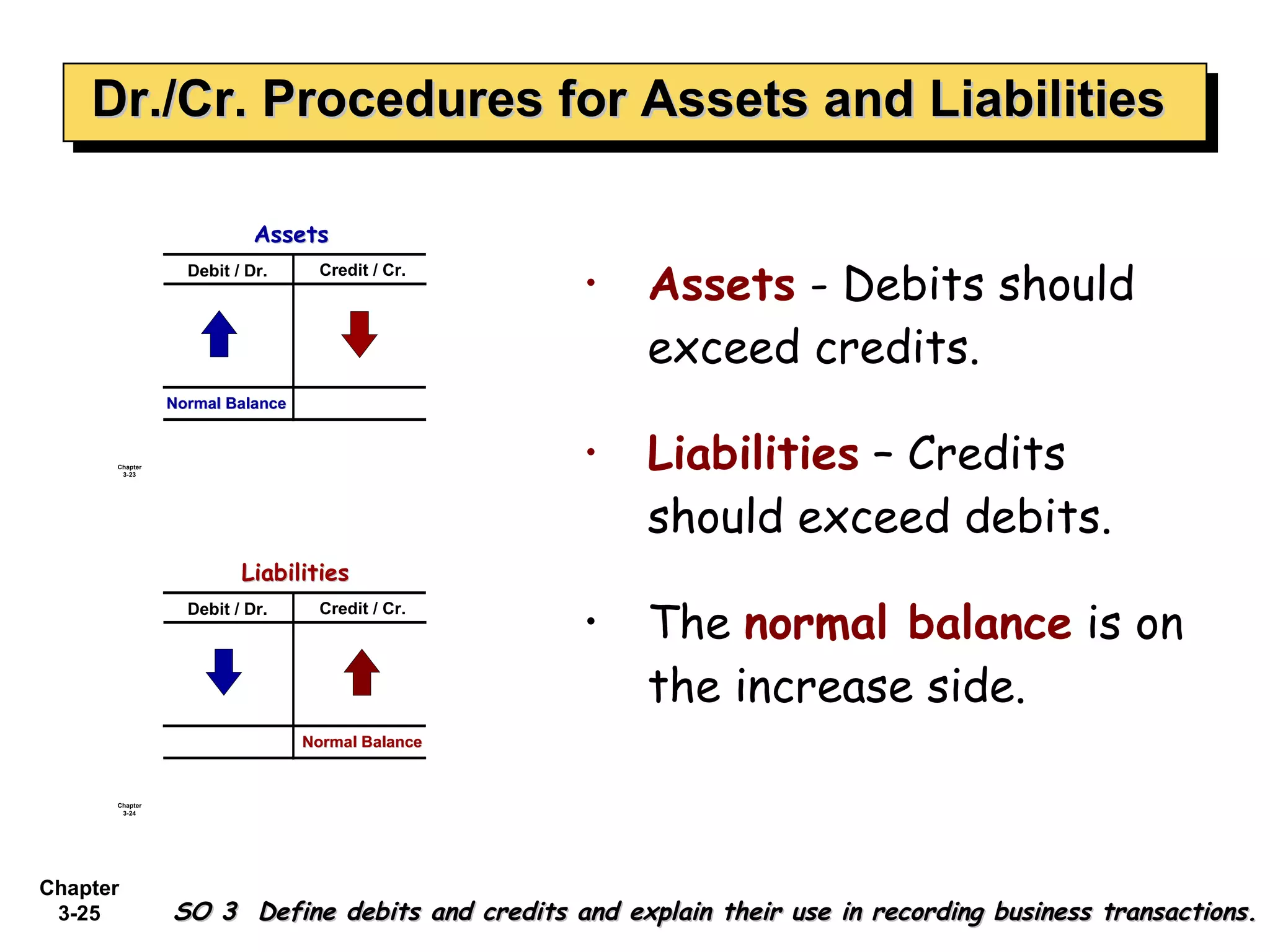

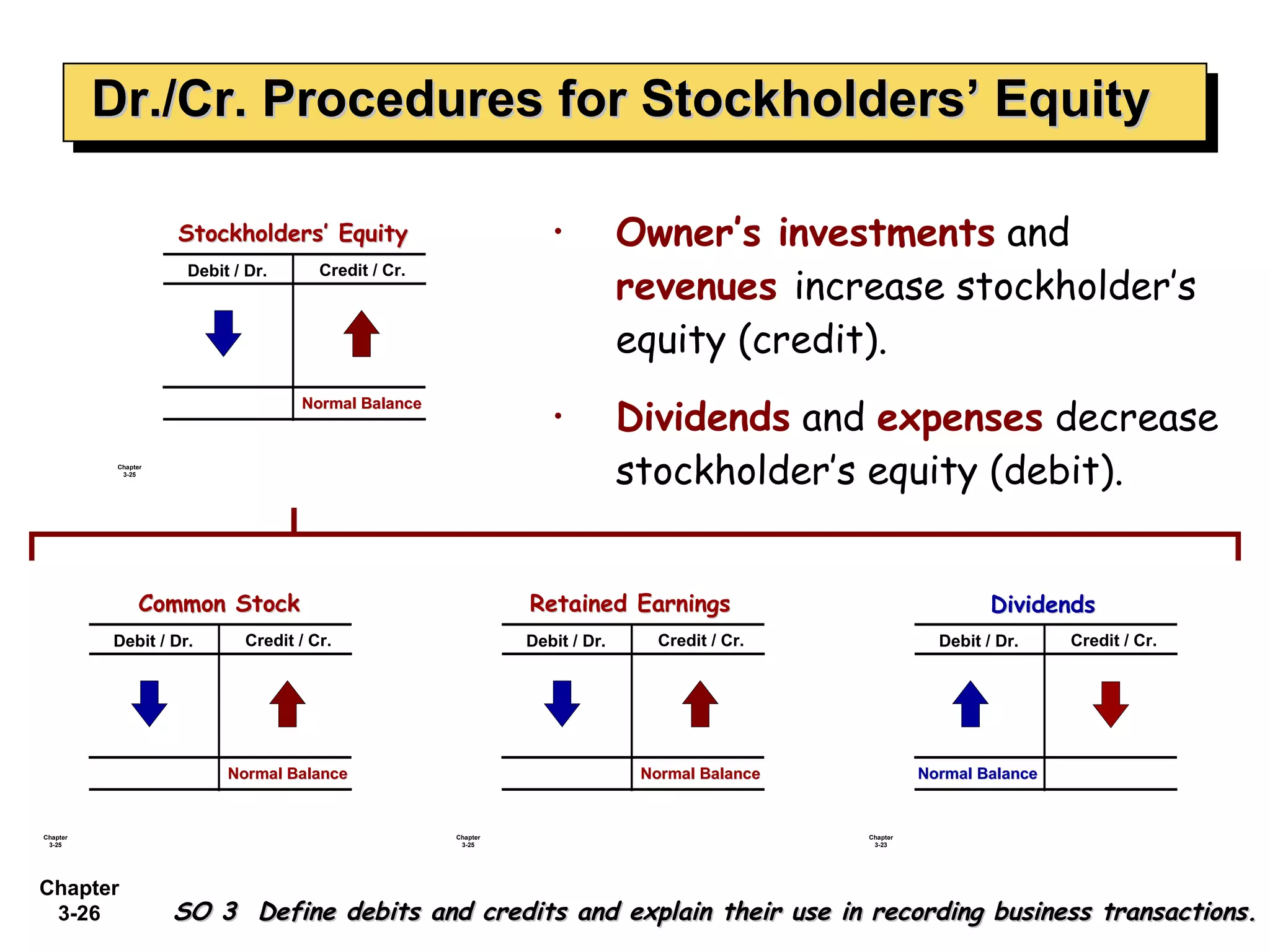

