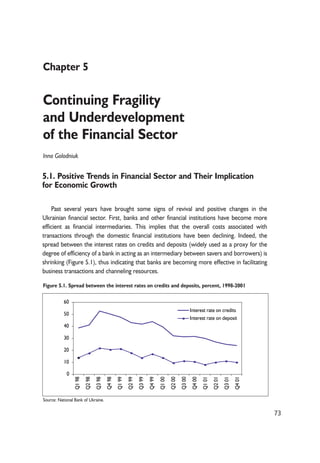

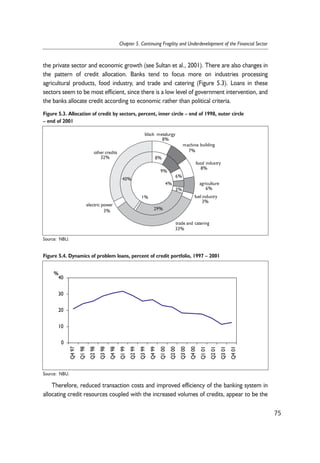

Download to read offline

![107

References

Antczak, R. (1996), Foreign Trade and Balance of Payments of Ukraine in 1992-1995 [Handel

zagraniczny i bilans p³atniczy Ukrainy w latach 1992-1995], [in:] M. D¹browski and R.

Antczak eds., Ukrainian Path to the Market Economy 1991-1995 [Ukraiñska droga do

gospodarki rynkowej 1991-1995; in Polish], CASE, Warsaw.

Aslund, A. (2001). Ukraine's Return to Economic Growth. Post-Soviet Geography and Economics,

Vol. 42 No. 5, pp. 313-328.

Aslund, A. (1994). Lessons of the First Four Years of Systemic Change in Eastern Europe, Journal

of Comparative Economics, Vol. 19, No. 1.

Babanin, O., V. Dubrovskiy and O. Ivaschenko (2002), Ukraine: The Lost Decade … and a

Coming Boom?. The GDN "Explaining Growth" working paper, In press, Available at:

http://www.eerc.ru/activ/GDN/.

Barth, J. R., G., Jr. Caprio, and R. Levine (2001), Bank Regulation and Supervision: What Works

Best? World Bank Working Paper.

Benecke Ch., and St. von Cramon-Taubadel (2001), The present and future profitability of

sugar production in Ukraine, [in:] St. von Cramon-Taubadel, S. Zorya, L. Stiewe (eds.),

Policies and Agricultural Development in Ukraine, pp. 214-239, Shaker-Verlag: Aachen.

Blanchard, O. (1997), The Economics of Post-Communist Transition, Clarendon Press: Oxford.

CASE (2002), Global Economy. Quarterly Outlook, No. 2/2002 (6), CASE, Warsaw. April. At

www.case.com.pl

CASE (2000-2001), Quarterly Ukrainian Economic Outlook – Trends, Opinions, Forecasts (in

Russian), Various editions.

Cabinet of Ministries of Ukraine (2001), Reformi zaradi dobrobutu v 2000 [Reforms for

Welfare in 2000], March 2, 2001.

D¹browski, M. (1994). Ukrainian Way to Hyperinflation, CASE, Studies and Analyses, No. 12,

Warsaw.

D¹browski, M., U. Górski, and M. Jarociñski (1999), Inflationary Consequences of Devaluation

Crisis in Russia and Ukraine: The First Observations, CASE Studies and Analyses, No. 159.

Dubrovskiy, V. (2001), Economic Transformation in the NIS and Failure of the Washington

Consensus: More Questions than Answers, [in:] Szyrmer and D. Snelbecker (eds.), Reforms

in Ukraine: Ideas and Actions, J. Kyiv, Alterpress, pp. 81-103.

Dubrovskiy, V., T. Shygayeva, O. Bilothsekivets, R. Bondarenko, M. Golovanenko (2001a),

The Impact of Privatization to the Economic Behavior and Performance of the Firms in the](https://image.slidesharecdn.com/rc55-141023035342-conversion-gate02/85/CASE-Network-Reports-55-The-Sources-of-Economic-Growth-in-Ukraine-after-1998-Currency-Crisis-and-the-Country-s-Prospects-107-320.jpg)

![Context of General Economic Conditions in Ukraine, Analytical Report, funded by SPFU.

Under the supervision of J. Szyrmer. HIID/CASE, mimeo, http://www.case-ukraine.

kiev.ua

Dubrovskiy, V., T. Shygayeva, O. Bilothsekivets, R. Bondarenko, M. Golovanenko (2001b),

The Impact of Privatization to the Economic Behavior and Performance of the Firms in the

Context of General Economic Conditions in Ukraine in the years of 2000-2001, Analytical

Report, funded by SPFU. Under the supervision of J. Szyrmer. HIID/CASE, mimeo,

http://www.case-ukraine.kiev.ua

Dubrovskiy, V., and T. Shygayeva (2000), It Would Go Worse Without Privatization: The Analysis

of Balance Sheets of the Industrial Enterprises Says for the Non-State Sector of the Economy

(in Russian), Zerkalo Niedeli newspaper (The Mirror Weekly), No. 7(280).

