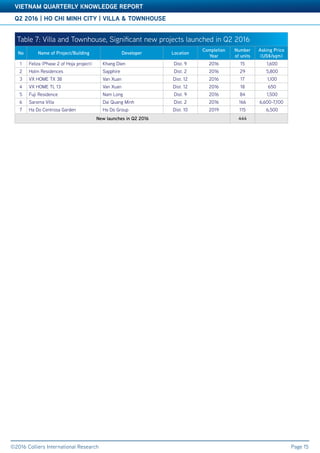

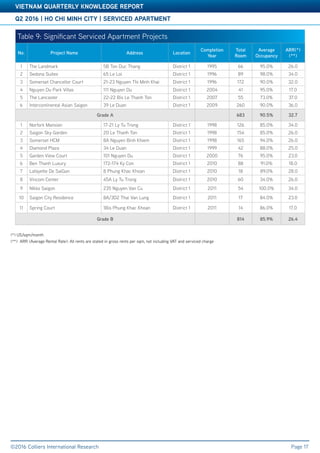

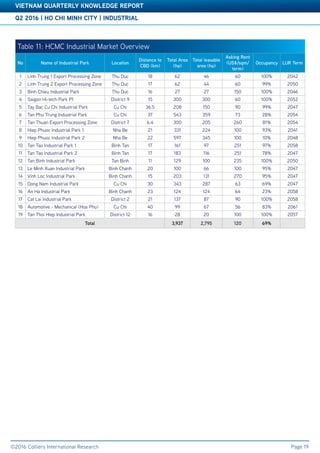

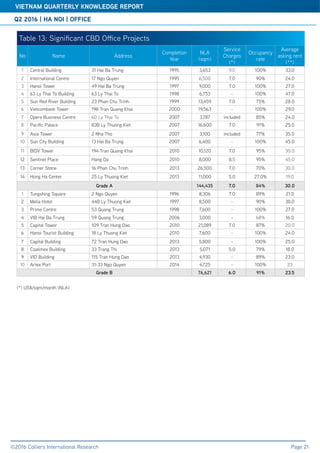

Downloaded 14 times

Vietnam's GDP grew by 5.52% in the first half of 2016, with significant contributions from foreign direct investment and retail sales. Ho Chi Minh City and Hanoi witnessed stable economic performance, with retail sales increasing and an uptick in international arrivals. Despite some challenges, such as adverse weather affecting agriculture, the outlook for the last half of the year remains optimistic, with predictions for a 6.7% GDP growth for the full year.

![Economic overview-final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/economic-overview-final1-120329125506-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)