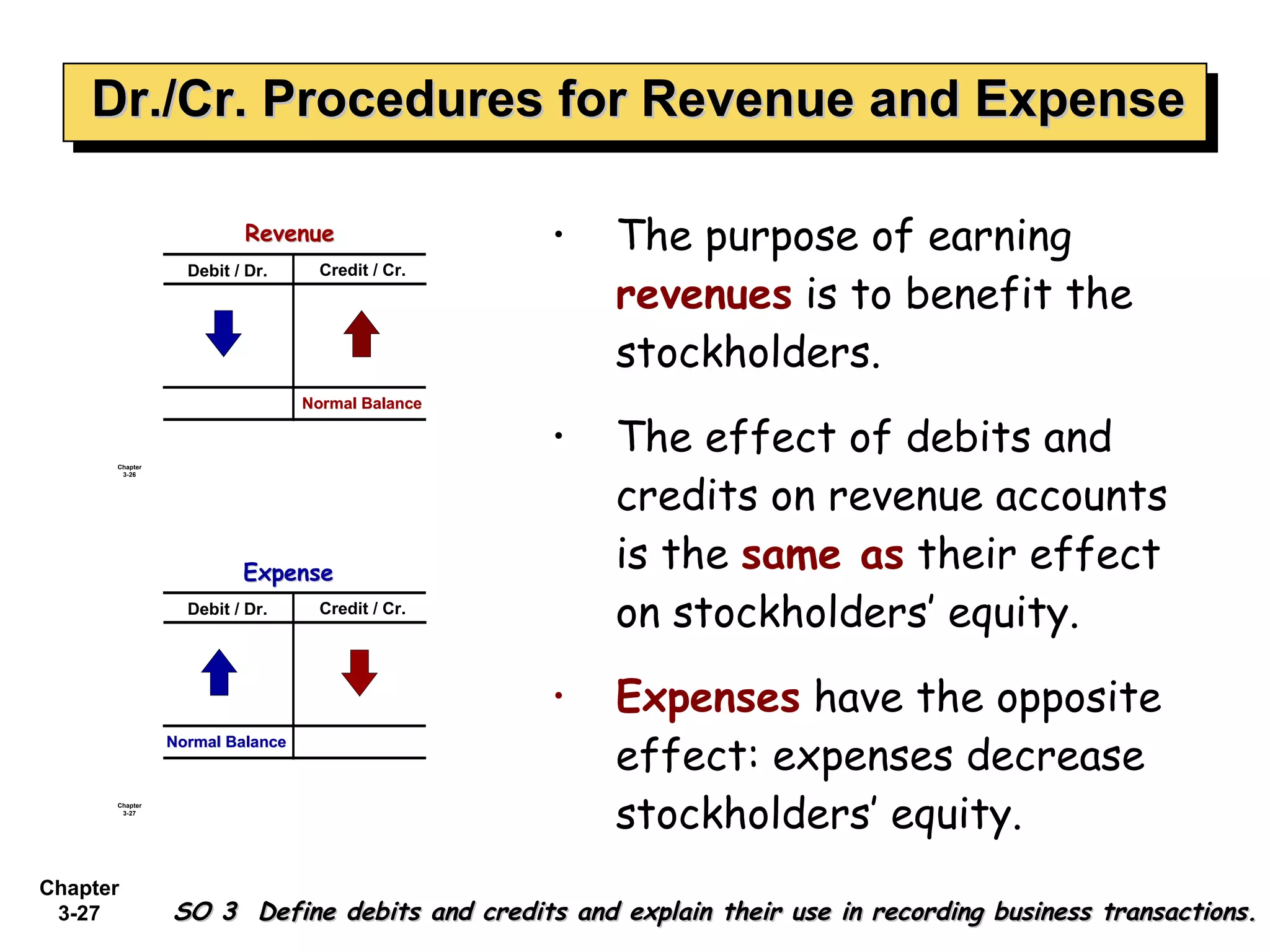

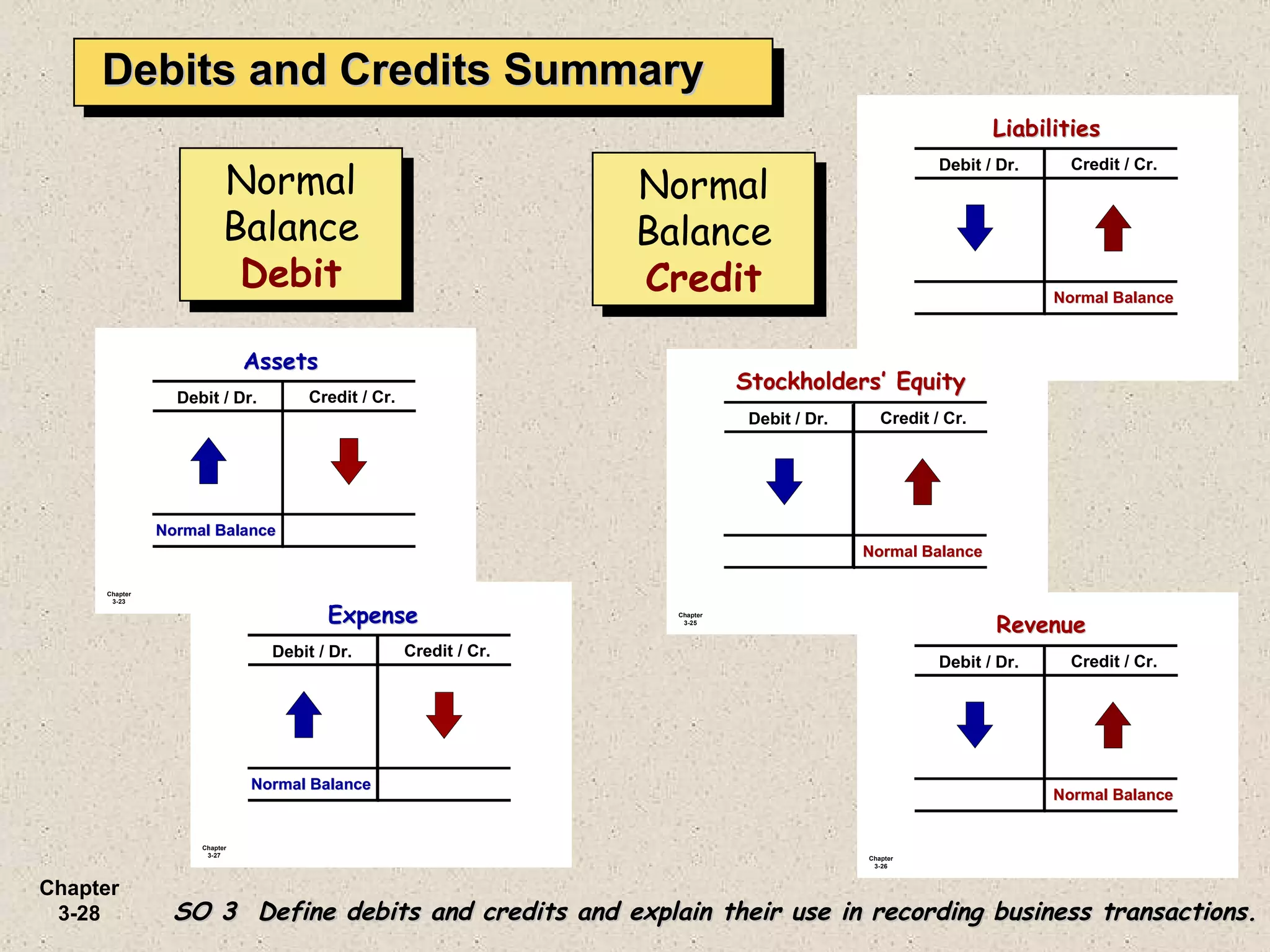