Dubrovskiy, V. (2001), Privatization and Growth in the Real World: The Case of Ukraine, [in:] A.

Paskhaver (ed.), The Ukrainian Privatization: Pros and Contras, Alterpress, Kyiv.

Easterly W., and R. Levine, (2000), It's Not Factor Accumulation: Stylised Facts and Growth

Models. Mimeo.

Enste, D., and F. Schneider (2000), Shadow Economies Around the World: Size, Causes and

Consequences, IMF Working Paper, WP/00/26.

Estrin, S. and R. Rosevear (2000), The Transformation of Ownership in Ukraine and Policy

Options, Economic Essays, Institute of Reforms, Kyiv, Available at: www.ir.org.ua (in

Ukrainian).

Estrin, S. and R. Rosevear (1998), Enterprise Performance and Corporate Governance in

Ukraine, paper presented during Workshop on Corporate Governance in Russia, London

Business School, June.

Fischer, S., and R. Sahay (2000), The Transition Economies after Ten Years, NBER Working

Paper No. W7664, April.

Frydman, R., Ch. Gray, M. Hessel and A. Rapaczynski (1997), Private Ownership and Corporate

Perormance: Some Lessons from Transition Economies, Research Report RR#97-28. C.V.

Starr Center for Applied Economics, New York University.

Frydman, R., M. Hessel, and A. Rapaczynski (1998), Why Ownership Matters? Politicization and

Enterpreneurship in the Restructuring of Enterprises in Central Europe. Research Report (RR

98-14). C.V. Starr Center for Applied Economics, New York University.

German Advisory Group on Economic Reform (2001), Welche Maßnahmen im

Landwirtschaftsektor führten zum Erfolg? [in:] Die ersten 365 Tage: Ein konstruktiver

Rückblick auf die Wirtschaftsreformen in der Ukraine im Jahr 2000, Deutscher

Beratergruppe Wirtschaft bei der ukrainischen Regierung, Kyjiv, January, pp. 18-28.

Guriev, S., and B. Ickes (2000), Microeconomic Aspects of Economic Growth in the Eastern

Europe and the Former Soviet Union, 1950-2000, Paper for the Research Project of

108

CASE Reports No. 55 – The Sources of Economic Growth in Ukraine ...](https://image.slidesharecdn.com/rc55-141023035342-conversion-gate02/85/CASE-Network-Reports-55-The-Sources-of-Economic-Growth-in-Ukraine-after-1998-Currency-Crisis-and-the-Country-s-Prospects-108-320.jpg)

![Global Development Network, "Explaining Growth", http://www.eerc.ru/activ/

GDN/Guriev_IckesPaper.pdf

Guriev, S., and B. Ikces (1999), Barter in Russia. [in:] P. Seabright (ed.), The Vanishing Ruble:

Barter and Currency Substitution in Post-Soviet Societies, Cambridge University Press:

Cambridge, UK.

Gylfason, T. (2001), Natural Resources and Economic Growth, Paper for the conference "The

Factors of Sustainable Economic Growth in Ukraine", Kyiv, June 25-26.

Hellman, J., and M. Schankerman (2000), Intervention, Corruption, and Capture, Economics of

Transition, Vol. 8(3), 2000, pp.545-576.

Hellman, Joel S. (1998), Winners Take All. The Politics of Partial Reform in Post-Communist

Transitions, World Politics 50, pp. 203-234.

Ickes, B. and Gaddy, (1998), Enterprises in Russia, Paper presented during Academic

Workshop on Corporate Governance in the Former Soviet Union, London Business

School, June.

IER (2002), Monthly Economic Monitor of Ukraine, Monthly outlook by Institute for Economic

Research and Policy Consulting, Kiev, Various editions, available at www.ier.kiev.ua

IFC, (1997), 1997 Business Survey, Obstacles to Small Business Development in Ukraine,

International Financial Corporation, Kyiv.

IMF (2001), Ukraine. Staff Report for the Fifth and Sixth Reviews Under the Extended

Arrangement, IMF, Washington, D.C., August.

Johnson, S., McMillan, J., and C. Woodruff (2000), Property Rights and Finance, MIT Working

Paper. At http://web.mit.edu/sjohnson/www/home.htm

Kornai, J. (1986), The Soft Budget Constraint, Kyklos, 39(1) pp. 3-30.

Libanova, E., O. Poznyak (2002), The Labour Migrations from Ukraine – a New Migration

Potential from Eastern Countries, Paper presented at Beyond Transition – Development

Perspectives and Dilemmas CASE conference. Falenty near Warsaw, Poland, April 12-13.

