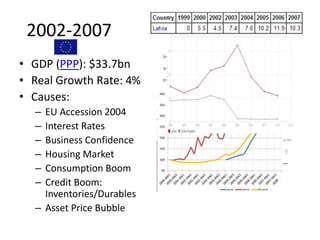

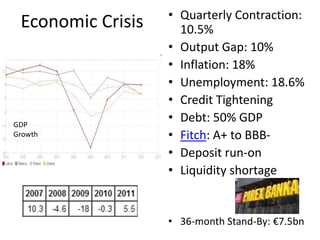

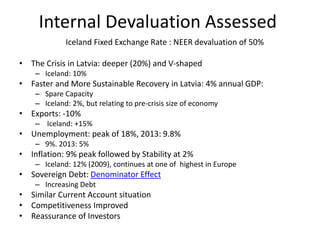

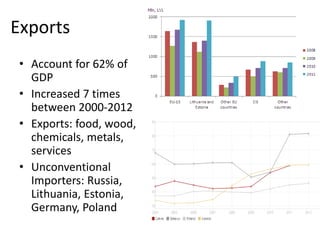

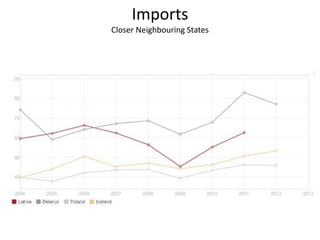

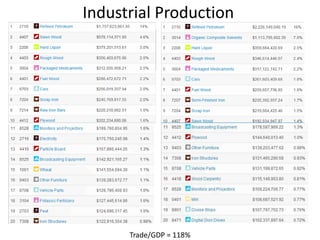

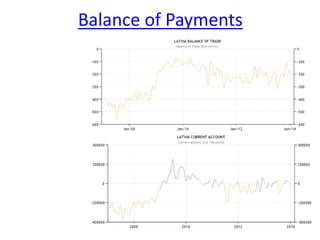

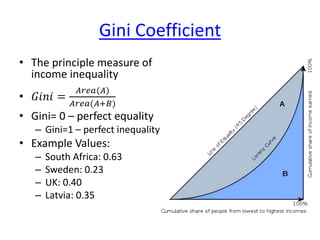

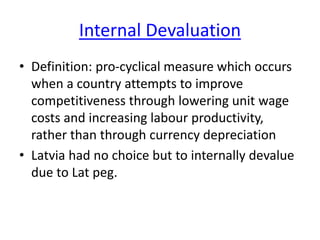

Latvia is a country located in Northern Europe with a population of 2.2 million. Its economy relies heavily on exports, which account for over 60% of GDP. During an economic crisis from 2008-2010, Latvia experienced a severe recession with GDP contracting over 10% and unemployment rising to nearly 19%. To recover without devaluing its currency pegged to the euro, Latvia implemented an "internal devaluation" through fiscal austerity, wage cuts, and boosting competitiveness. By focusing on exports and structural reforms, Latvia was able to recover faster than other crisis-hit countries and regain financial stability and investment grade credit ratings.