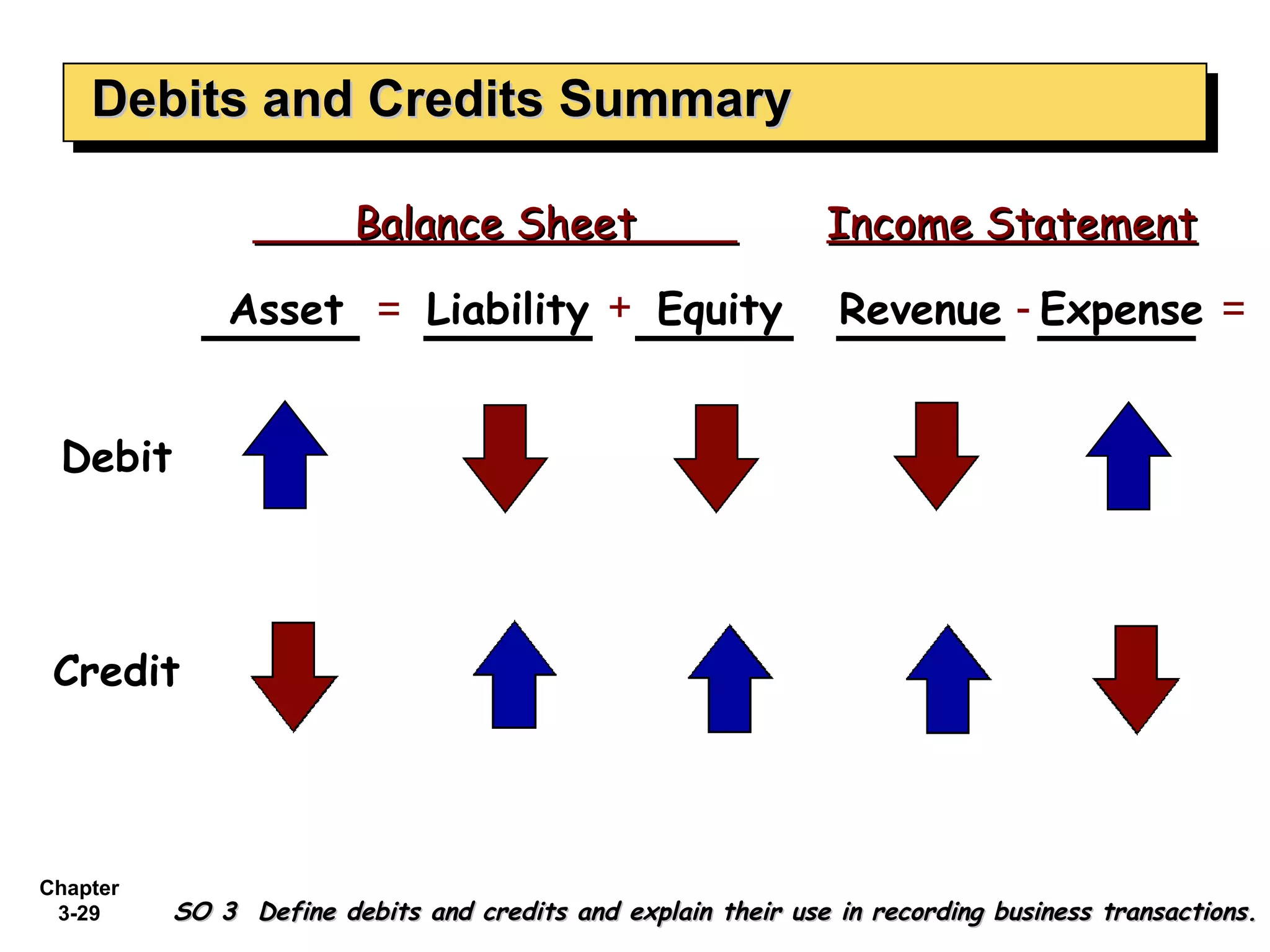

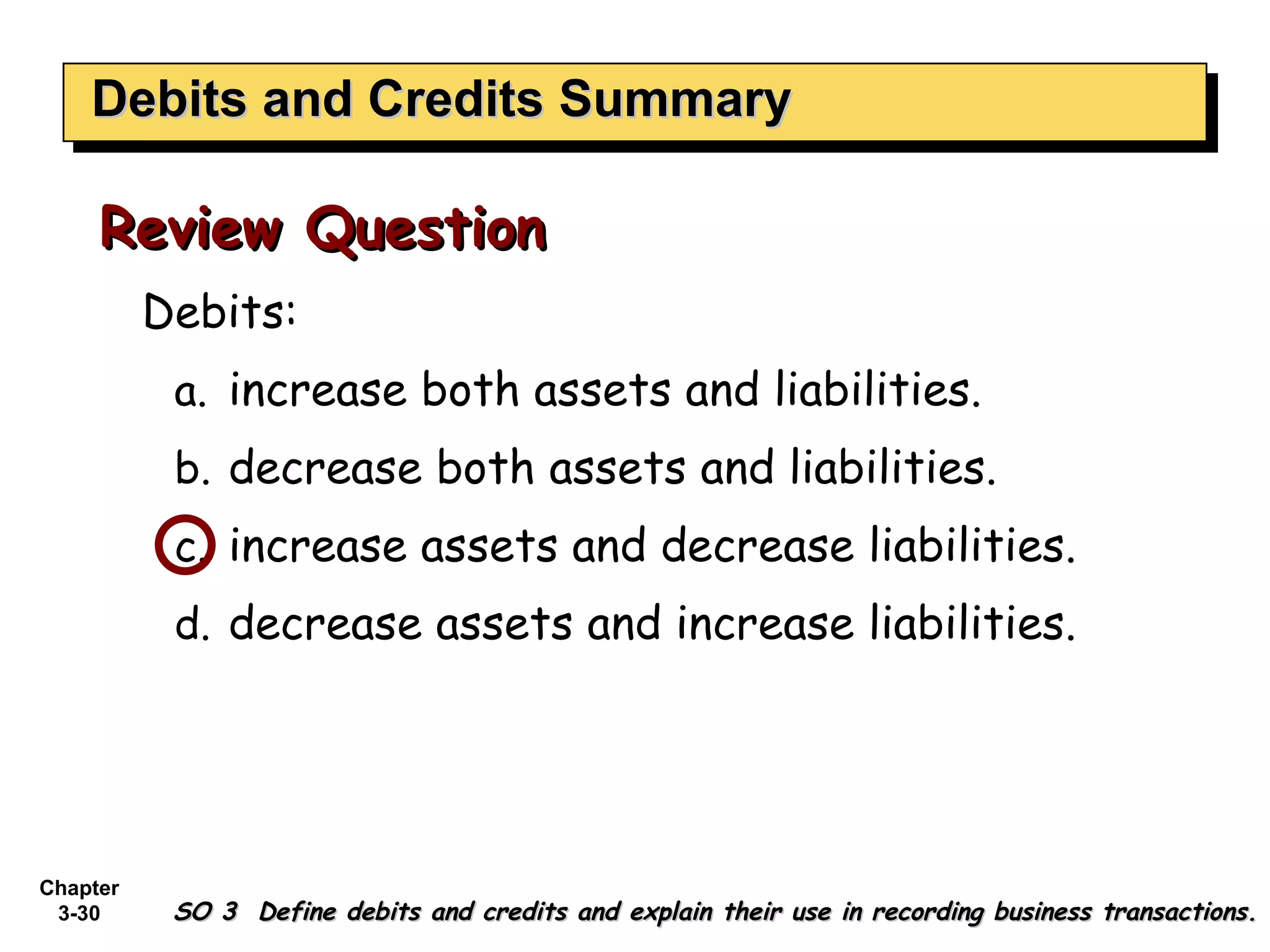