Lunina, I., and V. Vincetz, (1999), Subsidizing Ukraine's Enterprises, [in:] Ukraine at the

Crossroads, Springer Verlag, pp.118-132.

Nelson, R. and S. Winter (1982), An Evolutionary Theory of Economic Change, Harvard

University Press, Cambridge, MA.

Paskhaver, A. (2002), Two years of economic growth: more questions than answers, The PiC

(weekly), #9 (140), 2002, Kyiv (in Ukrainian), http://www.pic.com.ua/9 140/achas/c7.htm

Paskhaver, A. (1999), Prospects for Entrepreneurship in Ukraine: Privatization and Gains of the

New Capital, Monitoring of Ukrainian Economy 1/43.

Roe, A. (ed.) (2001), Ukraine: The Financial Sector and the Economy. The New Policy

Agenda, World Bank. Available at www.worldbank.org.ua

Shleifer, A., T. Frye (1997), The Invisible Hand and the Grabbing Hand, American Economic

Review Papers and Proceedings, May.

109

References](https://image.slidesharecdn.com/rc55-141023035342-conversion-gate02/85/CASE-Network-Reports-55-The-Sources-of-Economic-Growth-in-Ukraine-after-1998-Currency-Crisis-and-the-Country-s-Prospects-109-320.jpg)

![Shygayeva, T. (2001a), Industrial Production and Finance, [in:] J. Szyrmer (ed.), Ukraine:

Monetizing a Transition Economy, Harvard/CASE Ukraine Project, Kyiv.

Shygayeva, T. (2001b), Industry of Ukraine in 2000, Financial Risks, #1/2001, pp.7-43.

Shygayeva, T. (2000), Industry of Ukraine in 1999, Financial Risks, #1/2000, Kyiv (in Russian).

Striewe, L., and St. von Cramon-Taubadel (2001), Ernstfall Rekordernte: Was läuft schief auf

den Ukrainischen Getreidemärkten? Deutscher Beratergruppe Wirtschaft bei der

ukrainischen Regierung, Kyiv, September (manuscript).

Sultan, Khwaja, Dimitar Mishev, and Olga Pogarska, (2001), Finance and Growth, [in:] Janusz

Szyrmer (ed.), Ukraine: Monetizing a Transition Economy, Harvard/CASE-Ukraine,

Alterpress, Kyiv.

Szyrmer, J. (2001), Openness, Distortions and Growth, [in:] J. Szyrmer and D. Snelbecker,

(eds.), Reforms in Ukraine: Ideas and Actions, pp. 81-103. Alterpress, Kyiv.

Szyrmer, J. (2001), Post-Soviet Transition: Problems, Lessons and Solutions, [in:] J. Szyrmer and

D. Snelbecker (eds.), Reforms in Ukraine: Ideas and Actions, pp. 81-103. Alterpress, Kyiv.

Szyrmer, J., and O. Besedina, (2001), Transactions in Transition: To Barter or Not to Barter, [in:]

Ukraine: Monetizing a Transition Economy, J. Szyrmer (ed.), Alterpres, Kyiv.

Szyrmer, J. and V. Dubrovskiy (2001), Influence of Privatization on Behavior and Economic

Performance of Enterprises in the Context of Economic Situation in 2000-2001, CASE-Ukraine,

www.case-ukraine.org.ua.

Szyrmer, J., V. Dubrovskiy, and T. Shygayeva (1999), Is the Private Sector More Efficient? ICPS

Policy Studies 1, http://www.icps.kiev.ua.

UDN. Ukraine Daily News. Daily on-line news of Ukrainian News Agency.

World Bank (2002), Transition. The First Ten Years. Analysis and Lessons for Eastern Europe and

the Former Soviet Union, The World Bank, Washington, D.C.

Yakoub, M., B. Senchuk, and T. Tkachenko (2001), Ukrainian Enterprises in 2000: An IFC

Survey of Ukrainian Business, Report by IFC Ukraine Business Development Project.

Zhurzhenko, T. (1998), Ukrainian Women in the Transitional Economy, Labour Focus on

Eastern Europe, No. 60.

110

CASE Reports No. 55 – The Sources of Economic Growth in Ukraine ...](https://image.slidesharecdn.com/rc55-141023035342-conversion-gate02/85/CASE-Network-Reports-55-The-Sources-of-Economic-Growth-in-Ukraine-after-1998-Currency-Crisis-and-the-Country-s-Prospects-110-320.jpg)

This document, prepared for the World Bank, analyzes the sources of economic growth in Ukraine from the late 1990s and discusses the sustainability of this growth. It covers macroeconomic outlook, external sector developments, microeconomic prerequisites for growth, fiscal policy, and challenges for future growth. The study indicates the complex interplay of various macro and microeconomic factors affecting Ukraine's economy, emphasizing the need for comprehensive reform to ensure sustained economic progress.

![Economic overview-final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/economic-overview-final1-120329125506-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)