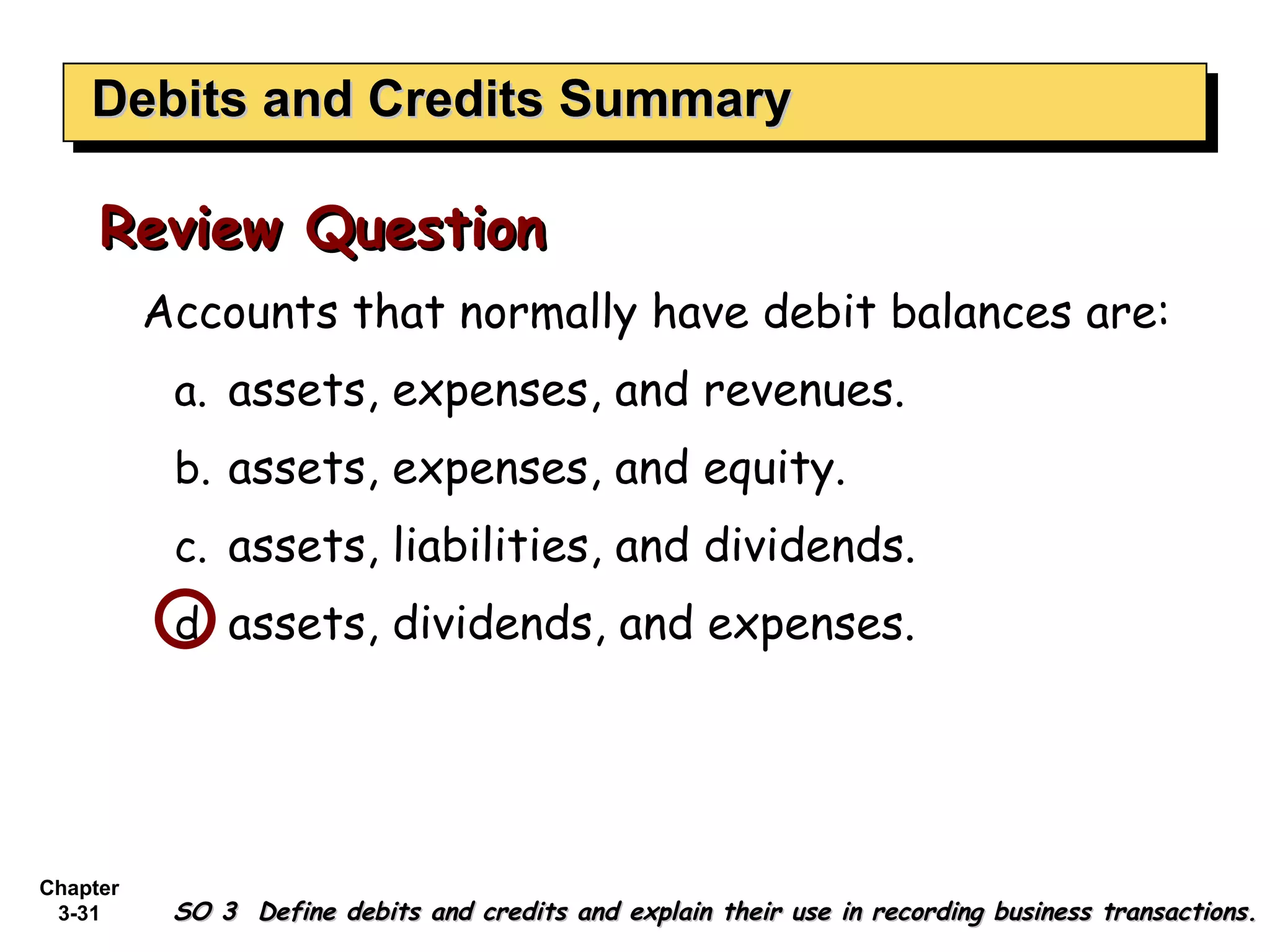

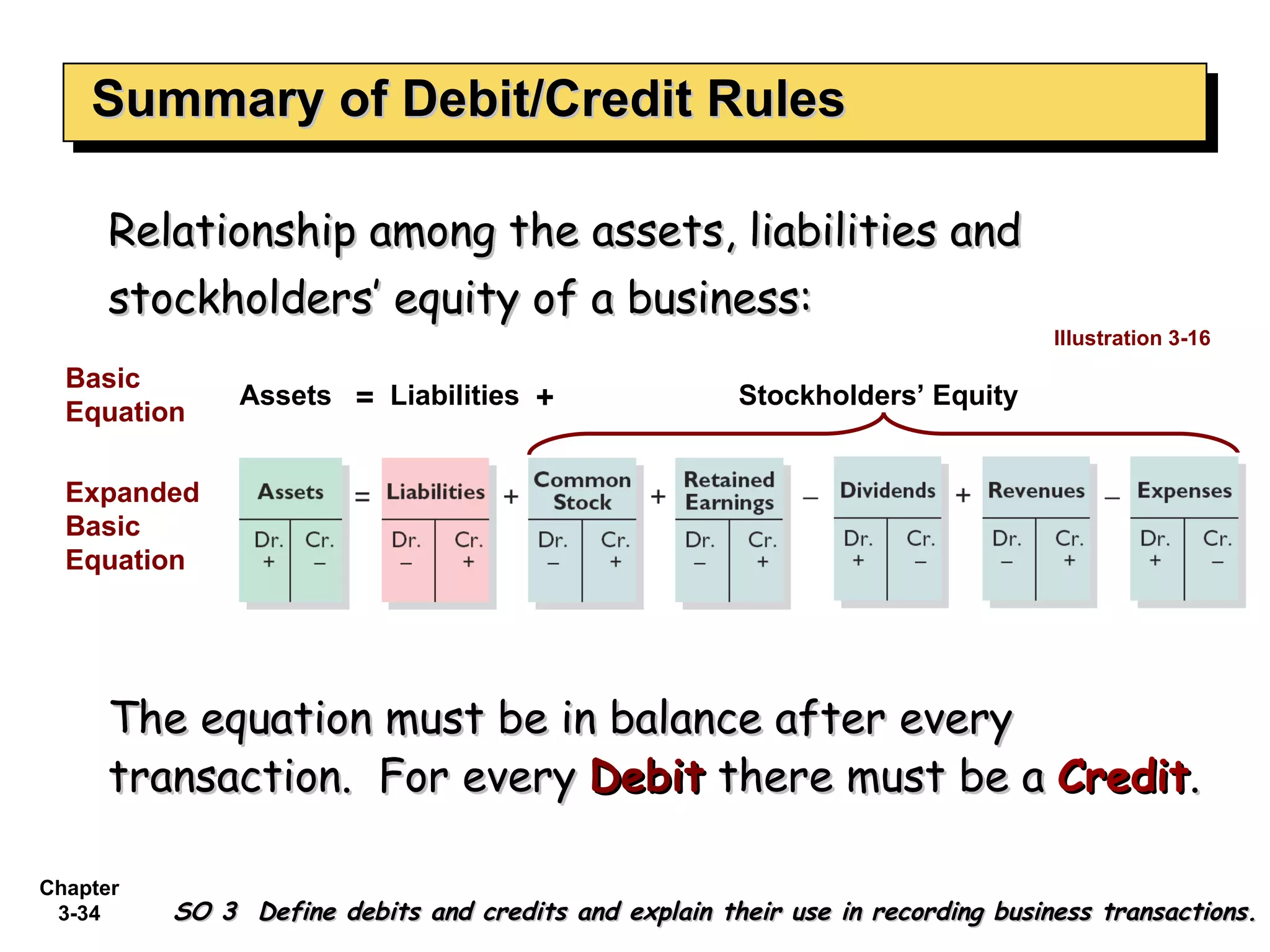

2) The use of debits and credits to record transactions and their effect on different types of accounts.

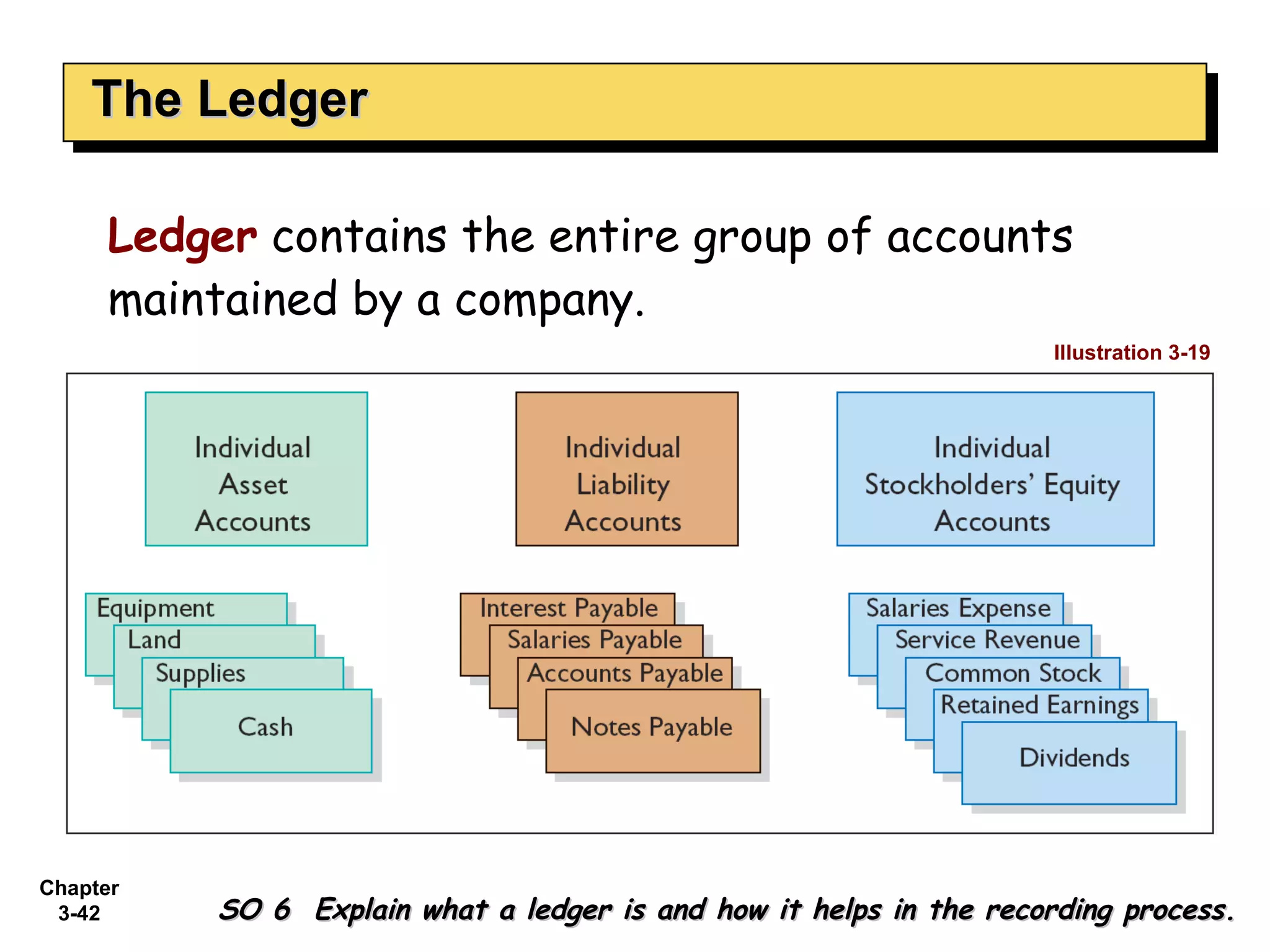

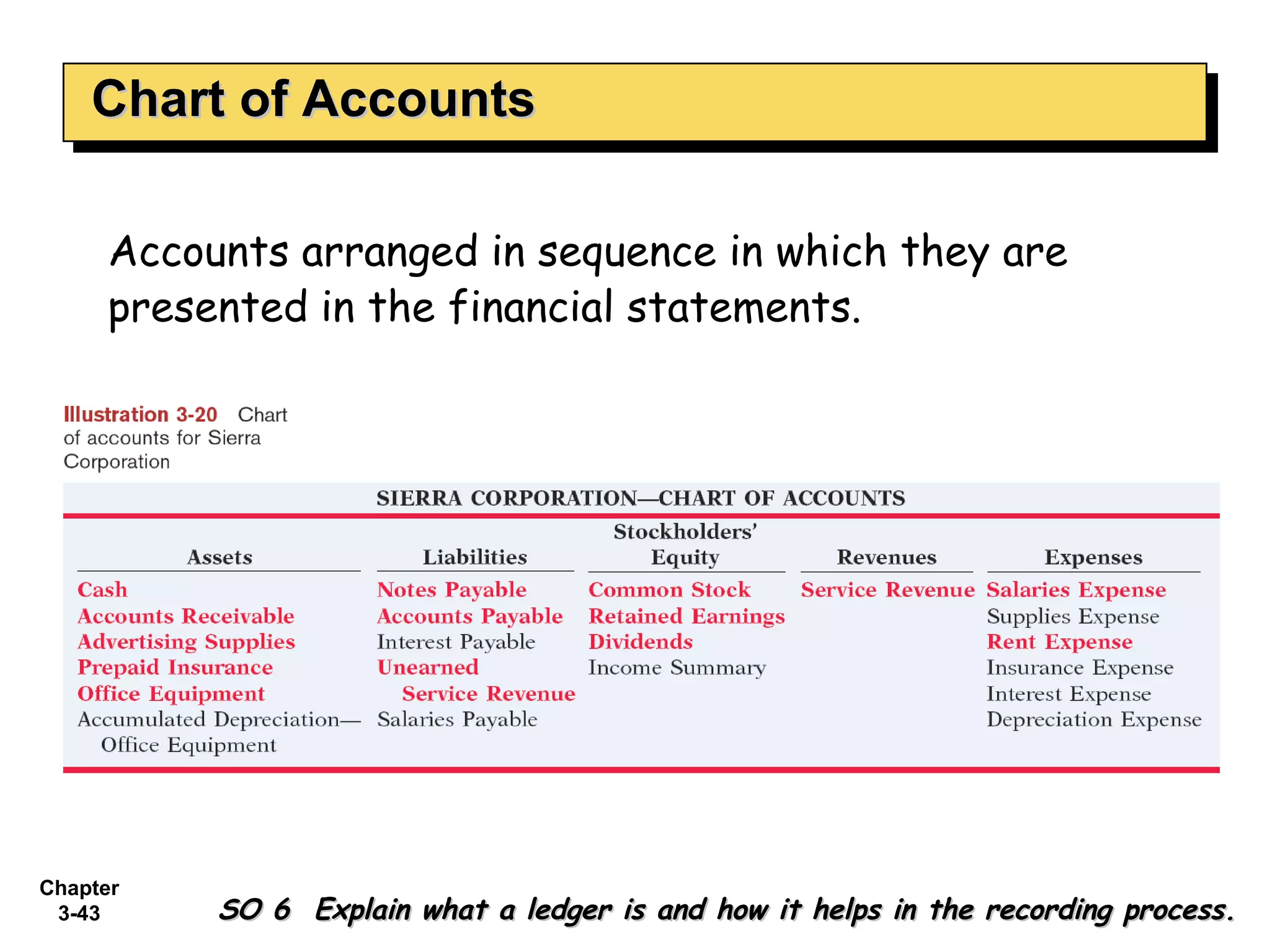

3) The purpose and use of accounts, journals, ledgers, and the trial balance in the recording process.